Dental Clinic in Dubai for Cosmetic Smile Makeover

Health |

2026-06-18 06:46:25

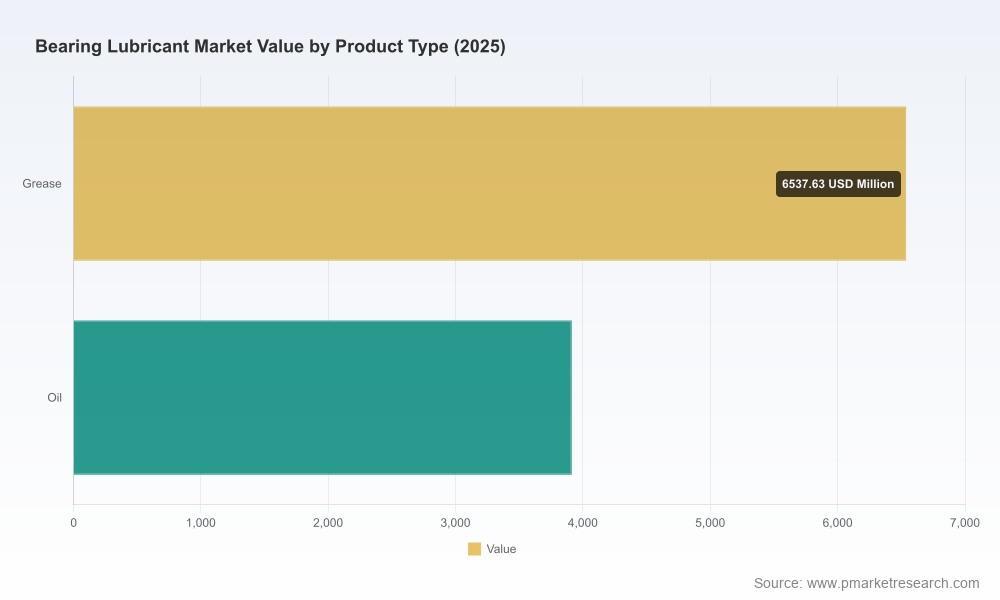

PW Consulting’s latest Bearing Lubricant Market study (base year 2025) equips executives and investors with the actionable intelligence needed to make high-confidence decisions in 2026. The global market reached USD 10,450 Million in 2025 and is projected to expand at a 4.12% CAGR through our 2026–2032 forecast window, arriving at roughly USD 13,863 Million by 2032. This briefing previews the report’s strategic implications — showing the depth of our analysis while withholding the granular segment tables that subscribers will find on our portal.

Bearing Lubricant Market

Timing: 2026 is a hinge year. Regulatory phase-outs, raw material volatility and tariff shifts converge to reshape cost curves and sourcing strategies for bearing lubricants.

Bearing Lubricant Market

Margin pressure: Our cost-model scenarios show that base oil and synthetic feedstock fluctuations can materially compress gross margins unless firms pursue targeted mitigation — procurement hedges, formula re-designs or premium pricing strategies.

Bearing Lubricant Market

Consolidation and specialization: With the top three and five firms controlling meaningful slices of the market (CR3 ~38.4%; CR5 ~52.15%), mid-market suppliers must choose between scale pursuits or differentiation through high-value niches.

Opportunity window: The steady, mid-single-digit CAGR to 2032 supports disciplined investments in R&D, plant upgrades, and aftermarket service models that convert technical leadership into recurring revenue.

Demand balance: Industrial modernization, renewable energy asset growth and vehicle electrification continue to underpin demand for advanced bearing lubrication, but growth is uneven across end-markets. Our demand elasticities and use-case matrices identify where volume growth will be accompanied by willingness-to-pay for premium chemistries.

Raw-material volatility: Base oil prices spiked, with early-2026 market data highlighting an approximate 8% YoY rise to near USD 850/MT in Q1 2026. Premium synthetic base stocks (PAOs) remain costly in key APAC markets. These input trends materially change the economics of synthetic vs mineral formulations and accelerate substitution and reformulation initiatives.

Regulatory risk and impetus: REACH restrictions and standards updates (including ISO 12925 revisions on oxidation stability testing) are driving reformulation cycles and extended qualification timelines for greases that historically relied on phased-out chemistries. Companies that front-load compliance into their 2026 roadmaps gain a two-year time-to-market advantage.

Trade & localization: Elevated tariffs and regional trade measures have amplified the total landed cost for imported lubricants, prompting a renewed emphasis on local manufacturing, toll blending arrangements, and regional supply-chain redundancy.

Technology & services: Predictive maintenance and sensor-enabled lubrication strategies are shifting value capture toward suppliers that bundle product and data-driven service contracts.

Klüber Lubrication (Germany) — Strength: Specialty greases for high-performance and food-grade applications. Strategic posture: deepening formulations certified for strict hygienic applications; recent product launches (e.g., a new NSF H1-certified food-grade grease) reinforce positioning in high-margin niches.

Shell Lubricants (Netherlands) — Strength: Broad industrial portfolio and scale in synthetic lubricants. Strategic posture: expanding availability for EV and electric-motor-specific greases, leveraging brand and upstream integration to defend industrial channels.

Mobil / ExxonMobil (USA) — Strength: Extensive R&D and global supply footprint; recognized product lines for electric motor and food-grade bearings. Strategic posture: emphasize reliability and OEM partnerships to sustain premium pricing.

SKF (Sweden) — Strength: Synergies between bearing systems and customized lubricants. Strategic posture: product updates to meet regulatory and operational demands (e.g., greases optimized for wind turbines) reinforce its systems-supplier model.

Timken, Fuchs, Dow Corning (DuPont), TotalEnergies, Castrol, Chevron — Each brings differentiated strengths: roller-bearing specialization, heavy-industry formulations, precision PFPE solutions, food-safe ranges, and strong aftermarket channels. Collectively, the five largest players create a market dynamic where scale protects pricing in base segments while technical leadership secures premium niches.

Recent movements to note: product launches and regulatory-aligned reformulations in 2024–2025 (including H1-certified food greases and REACH-compliant turbine greases) indicate incumbents are prioritizing compliance-led new product development. These moves raise the bar for entrants and increase the cost of non-compliance for laggards.

Transparent market-sizing & methodology: reproducible top‑down and bottom‑up models with assumptions and sensitivity tables so teams can re-run scenarios under alternate price or demand shocks.

Forecast workbook: baseline and three alternate scenarios (low-demand, high-price, and technology-adoption) covering 2026–2032 with line-item drivers; includes downloadable CSVs for integration into internal planning tools.

Cost and margin dashboards: raw-material exposure matrices, blended base-oil curves, and margin-impact calculators by product family to inform pricing and procurement negotiations.

Regulatory and formulation playbooks: step-by-step reformulation checklists, test-protocol timetables, and certification pathways to maintain market access across regulated regions.

Competitive audit and supplier maps: capability heatmaps for the top global suppliers, OEM partnerships, and channel structures — designed to support go/no-go and M&A decisions.

Go-to-market and aftermarket service frameworks: templates for bundling lubricants with predictive-maintenance services, short-term pilot KPIs, and scaling roadmaps.

Strategic options & M&A screeners: high-level targets and rationale (tech access, capacity, regional footprint) to accelerate inorganic growth or targeted bolt-ons.

Investment and capex guidance: NPV ranges for capacity expansions, tolling vs greenfield trade-offs, and expected payback periods under our three macro scenarios.

Hedge and diversify feedstock exposure — Implement layered hedging (forward buys, multi-sourcing, and long-term contracts) for base oils and PAOs; evaluate toll-blending contracts to transfer volatility and limit fixed-cost expansion.

Rationalize portfolio toward higher-value niches — Prioritize investments in food-grade, EV electric-motor, and wind-turbine greases where technical barriers and certification requirements enable superior margins and stickier customer relationships.

Fast-track regulatory compliance & reformulation — Put a cross-functional “REACH/ISO readiness” task force in place to accelerate approvals and qualify substitutes for restricted chemistries ahead of enforcement timelines.

Localize strategically to mitigate tariff exposure — Where trade measures elevate landed costs, pursue regional manufacturing partnerships, licensing, or contract manufacturing to preserve competitiveness in price-sensitive channels.

Monetize services and digitalization — Pilot sensor-linked lubrication programs with 6–12 month ROI horizons in high-value industrial accounts; use pilot results to sell annualized service contracts that improve customer retention and predictability of revenue.

Adverse raw-material shocks that exceed our stress-test thresholds can compress EBITDA by double digits for commodity-focused portfolios.

Delayed REACH conformity or certification failures for food- or aerospace-grade formulations can result in de‑listing at major OEMs — an immediate revenue and reputational risk.

Failure to adapt pricing mechanisms in contracts (indexation clauses, pass-throughs) leaves suppliers exposed to input cost cycles and competitive undercutting.

Consider this briefing a strategic executive trailer. The full PW Consulting report contains the segment-level forecasts, regional breakdowns, buyer personas, and downloadable models you will need to operationalize the playbook and stress-test investments for 2026–2032. Clients who subscribe gain access to: full segmentation tables, supplier scorecards, price-trajectory models, and our confidential M&A watchlist. For teams preparing 2026 budgets, the report is designed to be directly incorporated into capital allocation and procurement tender documents.

PW Consulting stands ready to run a hands-on scenario session for C-suite and board teams to translate these insights into a 90‑day activation plan. Request access to the full report and our custom scenario workshop to convert the market’s forecasted mid-single-digit growth and structural shifts into concrete, defensible decisions for 2026.

For detailed analysis of this topic, please visit the official page:Bearing Lubricant Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com