High-Performance Composites Market to Reach USD 95 Billion by 2034 Driven by Aerospace, EVs, and Renewable Energy Growth

Other |

2026-06-26 09:00:58

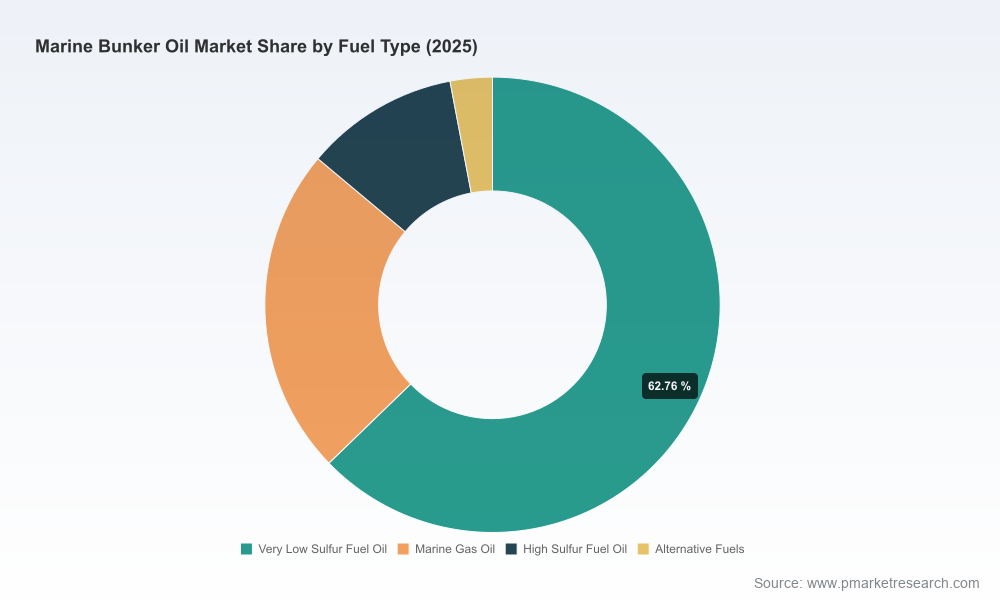

PW Consulting’s Marine Bunker Oil Market study (base year 2025) arrives at a pivotal moment for shipping and energy decision-makers. After recovering from pandemic-era disruptions, the global bunker market reached an estimated overall size of USD 198.45 Billion in 2025. Our forecasted compound annual growth rate (CAGR) of 4.72% across the 2026–2032 horizon points to steady expansion, with the market trending toward roughly USD 274 Billion by 2032 under our central case. Historical dynamics from 2020–2025 show a pronounced rebound interspersed with episodic volatility, reinforcing the need for scenario-ready strategies into 2026 and beyond.

Marine Bunker Oil Market

This briefing is deliberately crafted as a “trailer”: it synthesizes strategic conclusions and practical recommendations drawn from the full PW Consulting report while withholding granular, segment-level data to preserve the commercial value of the primary analysis. The full report contains the proprietary models, port-level stress tests, and vendor scorecards that senior leaders use to commit capital and reshape procurement in 2026.

Marine Bunker Oil Market

Regulatory acceleration. The regulatory landscape shifted materially with amendments to MARPOL Annex VI (low-flashpoint and gas-fuels guidance) and SOLAS updates that require supplier declarations on minimum fuel flashpoint. New Emission Control Areas (ECAs) designated for high-latitude waters and advancing NOx and sulphur controls will materially reshape compliance pathways.

Marine Bunker Oil Market

Supply elasticity under stress. In early 2026 the market signalled tightening in several Asian hubs, pushing regional premiums to multi-year highs and, in some cases, making refuelling logistics episodic rather than routine. These supply tight points translate directly into operational risk for voyage planning and bunker procurement.

Fuel quality and alternative blends. Standards evolution (the updated ISO 8217 series and revised bunker delivery notes) plus emerging research on biodiesel–bunker blends has created both technical uncertainty and opportunity. Compliance testing and chain-of-custody controls are now core procurement requirements, not optional extras.

Proprietary demand-supply modelling: multi-scenario forecasts covering shipping activity, refinery yield shifts, and fuel substitution pathways to 2032, with sensitivity levers for fuel price shocks and regulatory tightening.

Port resilience matrix: an actionable assessment of operational bottlenecks and alternative sourcing routes for the world’s major bunkering hubs — designed for procurement teams to reduce voyage-level risk.

Supplier risk and value scoring: an independent assessment of physical suppliers, integrated traders, oil majors, and state-owned entities against delivery reliability, quality control, credit exposure and compliance capability.

Commercial playbooks: contract clause templates, bunkering SOPs, escalation workflows for quality disputes, and hedging strategies tailored to bunker price drivers.

Decarbonization pathways: fleet-level decision trees comparing retrofit, dual-fuel conversion, and alternative fuel procurement options, with CAPEX/OPEX tradeoffs under multiple carbon pricing scenarios.

Executive dashboards: ready-to-deploy KPIs and early-warning indicators for CFOs, heads of procurement, and fleet operations to align corporate planning in 2026.

The bunker supply universe remains fragmented by volume and capability. Our concentration analysis indicates that the market is not dominated by a small cartel: the top three suppliers account for a modest share of global volumes, and the top five still leave substantial room for independents and regional players. This fragmentation keeps margins competitive but increases counterparty risk for large-scale buyers who require consistent, quality-assured delivery across many ports.

Corporate types to watch:

Integrated oil majors (e.g., Shell, BP, ExxonMobil, Chevron, TotalEnergies) — leverage downstream refining and terminal networks to bundle fuel supply with broader logistics and emerging lower-emission solutions.

Global trading houses and logistics integrators (e.g., Vitol, Trafigura, World Kinect) — compete on price discovery, flexible origination, and cross-commodity risk management.

Independent physical suppliers and regional champions (e.g., Bunker Holding, Peninsula Petroleum, Minerva Bunkering, Chemoil, Sinopec Bunker, Chimbusco, PetroChina and other state-backed suppliers) — excel in port-level execution and local regulatory navigation.

Rising challengers — a new cohort of entrants including fast-scaling regional players recently recognized in port rankings demonstrate how market share can shift quickly where operational excellence meets opportunistic supply windows.

Recent industry developments underscore these dynamics. New entrants achieved top-tier port rankings in 2025/2026, regulatory updates tightened supplier declaration requirements for flashpoint and safety, and industry bodies commissioned fresh research on biodiesel-blend pollutant pathways — all factors that change commercial negotiating power and technical compliance costs in 2026.

For shipowners, charterers, and energy suppliers, the intersection of regulatory tightening, supply concentration volatility, and evolving fuel specs creates six immediate imperatives for 2026:

Reassess counterparty exposure: diversify suppliers across corporate types and geographies; introduce performance-linked clauses and escrowed testing funds to manage quality disputes.

Embed compliance into procurement: require certified flashpoint declarations, independent sampling protocols, and digital Bunker Delivery Note flows to reduce port-time risk.

Stress-test voyage economics: incorporate bunker stress scenarios into commercial voyage planning and time-charter negotiations, capturing the asymmetric impact of localized supply tightness.

Hedge selectively: use a combination of physical forward purchases and financial derivatives calibrated to bunker-price drivers to smooth cash flow volatility without locking away operational flexibility.

Invest in operational resilience: optimise port calls, increase use of intermediate storage where viable, and negotiate priority access terms in high-risk hubs.

Align decarbonization and compliance paths: map regulatory timelines against retrofit windows and alternative fuel availability to avoid stranded capex and to secure fuel-supply pathways early.

Suppliers should prioritize demonstrable quality controls, fast digital documentation, and strategic node investments in high-premium ports. For investors, the combination of fragmented market shares and regulatory-driven value creation suggests attractive targets in logistics, testing labs, and technology stacks that enable traceable, compliant bunkering. M&A activity is likely to accelerate where scale materially reduces vessel-day risk for large account portfolios.

PW Consulting’s full Marine Bunker Oil Market report provides the detailed, executable intelligence required to move from strategy to contracts, capex approvals, and operational change programs. The report includes the granular, proprietary datasets and port-by-port, fuel-type and vessel-type analyses that underlie the summary conclusions above.

This briefing is intended to guide executives toward the right questions and immediate actions in 2026. For the full dataset, supplier scorecards, scenario model access, and a tailored workshop to translate findings into an implementation roadmap for your organisation, contact PW Consulting to request the complete report and advisory engagement options.

For detailed analysis of this topic, please visit the official page:Marine Bunker Oil Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com