Piston Connecting Rod Unit Market: Strategic Intelligence for 2026 Decisions — PW Consulting Releases Executive Preview

PW Consulting today publishes a teaser executive narrative for our forthcoming Piston Connecting Rod Unit Market research report (base year 2025, historical coverage 2020–2025, forecast 2026–2032). The study synthesizes macro-market dynamics, supplier positioning, technology evolution and supply-chain risk to produce an actionable decision framework for OEMs, Tier-1 suppliers, private-equity investors and procurement teams preparing strategies for 2026 and beyond.

Piston Connecting Rod Unit Market

Executive snapshot

- The market tracked in our report reached approximately USD 5,348.6 Million in 2025 after steady expansion from USD 4,810.5 Million in 2020.

- PW Consulting projects the market to continue expanding through 2032, with an underlying compound annual growth rate (CAGR) of 2.15% across the 2026–2032 forecast horizon and an estimated market trajectory consistent with mid-single-digit volatility year-to-year.

- Market concentration remains moderate: the three-largest suppliers capture roughly 31.4% of the market, while the top five account for approximately 45.8% — a structure that supports both global scale plays and niche, high-performance specialists.

Why this report matters for 2026 strategic planning

2026 is shaping up as a hinge year for engine-component strategies. Several intersecting forces — continued optimization of internal-combustion powertrains, performance-weight trade-offs where downsizing and boosted applications remain common, and the industrial aftermarket’s longer replacement cycles — mean that decisions made now on capacity, alloy selection, and partner networks will determine cost and capability profiles for the next product cycle.

Piston Connecting Rod Unit Market

Our analysis converts macro inputs into a practical set of levers. We model demand scenarios tied to vehicle production outlooks, durability requirements and aftermarket replacement rates; we layer in raw-material and processing shocks (forged/alloy steel prevalence, evolving forging methods, and the current softening of steel-price momentum); and we quantify the operational implications for suppliers operating at different tiers and specializations.

Piston Connecting Rod Unit Market

Key takeaways for executive teams

- Resilience through capability balance — Scale is necessary but not sufficient: leading suppliers combine high-volume forged-steel expertise with advanced metallurgy and precision processes. Manufacturers lacking either breadth or differentiated alloy/process capability are exposed to margin compression and specification displacement.

- Material and process premiumization — Demand for higher strength-to-weight ratios pushes investment into advanced forging processes, new alloys and more precise heat-treatment protocols. These technology investments have multi-year payback profiles; prioritization in 2026 will influence competitiveness in the 2028–2030 product cycles.

- Supply-chain agility matters more than lowest-cost sourcing — Overcapacity in steel and muted near-term demand growth imply limited near-term price recovery. Yet volatility remains: supplier selection should be driven by dual criteria of quality/certification compliance (ISO and OEM standards) and the capacity to scale or contract volumes without long lead-time penalties.

- Aftermarket & performance segments provide margin insulation — While core OE volumes trend with vehicle production, aftermarket and specialized performance segments continue to reward differentiated product portfolios and direct channels; firms that cultivate these segments will find insulation against cyclicality.

Competitive landscape — players to watch

The market is bifurcated between large, diversified engine-component suppliers and a vibrant set of high-performance specialists. PW Consulting’s competitive workstreams map capabilities across product architecture, metallurgical know-how, manufacturing scale, certification footprint and go-to-market routes.

- Major OEM-focused suppliers (examples): Several established global component houses provide integrated piston-connecting-rod assemblies and benefit from deep OEM relationships and scale manufacturing systems. These firms drive category standards on production tolerances, dimensional interchangeability and warranty-backed supply chains.

- Forging and heavy-engine specialists: Players with expertise in forged crankshafts and high-volume connecting rods are well-positioned for commercial vehicle and industrial engine programs, where durability and lifecycle cost dominate procurement decisions.

- Performance and motorsport specialists: A distinct cohort of manufacturers focuses on high-performance alloys (including titanium and billet solutions), low-volume bespoke runs and race-specified tolerances. Strategic partnerships and co-branded product lines are common as these suppliers leverage brand equity into adjacent OE and aftermarket opportunities.

Recent industry developments illustrate how competitive positioning is evolving: late-2025/early-2026 strategic partnerships and product updates have increased emphasis on high-performance forged steels and ti-grade solutions, while service instruction updates and targeted component releases in the first months of 2026 highlight the ongoing importance of technical compliance and aftermarket support.

What the PW Consulting report contains — practical, decision-ready deliverables

The full report is structured to move beyond descriptive analytics into direct operational guidance. Key deliverables include:

- Market-sizing and calibrated forecast models (2026–2032) with scenario toggles to test demand sensitivity against vehicle-production, aftermarket replacement intensity and raw-material swings.

- Supplier capability maps and stratified benchmarking across manufacturing scale, alloy/process competence, certification status and end-market exposure.

- Supply-chain vulnerability heatmaps, including tiered supplier loss scenarios, single-source concentration risk and lead-time shock simulations.

- Technology adoption pathways evaluating forging, powder-metal alternatives and cast-competitiveness; each pathway includes cost/benefit timelines and sample capex profiles.

- An M&A and partnership playbook: target archetypes, integration risks, synergies and valuation drivers tailored to strategic buyers and financial sponsors.

- Commercial tactics for procurement and aftermarket channels: pricing frameworks, OEM negotiation levers, aftermarket channel expansion strategies and warranty-cost modeling.

- Operational checklists for 2026: plant readiness, quality systems, alloy sourcing contracts and talent requirements for advanced forging and precision machining.

Strategic recommendations — an action-oriented checklist for 2026

- Prioritize selective capex for metallurgical and forging upgrades where ROI can be demonstrated within a 3–5 year horizon; favor modular upgrades that preserve optionality between forged and powder-metal pathways.

- Lock-in dual-sourcing for critical alloy inputs and build contractual flexibility to manage price and availability swings without compromising OEM qualifications.

- Invest in a targeted aftermarket and performance-channel strategy: these segments provide differentiated margins and reduce exposure to OE volume swings.

- Pursue technology partnerships or minority investments to acquire titanium or billet capability without full-greenfield risk, particularly if your product roadmap targets racing, motorsport or premium performance vehicles.

- Embed data-driven scenario planning in procurement and sales forecasts; the relatively modest market CAGR masks significant subsegment heterogeneity that will reward active portfolio management.

Methodology and confidence bounds

Our market models are built on a multi-source foundation: unit production and replacement rates, OEM program specifications, supplier shipment data, and proprietary interviews across Tier-1s, aftermarket distributors and metallurgical experts. We apply probabilistic scenario analysis to produce a central forecast (CAGR 2.15% for 2026–2032) and two stress scenarios that capture demand shocks and raw-material swings. Confidence is highest where product architecture and OEM specification cycles drive deterministic replacement demand; uncertainty is greater in discretionary performance segments and in timelines for powertrain transitions.

Limitations and where to find the full intelligence

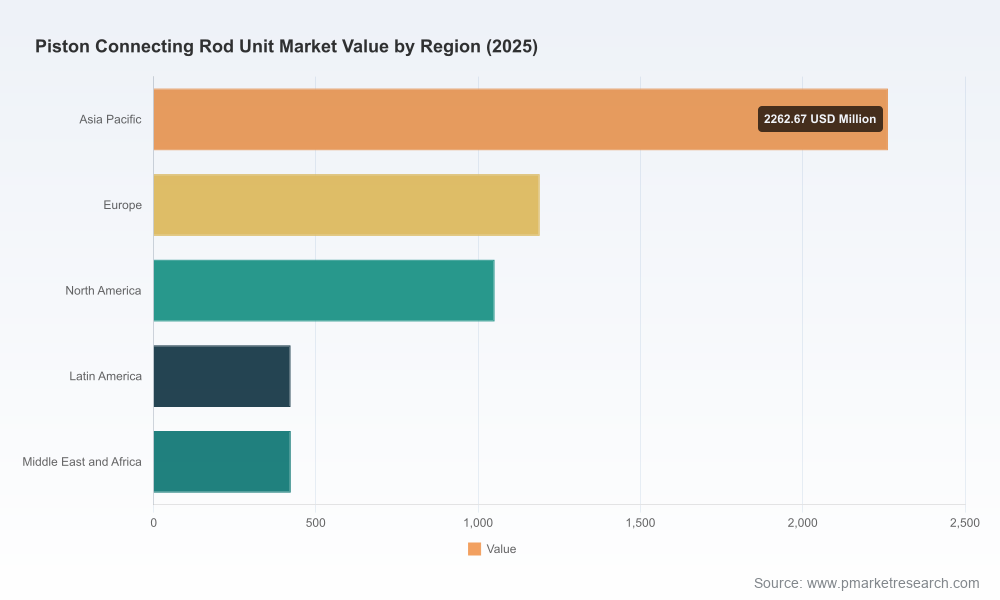

This executive preview is intentionally selective. To preserve the integrity of client-grade insights we are not publishing the granular regional or application splits in this release. The full report contains detailed segmentation tables, regional and application breakdowns, supplier-specific revenue estimates and asset-level capacity maps that are indispensable for transaction diligence or procurement contracting. PW Consulting’s complete dataset and model workbook are available through our report portal and can be licensed with custom scenario workshops for corporate teams.

How to use this insight in Q1–Q3 2026

- Immediate: Run supplier risk audits against the supply-chain heatmap and secure short-term alloy supply flex clauses where exposure is highest.

- Near-term (6–12 months): Initiate technology pilots for lighter materials and higher-strength processing in collaboration with selected suppliers; include performance validation in OEM engineering cycles.

- Strategic (12–36 months): Consider M&A or JV targets that fill capability gaps (e.g., powder-metal competency or titanium billet manufacturing), using the PW Consulting target archetypes and valuation framework.

Conclusion — a call to action

Decisions made in 2026 about capacity, material strategy and partner selection will persist through the 2028–2032 window. PW Consulting’s Piston Connecting Rod Unit Market report gives leadership teams a practical, scenario-driven playbook anchored in market sizing (2020–2025 historicals and a 2026–2032 forecast at a central CAGR of 2.15%), supplier concentration diagnostics and technology adoption roadmaps.

To access the full report, segmented data, company profiles and the interactive forecast model, please visit our report page. PW Consulting also offers tailored workshops to translate the report’s findings into company-specific action plans and financial models.

For detailed analysis of this topic, please visit the official page:Piston Connecting Rod Unit Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com