Robot Joint Precision Reducers Market: Strategic Imperatives for 2026 — PW Consulting Market Brief

As manufacturers accelerate automation and robotics move into increasingly diverse applications, the precision reducers that sit at the heart of robot joint actuation have become a focal point for competitive advantage. PW Consulting’s latest Robot Joint Precision Reducers Market report (base year 2025) synthesizes proprietary forecasting, supplier intelligence, and cost-shock scenarios to equip executives with the situational awareness and actionable playbook needed for 2026 decision-making.

Robot Joint Precision Reducers Market

Market snapshot — momentum and trajectory

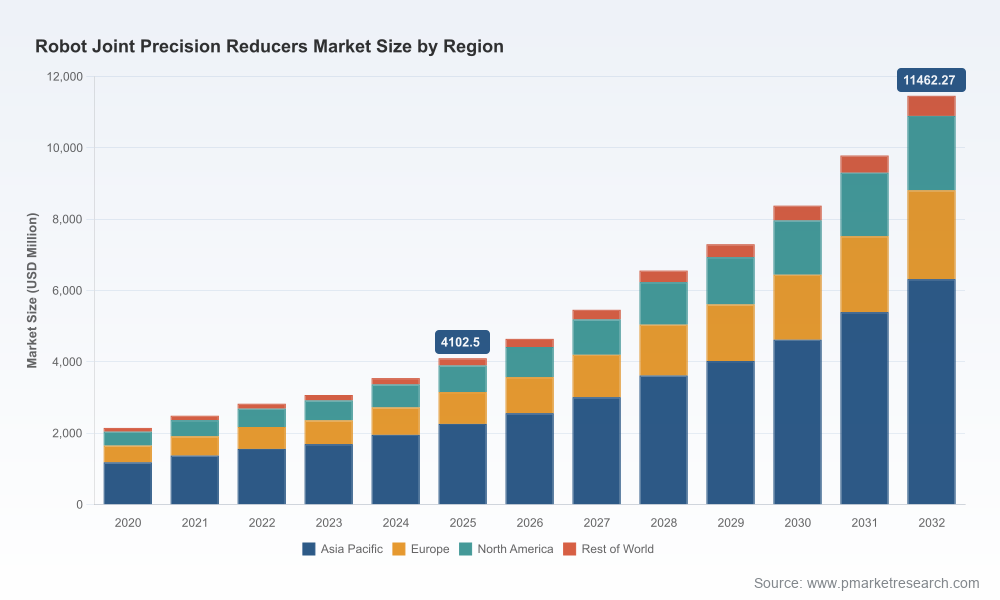

The global Robot Joint Precision Reducers market has expanded rapidly in the first half of the decade, rising from roughly USD 2.15 billion in 2020 to USD 4.10 billion in 2025. Our projection shows continued robust growth through the forecast window (2026–2032), with a compound annual growth rate (CAGR) of 15.81%. By 2032 the market is modeled to exceed USD 11.4 billion, reflecting the intersection of intensifying factory automation, the emergence of humanoid and service robot applications, and ongoing adoption of collaborative robotics in high-mix environments.

Robot Joint Precision Reducers Market

This growth is not homogeneous — it is being driven by technology-specific dynamics (e.g., zero-backlash solutions for high-precision tasks, compact architectures for humanoids, and high-torque, ruggedized units for heavy industrial cells), by end-market demand cycles (semiconductor, automotive, logistics, consumer electronics), and by supplier footprint adjustments in response to cost and capacity shifts.

Robot Joint Precision Reducers Market

What the PW Consulting report delivers

- Quantitative market sizing and seven-year forecasting (2026–2032) built from vendor-derived shipment models, OEM adoption curves, and end-market volume assumptions.

- Supply-side mapping: manufacturing footprints, capacity expansions, and recent capital allocations that materially influence lead times and pricing power.

- Competitive archetypes and risk profiles across three dominant technology families (cycloidal/RV, strain-wave/harmonic, and precision planetary) with practical guidance for product, pricing, and partnership strategies.

- Component-level cost sensitivity analysis that models steel price volatility, bearing supply constraints, and sub-tier specialization to quantify margin exposure under multiple scenarios.

- Go-to-market playbooks for suppliers, OEMs, systems integrators, and private-equity investors — including M&A signaling, aftermarket monetization strategies, and co-development approaches with robotics OEMs.

- Actionable due-diligence templates and an executive dashboard that distills KPIs for procurement, product, and strategy teams to monitor over the next 12–18 months.

Why 2026 is a strategic inflection point

Several converging variables make 2026 a pivotal year for decisions that will determine market position across the next cycle:

- Capacity rebalancing by incumbent manufacturers: Leading Japanese suppliers have announced capacity investments aimed at semiconductor and automotive demand segments. These moves tighten lead times for certain high-spec products while also compressing margins in standard platforms.

- Raw material and input-cost pressure: Recent increases in hot-rolled coil prices underscore a cost environment that can erode component-level margins unless offset by design-for-cost, alternative materials, or supply diversification.

- Product differentiation is accelerating: Compact, zero-backlash designs and integrated actuator modules are shortening development cycles for humanoid and collaborative robots, shifting buying criteria from pure price to total system performance and reliability.

- Market concentration: The top three suppliers capture a substantial share of the market, with the top five further extending control — a structure that creates both barriers to entry and opportunistic niches for specialized challengers.

Competitive landscape — who matters and why

The market is populated by a mix of global incumbents, regional champions, and nimble specialists. Our analysis emphasizes capability vectors rather than raw market share to highlight where strategic advantage accrues:

- Nabtesco Corporation (Tokyo, Japan) — World-class in RV cycloidal technology; strong torque-density and rigidity positions Nabtesco as the default partner for high-throughput industrial OEMs. Recent new product introductions and capacity investments in Japan signal intent to secure semiconductor and automotive supply chains.

- Harmonic Drive Systems Inc. (Tokyo, Japan) — The pioneer of strain-wave reducers remains the leader for ultra-compact, zero-backlash applications, including collaborative and humanoid platforms. Continued product line extensions reinforce their role in miniaturized, precision-critical joints.

- Sumitomo Heavy Industries (Tokyo, Japan) — Focused on high-speed, low-vibration cycloidal solutions, Sumitomo’s technology is tailored to automation scenarios where energy efficiency and vibration mitigation are decisive.

- Wittenstein SE (Germany) — European engineering leadership in precision planetary and cycloidal variants positions Wittenstein to serve high-performance automation markets, particularly where integration with servo architectures is required.

- SPINEA s.r.o. (Slovakia) and other specialists — Companies like SPINEA differentiate through actuator-level integration and bearing innovations that simplify system integration and improve life-cycle reliability for motion-critical joints.

- High-volume Chinese suppliers — A cohort of Chinese manufacturers is scaling production and narrowing the performance delta in common platforms, creating effective cost-competitive options for OEMs prioritizing TCO over peak-spec performance.

Recent product activity — including compact and higher-rigidity launches by major players and catalogue refreshes by specialists — demonstrates how suppliers are competing on both technology and system-level integration. These innovations, combined with targeted production expansions, will materially reshape supply dynamics in 2026.

Strategic implications for stakeholders

For executives making 2026 decisions, the report translates market dynamics into concrete actions across four stakeholder groups:

- Component suppliers — Prioritize modular product families that enable tiered pricing and faster qualification. Invest selectively in actuator-integrated platforms to capture higher ASPs and to lock in OEM design wins.

- Robot OEMs and integrators — Reassess supplier concentration risk and create dual-sourcing strategies for mission-critical reducers. Where possible, co-develop joint roadmaps with suppliers to secure early access to miniaturized, low-backlash technologies for humanoid and collaborative cell designs.

- Procurement & operations leaders — Hedge raw material exposure and negotiate multi-year agreements that include capacity reservation clauses. Build visibility into sub-tier bearing and heat-treatment providers to avoid downstream disruptions.

- Investors and M&A teams — Seek targets that combine proprietary gearing technology with scalable actuator integration, or those that provide aftermarket service contracts — both yield defensible revenue upside as adoption broadens.

Supply chain vulnerabilities and mitigation playbook

Steel price volatility and concentrated bearing supply continue to be the most immediate sources of margin stress. PW Consulting models show that without design or sourcing changes, material cost shocks can compress supplier margins meaningfully.

- Mitigation tactics include: design-for-manufacturability programs to reduce high-cost alloy usage; geographic diversification of heat-treatment and bearing partners; and supplier alliances that share inventory buffers for critical subcomponents.

- On the operational side, near-shoring selective assembly operations and adopting digital twin-driven process controls can materially shorten lead times for high-mix, low-volume product lines.

What we recommend for 2026 — high-priority moves

- Fast-track partnerships between reducer suppliers and motion-system integrators to co-develop actuator modules tailored to humanoid and collaborative end-cases; prioritize programs with clear OEM pipeline commitments.

- Pursue a two-tier product strategy: premium, high-spec platforms for industrial and semiconductor customers; cost-engineered families for high-volume automotive and logistics deployments.

- Implement procurement hedges and contractual capacity reservations tied to performance milestones to protect against input-cost spikes and to assure supply for critical launches.

- For investors: focus diligence on firms that demonstrate aftermarket service capabilities, strong IP in zero-backlash designs, and clear pathways to scale manufacturing without linear increases in working capital.

How PW Consulting can support your 2026 agenda

Our Robot Joint Precision Reducers Market report offers an executive dashboard, scenario-modeling toolkits, supplier scorecards, and a prioritized action matrix keyed to 12- and 24-month KPIs. For teams preparing supplier negotiations, M&A pipelines, or product development roadmaps, we provide tailored workshops that translate the report’s insights into operational plans with measurable milestones.

To preserve competitive value and to encourage direct engagement with our detailed datasets, this brief highlights strategic findings while holding back granular segment-level allocations and proprietary supplier-by-segment financials. Clients who require the full dataset, including region/application breakdowns and vendor-level shipment forecasts, are invited to obtain the full report through PW Consulting’s market portal.

Conclusion

As robotics proliferates into higher-value, human-centric environments, the quality of robot joint reducers will increasingly determine system capability, reliability, and total cost of ownership. 2026 represents a window of opportunity: suppliers who calibrate product portfolios, secure resilient supply chains, and align with OEM system roadmaps will capture outsized share as the market scales toward USD 11+ billion by 2032. PW Consulting’s report equips leadership teams with the foresight and practical tools needed to make those choices with confidence.

For detailed analysis of this topic, please visit the official page:Robot Joint Precision Reducers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com