金属加工油剤市場、安定成長へ—2033年に163億米ドル規模へ拡大予測

Other |

2026-05-06 11:19:15

PW Consulting’s latest market intelligence briefing on the Standalone Analytics Sandbox market equips business leaders with the vantage point required to make high-stakes decisions throughout 2026. Built on a base year of 2025 and a comprehensive historical series from 2020–2025, the report projects the market through 2032 and identifies the structural inflection points that will shape buying, architecture, and governance choices next year. At the macro level the market exhibits robust expansion, underpinned by a compounded annual growth rate of 16.03% and a multi‑fold increase in aggregate value across the forecast window—evidence of both proliferating use cases for safe, isolated analytics and the commoditization of sandbox infrastructure. For executives evaluating strategic options in 2026, the report is designed to translate that macro momentum into executable programs without exposing the granular segment-level line items reserved for the full research package.

Standalone Analytics Sandbox Market

Operational resilience and experimentation: As organizations accelerate model-driven initiatives, the need for isolated environments to safely prototype, validate and iterate models has become non-negotiable. Standalone sandboxes enable discovery without compromising production stability or compliance boundaries.

Standalone Analytics Sandbox Market

Regulatory and privacy pressure: Regulatory regimes—most notably GDPR and its evolving interpretations—are tightening expectations for how sensitive data is used in experimentation. Sandboxes that enforce strict separation and governance are becoming a prerequisite in regulated industries such as healthcare and transportation.

Standalone Analytics Sandbox Market

Cloud maturation: Cloud storage, compute and network improvements have materially lowered the cost and friction of provisioning ephemeral analytic environments, enabling trial-driven procurement and rapid time-to-insight.

Algorithmic risk management: As machine learning and advanced analytics assume higher-stakes roles, institutions are demanding auditable, reproducible evaluation cycles; sandboxes provide the technical scaffolding to embed reproducibility, versioning and lineage into R&D workflows.

Drivers — Democratization, AI demand and secure testing: The convergence of self‑service analytics, demand for explainable AI, and stricter data governance has created a steady stream of adoption across multiple industries. Organizations are prioritizing platforms that allow non-production experimentation, rapid prototyping, and tightly scoped collaboration between data scientists and business users.

Constraints — Integration, governance, and talent: Complexity of legacy systems, inconsistent data quality, and shortages of experienced analytics engineers remain friction points. Successful sandbox programs require investment in integration adapters, governance automation and training to avoid becoming isolated “playgrounds” with low enterprise value.

Market structure — Mid-level concentration: Competitive concentration metrics indicate a market where the top few vendors command meaningful share but no single incumbent determines direction for the whole market. This creates room for specialist players to capture vertical or use-case niches while larger vendors expand platform breadth through integrations and partnerships.

Actionable buy-side playbooks: A staged procurement blueprint—from proof-of-concept to enterprise rollout—covering success criteria, selection matrices and pilot acceptance tests designed specifically for sandbox engagements.

Operational runbooks and governance templates: Concrete artifacts for running sandboxes day-to-day, including data access models, anonymization patterns, environment lifecycle policies, and audit-ready logging configurations that align with privacy requirements.

Architecture reference patterns: Modular design patterns showing how sandboxes integrate with data lakes, MLOps pipelines, identity and access controls, and security monitoring—plus migration roadmaps that minimize production impact.

Financial and risk frameworks: TCO and ROI approaches tailored to sandbox programs—how to quantify time-to-insight improvements, model risk reduction, and the cost of isolation versus integrated experimentation.

Use-case catalog and prioritization tool: A sector-agnostic taxonomy of high-value sandbox use cases (model validation, synthetic-data testing, advanced analytics sandboxing) coupled with a scoring mechanism to prioritize pilots in 2026.

Vendor evaluation toolkit: A pragmatic feature checklist and vendor shortlisting methodology that emphasizes security posture, integration breadth, ease-of-use, and support for reproducible experiments. (Detailed vendor scoring matrices are contained in the full report.)

Case studies and success metrics: Practitioner vignettes that show how organizations reduced model deployment failure rates and shortened iteration cycles—presented with anonymized performance indicators to illustrate outcomes without revealing proprietary figures.

The standalone sandbox market blends platform incumbents, self-service specialists and focused sandbox vendors. PW Consulting evaluates each on capability depth, enterprise readiness, and fit for distinct buyer archetypes.

DataWalk (United States) — A purpose-built sandbox and analytics environment, DataWalk focuses on rapid data ingestion, visual exploration and prototyping in a self-contained workspace. It appeals to organizations that prioritize investigative analytics and entity-centric use cases where flexible graph-style exploration is important.

SAS Institute (United States) — With a long history in advanced analytics and regulated industries, SAS offers sandbox-capable platforms that emphasize statistical rigor, auditability and model governance. SAS is typically selected where deep analytics capabilities and compliance maturity are critical selection criteria.

Alteryx (United States) — Known for self-service data preparation and analytics, Alteryx is frequently leveraged to accelerate analyst-driven sandbox programs. Its strengths lie in rapid workflow creation, integration with enterprise data sources, and enabling non-engineer power users to prototype effectively.

Qlik (United States) — Qlik’s associative engine and visualization tooling make it a strong fit for exploratory, visualization-heavy sandbox use cases. Organizations using Qlik tend to emphasize speed of insight and intuitive data discovery for cross-functional teams.

MicroStrategy (United States) — MicroStrategy brings enterprise-grade BI and a platform mindset, enabling the creation of controlled analytical environments that can scale into productionized insights. Buyers seeking BI-led sandboxes with governance built-in often shortlist MicroStrategy.

TIBCO Software (United States) — TIBCO provides analytics and data management solutions that support both data orchestration and sandbox isolation. Its appeal is strongest among organizations that want to combine real-time integration capabilities with isolated experimentation environments.

Each vendor has distinct strengths; our detailed vendor profiles benchmark them across security, reproducibility, integration surface area, and data governance. The tactical vendor shortlists for specific buyer archetypes are only available in the full report to preserve the advisory value for commercial users.

For CIOs and CDOs: Use the staged procurement playbook to sequence investment—pilot, scale, optimize—and align sandbox programs with risk appetite and governance maturity.

For Heads of Analytics: Implement the use‑case prioritization tool to focus scarce engineering resources on experiments that yield measurable business KPIs within defined timeboxes.

For Procurement and Vendor Management: Leverage the vendor evaluation toolkit to move beyond feature checklists and evaluate vendors on integration depth, security attestations, and operational support models that reduce vendor lock-in risk.

For Security and Compliance Officers: Adopt the governance templates and audit playbooks to ensure sandboxes satisfy data protection requirements and can be demonstrated during regulatory reviews.

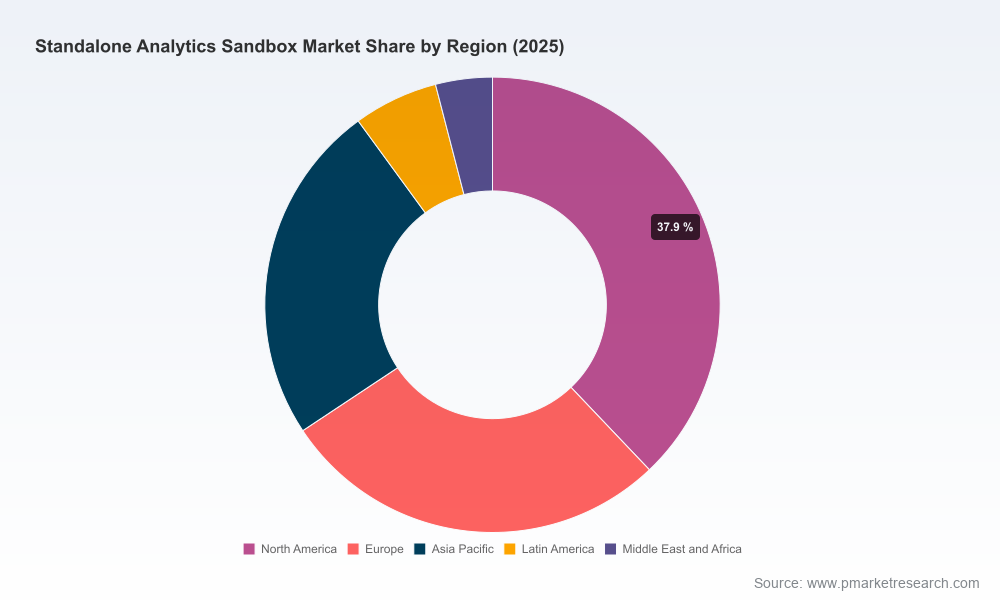

The PW Consulting study uses a base year of 2025 with a historical reconstruction covering 2020–2025 and a forecast horizon from 2026–2032. Market sizing and projection integrate bottom‑up vendor analysis, customer adoption signals and macro adoption vectors, producing a consensus growth trajectory (CAGR 16.03%). The study explicitly separates macro totals from detailed segment-level datasets; while the report maps regions, deployment models, and end-use verticals, granular segment allocations and proprietary vendor scoring matrices are gated for the full research deliverable.

Regulation: Privacy frameworks such as GDPR continue to shape how sandboxes are designed—favoring solutions that emphasize data minimization, robust access controls, and comprehensible audit trails.

Infrastructure: Effective standalone sandboxes depend on optimized cloud storage, compute orchestration and network architecture. The report includes reference infrastructure patterns that reconcile cost, latency and security requirements for enterprise adoption.

Adoption reality: Sandboxes are principally R&D and validation environments intended to protect production systems. The report provides guidance for translating sandbox outcomes into production-deployable artifacts while preserving model governance.

As enterprises enter 2026, the choice is less about whether to adopt analytics sandboxes and more about how to operationalize them in a way that accelerates insight while controlling risk. PW Consulting’s Standalone Analytics Sandbox research converts prevailing market momentum into pragmatic guidance: procurement frameworks, operational runbooks, architecture blueprints and vendor evaluation tools that C-suite and functional leaders can apply immediately. The public executive summary highlights trends, strategic implications and top-level forecasts; the full report contains the actionable playbooks, segment-level intelligence and vendor matrices that organizations will rely on to allocate capital and run pilots in 2026.

For executives ready to convert insight into action, the full report and our advisory services provide the guarded, detailed intelligence necessary to architect sandbox programs that deliver measurable business outcomes without exposing sensitive segment-level data in public summaries.

For detailed analysis of this topic, please visit the official page:Standalone Analytics Sandbox Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com