Why Panchit is the Most Exciting Upcoming Social Media App You Need Right Now

Technology |

2026-04-25 03:33:16

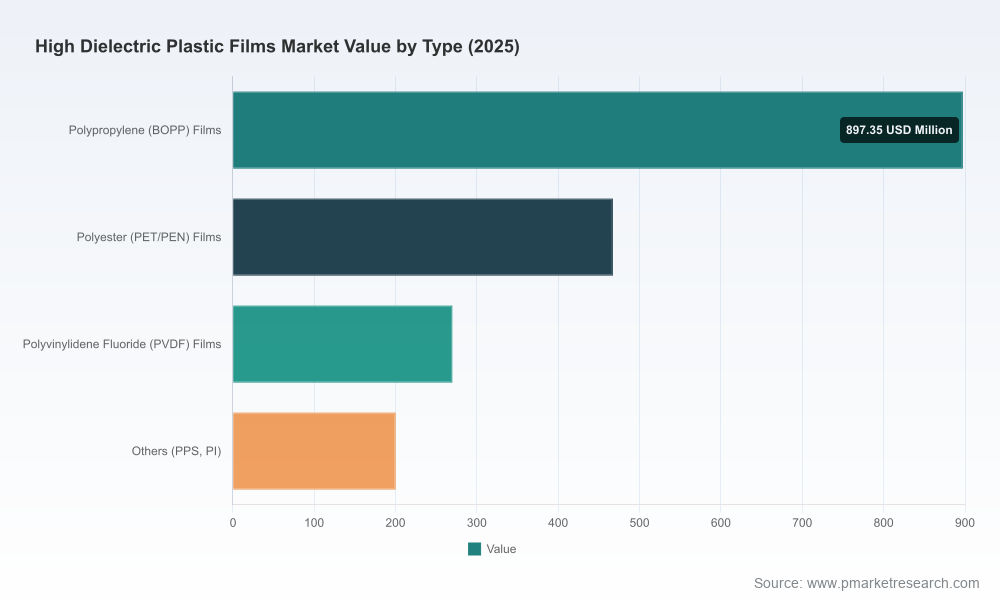

PW Consulting today publishes a new strategic study on the High Dielectric Plastic Films market, delivering a pragmatic decision-support toolkit for commercial, procurement and corporate development teams preparing for 2026. Our analysis traces the market from 2020 through 2025 and extends a detailed forecast across 2026–2032. The market expanded from USD 1,320.5 Million in 2020 to USD 1,834.77 Million in 2025, and is modeled to reach USD 1,988.79 Million in 2026, progressing to USD 2,851.21 Million by 2032. Our forecast period carries an expected compound annual growth rate (CAGR) of 6.48% (2026–2032), reflecting robust demand in power electronics, energy storage and electrified mobility applications.

High Dielectric Plastic Films Market

Timing: 2026 is a pivot year for procurement contracts, capacity planning and regulatory compliance cycles across the sector. Our market sizing and forward-looking scenarios give buyers and suppliers the clarity they need to align budgets and capital plans with realistic demand trajectories.

High Dielectric Plastic Films Market

Risk-adjusted strategy: The market is moderately concentrated (CR3 approximately 42.5%; CR5 approximately 58.8%). That structural concentration creates both supply-side resilience and single-source vulnerability — our playbooks translate that structural insight into tactical steps for risk mitigation and opportunity capture.

High Dielectric Plastic Films Market

Operational relevance: We pair top-line forecasts with actionable modules — supplier scorecards, raw-material stress tests and certification roadmaps — so commercial teams can convert insight into near-term purchasing and product decisions.

Raw material volatility: Fluoropolymer resin supply constraints — notably on tetrafluoroethylene monomer — pushed resin price inflation in the most recent year. Firms must model price pass-through, hedge exposures and identify alternative resin chemistries or blended formulations to protect margins.

Regulatory tightening: New chemical restrictions have practical consequences. For example, tighter regulatory controls on certain fluorinated substances require firms to map product formulations against REACH and similar regimes and to prepare essential-use derogation dossiers where electrical safety depends on the material.

Trade and logistics friction: Tariff measures and hazardous-goods transport classifications have real P&L impact. Heightened duties on high-tech fluoropolymer imports and IMO hazardous-material surcharges for certain film shipments increase landed costs and favor regional sourcing and inventory reconfiguration.

Product certification thresholds: Elevated dielectric constants can trigger specific certification regimes for commercial electronics. Firms developing high-permittivity films must bake compliance (including UL and comparable approvals) into development timelines to avoid market access delays.

The competitive field is a mix of material specialists, large diversified chemical groups, and targeted niche suppliers. Several strategic moves in 2024–2025 illustrate the near-term competitive pattern:

DuPont (USA) expanded capacity for high-dielectric Kapton-type films to address accelerating electronics demand. Capacity investments by incumbent suppliers shorten lead times for established film chemistries but also signal rising minimum efficient scales that new entrants must consider.

Toray Industries (Japan) launched an advanced fluoropolymer film variant targeted at EV power modules with improved breakdown voltage. Product innovation at this level raises the technical bar for application-specific suppliers and accelerates performance-driven adoption in high-voltage systems.

3M (USA) advanced certification and product-positioning activities in mid-2025, reinforcing its play in dielectric films for inverters and energy storage. Certification events should be read as market-access accelerants that drive OEM qualification timelines.

Regional specialist producers and converters (examples include Saint-Gobain, AGC Inc., Tekra/Materion, Polyflon Technology) maintain differentiated portfolios — from fluorinated polymer expertise to converter-led customizations — making them preferred partners for bespoke applications or short-lead prototypes.

Implication: incumbent scale, targeted innovation, and certification velocity are the three levers shaping supplier competitiveness. Purchasers should map suppliers across these axes when constructing preferred-supplier panels.

Our research is designed to be an execution blueprint rather than an academic overview. Key deliverables include:

Market sizing and scenario suite: historical modelling (2020–2025) and three demand scenarios for 2026–2032, with sensitivities for EV penetration, energy storage deployment and capacitor design shifts.

Supply-demand balancing engine: plant-level capacity tracking, lead-time maps and a commercial stress-test to simulate allocation impacts under disruption scenarios.

Materials risk dashboard: price drivers, alternate chemistry pathways, and a resin-sourcing decision matrix that quantifies cost and compliance tradeoffs.

Regulatory & certification heatmap: mapping of REACH-like restrictions, UL/IEC certification triggers and the procedural steps to secure essential-use derogations or equivalent approvals.

Supplier scorecards and shortlists: multi-criteria assessments that combine technical capability, capacity flexibility, commercial terms and sustainability metrics to create prioritized supplier shortlists.

Commercial playbooks: procurement negotiation templates, inventory-and-logistics configuration options under tariff and hazardous-shipping scenarios, and sample pass-through clauses for OEM contracts.

M&A and partnership screens: target characteristics and valuation heuristics for buyers seeking bolt-on technology, converter capacity or geographic diversification.

OEMs and system integrators: Re-run qualification timelines to include updated certification windows; insist on supplier roadmaps for material-substitution scenarios; include tariff contingency clauses in supply agreements.

Material suppliers: Prioritize investments that widen application envelopes (higher breakdown voltages, tailored permittivity) and accelerate third-party certifications. Consider regional mini-mills or toll-conversion partnerships to offset tariff and logistics exposure.

Procurement leaders: Implement a stratified sourcing approach — strategic dual-sourcing for mission-critical chemistries, opportunistic spot buys where standard chemistries prevail, and hedging strategies for fluoropolymer resin exposure.

Private equity / corporate development teams: Use our M&A screening matrix to identify targets that fill capability gaps (certified production lines, regional presence, or specialized fluoropolymer IP) and stress-test valuations against regulatory and feedstock risk scenarios.

In one conservative scenario modeled in the report, a sustained uptick in fluoropolymer feedstock prices combined with elevated duties and hazardous-material surcharges forces a reshuffle of global sourcing. The immediate outcomes include compressed supplier margins, longer qualification timelines for new chemistries, and an accelerated push toward regionalized inventory hubs. The result: firms that proactively reengineer bill-of-materials, lock in conversion capacity, and secure certification early realize a clear time-to-market advantage in 2026.

Integrate the supply-demand engine into your CAPEX planning to identify the earliest safe start-date for capacity expansions or new lines.

Deploy the supplier scorecards to validate Tier-1 and Tier-2 contracts, and to prioritize conversion partners for proof-of-concept runs.

Adopt the regulatory heatmap as part of product launch checklists to prevent costly market-access delays when deploying high-permittivity materials.

Leverage the M&A screens in diligence to quantify upside and downside under alternate feedstock and regulatory trajectories.

This briefing is intentionally selective — designed to communicate our strategic framing and practical value without reproducing the segmented tables and supplier-level data that clients use to make transaction-level decisions. To access the full dataset, segmented forecasts, supplier scorecards and the interactive supply-demand engine, please visit the PW Consulting report page or contact our industry team. The full report includes downloadable Excel models, scenario toggles and a decision-tree annex that operational teams can deploy directly in 2026 planning workstreams.

High dielectric plastic films are a foundational enabling material for the electrification economy. Growth is substantive and durable, but it is accompanied by legitimate commercial and regulatory friction. Companies that combine rigorous market-sizing with tactical supply-chain redesign, certification acceleration and focused product innovation will capture disproportionate value in 2026 and beyond. PW Consulting’s study equips leaders with the roadmaps, models and negotiation playbooks required to do exactly that.

For detailed analysis of this topic, please visit the official page:High Dielectric Plastic Films Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com