Middle East and Africa Animation Market: Insights, Key Players, and Growth Analysis

Other |

2026-05-26 12:05:35

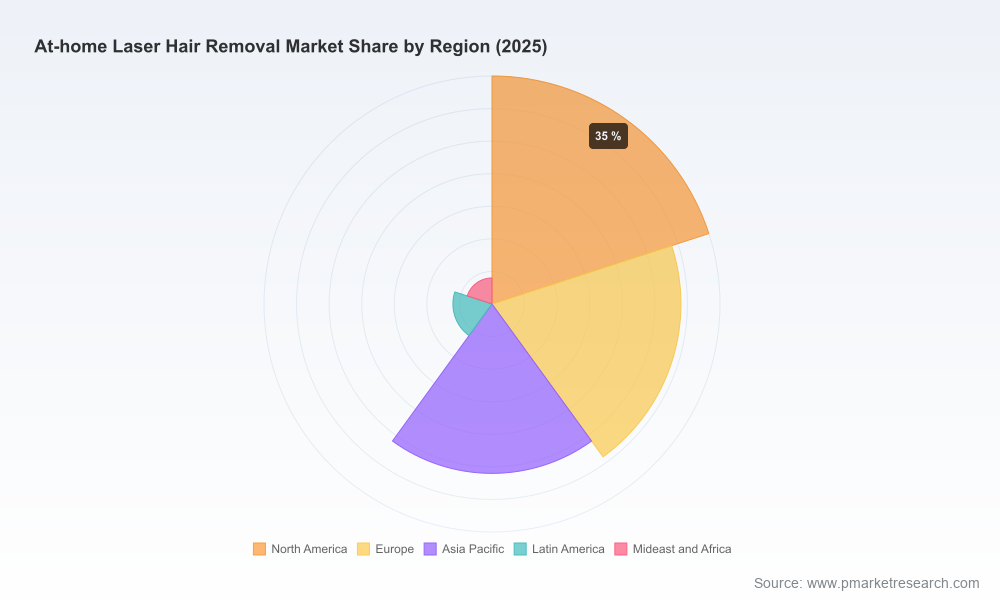

PW Consulting’s new market study on the At Home Laser Hair Removal Market offers an operationally focused, strategy-grade briefing intended to inform boardroom decisions and investment theses in 2026. The sector is no longer a niche beauty adjunct; it is an established consumer health-technology category that has demonstrated steady growth and clear pathways to scale. Our analysis places the market at approximately USD 950.0 Million in 2025 and projects steady expansion through the coming decade — reaching roughly USD 1.58 Billion by 2032 on a 7.5% compound annual growth rate (forecast period 2026–2032). These headline numbers reflect the combined force of product innovation, digital distribution, and changing consumer adoption curves that continue to favor at-home interventions for routine cosmetic care.

At Home Laser Hair Removal Market

Actionable foresight: We translate macro momentum into operational priorities you can execute in the next 6–18 months — product roadmap pivots, channel investments, and regulatory risk mitigation that materially affect 2026 P&L outcomes.

At Home Laser Hair Removal Market

Investment readiness: For private equity, corporate development and strategic investors, the report maps where returns are most likely to emerge — innovation-driven premiumization, recurring consumables/subscription models, and regional rollouts with the fastest customer acquisition economics.

At Home Laser Hair Removal Market

Competitive positioning: We provide a practical playbook for incumbents and new entrants to win share without resorting to price wars — focusing on differentiated energy platforms, safety ergonomics and software-enabled retention strategies.

Product differentiation is central. The category now supports distinct technical value propositions — from true diode laser systems designed for clinical-level energy delivery, to advanced IPL devices that optimize safe, repeatable at-home use. Consumers reward demonstrable efficacy and ease-of-use; devices that combine validated clinical performance with simple UX consistently outperform in trial-to-purchase conversion.

Digital distribution accelerates scale. Direct-to-consumer e-commerce channels drive lower CAC and enable faster iteration on bundles, subscriptions for consumables, and service-based monetization that lift lifetime value.

Consumer safety expectations shape adoption curves. Skin-sensing, cooling technology and clear contraindication guidance reduce friction and decrease warranty/complaint risk, which in turn unlocks broader addressable markets.

Regulatory clarity and enforcement are double-edged. Class II device regulation (e.g., 510(k) pathways in the U.S.) raises entry barriers — benefitting credible brands — but also increases compliance costs and time-to-market for newcomers.

Regulatory enforcement against noncompliant devices can rapidly alter competitive dynamics and channel willingness to list lower-cost SKUs.

Price-led commoditization in certain channels threatens returns unless mitigated by service, warranty, or ecosystem-based differentiation.

Technological misconceptions among consumers (e.g., conflating device types and expected speed-to-results) amplify returns for brands that invest in clear clinical communication.

The category is occupied by a mix of consumer-electronics incumbents, specialized medtech players, and agile regional brands. Competition is best understood as differentiated by core technology, go-to-market model, and brand trust. Key industry participants include brands that represent each of these vectors of competition — from companies offering FDA-cleared diode lasers to leading consumer-electronics firms that scale via household distribution and broad marketing reach.

Technology-led players: Firms offering diode laser technology position themselves on clinical efficacy and “professional-grade” messaging. Their value lies in higher energy delivery and clinical differentiation that can command premium pricing and a loyal user base.

Consumer-electronics incumbents: Large established brands have strengths in retail distribution, brand recognition, and cross-category marketing. Their advantage is scale — rapid placement in mass retail and online marketplaces, and the ability to bundle with adjacent beauty devices.

Fast-follow innovators: Emerging brands achieve traction by optimizing comfort (cooling), reducing treatment times, or targeting under-addressed consumer segments (e.g., male grooming, diverse skin tones).

Recent product activity underscores how vendors are jockeying for differentiation: few companies have launched new home devices with high flash counts and improved skin-tone sensors in the last 12–18 months, while others continue to showcase refined hardware iterations and retail-ready designs. These market movements validate PW Consulting’s thesis that 2026 will reward brands that combine verifiable performance with consumer-centric ergonomics.

Regulations matter operationally: At-home IPL and laser devices are regulated as medical devices in several major markets, and compliance affects labeling, clinical claims and distribution. Companies should budget upfront for regulatory strategy, which includes 510(k)-type clearances where applicable and ongoing post-market surveillance.

Enforcement is real: Recent regulatory actions against unregistered or misbranded devices serve as a caution. Noncompliant manufacturers expose channel partners to risk and can face recalls, damaging both brand equity and retailer relationships.

Design for safety: Skin-tone sensors, energy caps for home use, clear contraindication guidance, and robust customer support systems are not optional — they materially influence return rates, adverse event incidence, and long-term brand trust.

Integrated market model with yearly topline estimates (2020–2025 historical base and a 2026–2032 forecast path), scenario analyses and sensitivity to key variables such as unit ASP, replacement cycle and consumable penetration.

Commercial playbooks: SKU architecture recommendations, pricing ladders, bundling tactics and channel mix optimization for maximizing 2026 customer acquisition efficiency and lifetime value.

Regulatory and safety playbook: Pathways to clearance, recommended clinical evidence packages, labeling best practices, and post-market surveillance frameworks designed to satisfy major regulators and reassure retail partners.

Technology and product evaluation: Head-to-head benchmarking criteria (energy platform, cooling, flash count, sensor fidelity) and a roadmap for R&D prioritization tied to five-year ROI estimates.

M&A and partnership opportunities: A prioritized list of target archetypes, valuation benchmarks, and integration risk checklists to accelerate inorganic growth while preserving customer retention.

Retailer and channel playbook: Operational guidance for DTC, marketplace and mass-retail launches, including promotional cadence, warranty structures and omnichannel fulfillment considerations.

Manufacturers: Prioritize clinical differentiation or price leadership — do not attempt both without deep pockets. If choosing premium, ensure FDA/CE-style clearances and invest in outcome-based marketing. If choosing value, secure compliant supply chains and defensive channel agreements.

Retailers & e-tailers: Curate assortments by certifying compliance and clinical claims; favor partners who provide clinical evidence and strong post-sale support to minimize returns and regulatory exposure.

Investors & corporate development teams: Target asset-light brands with strong DTC unit economics or bolt-on technologies that improve device efficacy (e.g., cooling modules, sensor software). Prepare for a market where consolidation will be driven by technology consolidation and distribution scale.

Clinics & professional partners: Leverage at-home devices as retention tools and cross-sell anchors while emphasizing in-clinic services for faster or more intensive workflows; channel partnerships with consumer brands can be a revenue-bearing distribution route.

Our research blends rigorous top-down sizing with practitioner-focused bottom-up unit economics. The forecasting framework explicitly models how product innovations, regulatory timelines and channel mix changes impact revenue and margin pathways through 2032. While this summary highlights the strategic contours, the full report contains the granular dashboards and segmentation matrices decision-makers need to operationalize these insights.

This release is a strategic preview designed to surface the highest-impact findings. To access the complete datasets, scenario models, vendor scorecards and playbooks referenced here — including downloadable financial models and go-to-market templates — please visit our report landing page. The full report provides the segmented tables and raw model assumptions that are essential for transaction diligence, product planning and channel negotiations in 2026.

The At Home Laser Hair Removal Market is maturing from a technology novelty into a repeatable, serviceable consumer-health revenue stream. For 2026 strategy cycles, winners will be those who translate clinical credibility into scalable commerce, while avoiding regulatory missteps and commoditization traps. PW Consulting’s report is built to be the operational guidebook for that transition.

For detailed analysis of this topic, please visit the official page:At Home Laser Hair Removal Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com