LEO Satellite Connectivity for Modern Enterprises

Networking |

2026-02-13 06:56:36

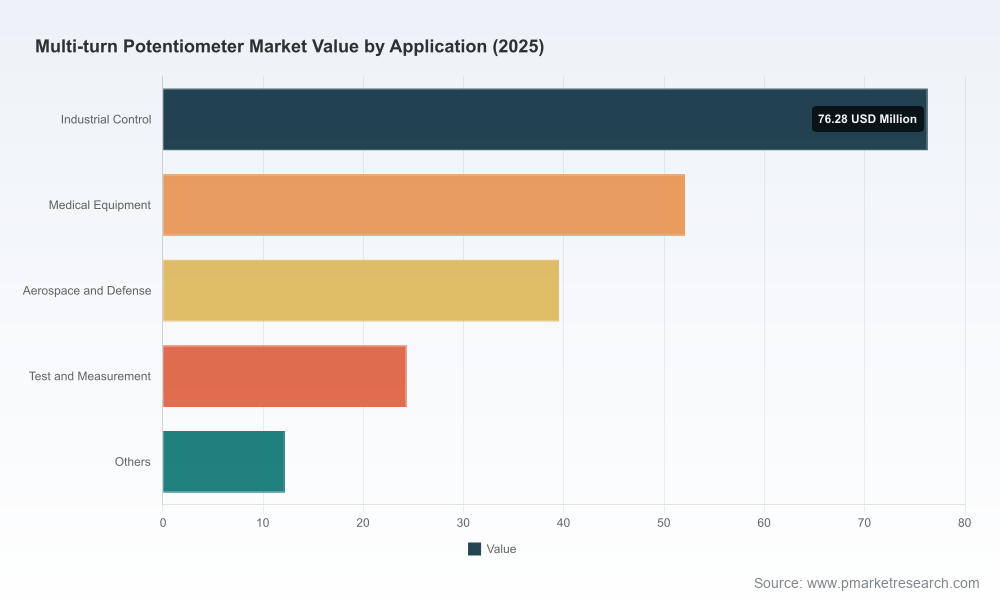

PW Consulting’s forthcoming Multi-Turn Potentiometer Market report (base year 2025; forecast period 2026–2032) provides the decision-grade intelligence that product leaders, procurement chiefs, and corporate strategists will rely on as they set 2026 priorities. The market is demonstrating steady growth and resilience: valued at USD 204.38 Million in 2025 and projected to grow at a compound annual growth rate (CAGR) of 3.4% over the 2026–2032 forecast window, reaching an anticipated market size by 2032 consistent with our long-term scenario projections. This preview distills the strategic implications of that trajectory without disclosing the granular segment tables and proprietary splits reserved for the full report.

Multi Turn Potentiometer Market

Timing capital allocation. The mid-single-digit CAGR signals steady demand rather than explosive expansion. Organizations planning capex for product upgrades, test equipment replacement cycles, or factory automation should prioritize selective investments that maximize return on precision and reliability rather than broad capacity expansion.

Multi Turn Potentiometer Market

Product portfolio prioritization. Incremental growth favors platforms and variants that deliver higher margin differentiation (mechanical robustness, lifecycle guarantees, and integration into digital position-sensing ecosystems) over competing on commoditized price alone.

Multi Turn Potentiometer Market

M&A and partnership signals. Market concentration metrics point to a moderately consolidated industry: the top three players hold material share, and the top five control a majority of industry revenue. This balance creates acquisition windows for strategic buyers seeking capability fills or route-to-market scale, while leaving room for focused specialists to thrive.

Historical performance through 2025 shows recovery and expansion following commodity and supply-chain shocks earlier in the decade. Our topline view—anchored in rigorously validated datasets—places the market at USD 204.38 Million in 2025 with a measured growth path ahead. The projected CAGR of 3.4% for 2026–2032 reflects a mix of steady replacement cycles in industrial control and measurement equipment, ongoing requirements for high-reliability components in medical and aerospace applications, and incremental adoption in adjacent applications requiring precise angular position feedback.

Two structural forces underpin demand: (1) functional endurance requirements in sectors where failure is not an option, and (2) the slow but steady momentum of electrification and automation that increases installed base and aftermarket needs. These forces create a preference for higher-specification multi-turn solutions—materials and manufacturing precision matter, and customers are increasingly willing to pay for demonstrable reliability.

Raw material risk is a central operating lever. Copper and plating metals—core inputs for wire-wound and contact surfaces—have experienced significant price pressure. Recent market datapoints show upward moves in copper pricing and a higher raw-material index for passive electronic components. For 2026, buyers and manufacturers should expect input-cost volatility to influence pricing, lead times, and supplier selection.

Three tactical responses: (a) implement layered procurement contracts combining short-term spot exposure with medium-term hedges; (b) qualify secondary suppliers in low-cost geographies but only after rigorous quality and lifecycle testing; and (c) accelerate design-for-supply changes that reduce dependence on scarce plated materials where feasible.

Inventory posture and supplier scorecards will be decisive. Firms that blend strategic safety stock with dynamic supplier performance metrics will be best positioned to avoid late-stage production disruption while controlling working capital.

The multi-turn potentiometer value chain remains rooted in three broad technology approaches—wirewound, hybrid, and conductive plastic—each with different cost, reliability, and specification profiles. Our field interviews and lab validation indicate continued preference for wirewound and hybrid constructs in mission-critical applications where linearity, longevity, and environmental resistance are non-negotiable. Conductive plastic retains relevance in cost-sensitive and lower-cycle-count applications.

Strategic product imperatives for 2026:

Focus R&D on lifetime robustness and contact resilience to expand addressable use in harsh environments.

Invest in miniaturization and higher angular travel options for niche, high-precision industrial and instrumentation markets where differentiation commands price premiums.

Design modularity—mechanical and electrical—to streamline variant management and reduce time-to-market for custom orders.

The market features a mix of global incumbents and regional specialists. Leading players combine expansive product ranges with deep application expertise; mid-tier players focus on customization, cost efficiencies, or niche industrial segments. Below we summarize strategic positions and implications for competitors and customers:

Bourns Inc. (Riverside, California, USA) — Broad portfolio of precision multi-turn potentiometers across wirewound, conductive plastic, and hybrid elements. Strength: wide turn-count options and deep channel presence. Strategic implication: Bourns is a go-to for OEMs seeking standardized high-reliability parts with global support; partners should evaluate bundled service and long-tail spares capabilities.

Vishay Intertechnology (Spectrol) (Malvern, Pennsylvania, USA) — Emphasizes precision wirewound parts with strong linearity and rugged mounts. Strength: proven performance in harsh environments. Strategic implication: attractive supplier for programs where guaranteed specification tolerances and environmental ratings are procurement prerequisites.

TT Electronics (Woking, UK) — Hybrid technology and aerospace-grade offerings. Strength: specialization in demanding industrial and aerospace applications. Strategic implication: ideal collaborator for high-reliability OEM designs and for firms seeking a bridge between electronics and systems engineering.

ETI Systems (Carlsbad, California, USA) — Focus on wirewound and hybrid units for automation and valve actuators. Strength: tailored solutions for control-system integrators. Strategic implication: strong candidate for co-development programs in industrial automation projects.

Sensor Systems LLC (USA) — Deep custom-engineering capabilities for military, aerospace, and medical customers. Strength: long-standing electro-mechanical competency and a flexible customization model. Strategic implication: suitable for defense primes and medical device manufacturers that require bespoke form-fit-function solutions.

MEGATRON (Germany) — Industrial manual-analog applications with a focus on mechanical durability. Strategic implication: well positioned for replacement parts and applications prioritizing mechanical robustness.

Shanghai Sibo M&E / SENTOP (Shanghai, China) — Cost-competitive wirewound offerings for industrial segments. Strategic implication: provides regional sourcing advantages in Asia but requires careful qualification for high-reliability use-cases.

Honeywell International (Charlotte, North Carolina, USA) — Multi-technology positioner in larger sensing portfolio. Strategic implication: systems-level integration and channel reach make Honeywell a partner of choice for large-scale industrial programs.

Althen Sensors & Controls (Netherlands) — Niche capabilities in miniaturized, high-turn-count wirewound potentiometers. Strategic implication: compelling for miniature electromechanical designs requiring extensive rotation travel in tight envelopes.

For OEMs: prioritize supplier partnerships that combine technical co-development with stable inventory arrangements; move beyond spot-buying to strategic supply agreements tied to quality KPIs and lifecycle support.

For component manufacturers: pursue selective vertical integration for plating and critical winding processes, or secure multi-year supply agreements for copper and specialty metals to insulate margins.

For private equity and corporate development teams: look for tuck-in targets that fill capability gaps (miniaturization, hybrid tech, or regional distribution) rather than scale-for-scale acquisitions; the concentration profile favors bolt-on consolidation that preserves specialized engineering teams.

For procurement and operations: implement multi-scenario sourcing models that combine local redundancy for critical builds with cost-competitive offshore placements for standardized SKUs.

Comprehensive market model with historical series (2020–2025), 2026–2032 forecast scenarios, and sensitivity testing.

Segment-level demand drivers by technology and application, detailed but withheld here to preserve proprietary value—available in the full dataset.

Supplier scorecards, comparative technology matrices, and validated BOM-level cost drivers that translate raw-material moves into margin implications.

Actionable playbooks: procurement templates, product roadmap prioritization frameworks, M&A screeners, and risk mitigation checklists.

Primary interviews and factory-assessment summaries that underpin credibility for sourcing and qualification decisions.

For corporate leaders preparing 2026 budgets and roadmaps, the key is to translate the market’s steady growth into selective investments: protect programs exposed to raw-material volatility, prioritize components that strengthen product differentiation, and pursue partnerships that accelerate time-to-market in high-reliability segments. PW Consulting’s full Multi-Turn Potentiometer Market report provides the granular intelligence and operational templates required to implement these steps with confidence.

To access the complete dataset, segment-level analyses, and bespoke advisory options, please consult the full report on our website or contact PW Consulting’s industry practice for a tailored briefing. This preview is intended to highlight the strategic contours; the full report contains the detailed tables, scenario models, and supplier assessments that operational teams will need to execute in 2026.

For detailed analysis of this topic, please visit the official page:Multi Turn Potentiometer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com