The Rise of Natural-Looking Dermal Fillers: Why “Undetectable Beauty” Is Replacing Overfilled Faces

Health |

2026-06-11 09:28:11

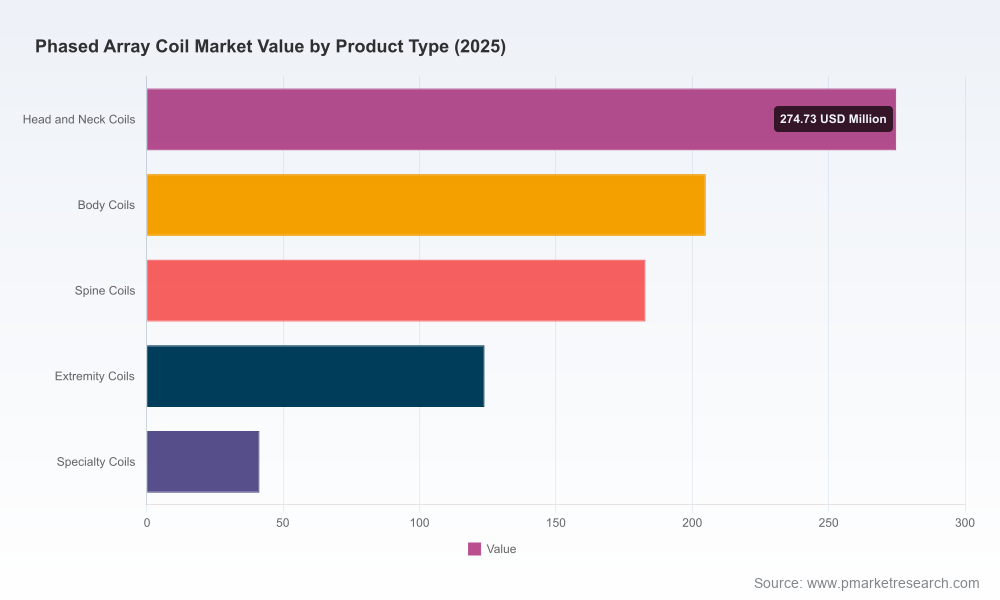

PW Consulting’s latest market study on Phased Array Coils provides an operationally focused roadmap for healthcare providers, OEMs, component suppliers, and investors as they plan for 2026 and beyond. Our analysis—which covers historical performance from 2020–2025 and provides a 2026–2032 forecast—shows a resilient market expanding at a compound annual growth rate (CAGR) of 6.32%. The global market size is projected to grow from approximately USD 827.5 Million in 2025 to about USD 1,270.8 Million by 2032. This trajectory reflects sustained adoption of multi-channel receive technology across clinical and research modalities, incremental product innovation, and rising procedural intensity in imaging portfolios.

Phased Array Coil Market

Operational inflection: Hospitals and imaging centers are shifting from one-off coil purchases to portfolio-level strategies that prioritize lifecycle cost, serviceability, and cross-platform interoperability. Procurement cycles that begin in 2026 will determine installed-base configurations for much of the coming decade.

Phased Array Coil Market

Regulatory and reimbursement crosswinds: 2025–2026 regulatory activity—particularly ongoing enforcement around FDA 510(k) pathways for receive coils and IEC safety standards for MRI systems—means that products introduced or refreshed in 2026 must be validated against a stricter environment. Simultaneously, jurisdictions with favorable reimbursement for high-resolution MRI procedures are demonstrating materially higher adoption rates, amplifying the commercial upside for compliant, high-channel-count solutions.

Phased Array Coil Market

Technology consolidation: Vendors are moving from single-product differentiation to platform strategies that bundle coil innovations (flexible arrays, ultra-high-density elements, dual-tuned coils) with software-enabled workflow advantages. Decisions made in 2026 should therefore assess both hardware performance and software/service interoperability.

Think portfolio, not piece: Capital planning must treat phased array coils as modular ecosystems. Total cost of ownership (TCO) analyses that include repair/refurbishment cycles, cross-vendor compatibility, and upgrade pathways deliver materially different outcomes than one-off price comparisons.

Prioritize compatibility and validation: Third-party and custom coils can unlock cost and ergonomics gains, but clinical rollout requires rigorous OEM compatibility validation and regulatory clearances. Build a short-list of suppliers with proven 510(k)/CE track records and documented cross-platform performance metrics.

Design for patient and workflow impact: Lightweight flexible arrays and pediatric-focused designs are shifting throughput and patient satisfaction metrics. Operational buyers should model efficiency gains from reduced scan times and fewer repeat exams when evaluating next-generation coil investments.

Embed regulatory readiness into procurement: New purchases should include supplier commitments on ongoing regulatory support (e.g., documentation for substantial equivalence, SAR testing compliance). This reduces downstream clinical risk and protects reimbursement pathways.

The market remains anchored by major OEMs and a growing set of specialized innovators and contract manufacturers. Incumbent system providers continue to offer integrated coil portfolios optimized for their scanner platforms, while agile specialists deliver targeted innovations that accelerate adoption in niche applications.

System OEMs: Established imaging OEMs provide integrated phased array receive solutions that leverage platform-level advantages—high-channel-count arrays, flex coil families, and clinical workflows tuned to their 1.5T and 3T systems. Their breadth of installed bases and system-service bundles remain a primary purchasing consideration for large hospital networks.

Innovators and specialists: A cohort of smaller firms has demonstrated rapid product development, focusing on ultra-lightweight flexible arrays, pediatric comfort designs, and dual-tuned capabilities for combined proton/non-proton imaging. These players are increasingly securing regulatory clearances for targeted coils and forming partnerships to reach major scanner platforms.

Contract manufacturers and refurbishers: Outsourced production and lifecycle service providers offer cost-efficient manufacturing, repair, and refurbishment options—critical levers for health systems managing capital budgets and sustainability goals.

Notable vendor activity in the past 18 months validates these dynamics: flexible pediatric arrays and lightweight small-body coils received regulatory clearances and product launches; manufacturers expanded high-density arrays for 3T platforms and dual-tuned head coils to enable multimodal research. These developments underscore how incremental coil innovations drive clinical differentiation even in mature MRI installations.

Device classification and approvals: Receive coils are regulated under established medical device frameworks; in the U.S., many designs proceed through FDA 510(k) pathways requiring demonstration of substantial equivalence. Expect procurement contracts in 2026 to demand clear regulatory traceability and vendor support commitments.

Standards and safety: Compliance with MRI-specific safety standards—including SAR limits during parallel imaging and IEC 60601-2-33 conformance—remains non-negotiable. Buyers should insist on third-party validation data and clear statements of compliance in technical submissions.

Reimbursement sensitivity: Our sector analysis finds that jurisdictions with supportive reimbursement policies for advanced MRI procedures exhibit markedly higher adoption of multi-channel phased array coils. Investment cases that model reimbursement-linked volume uplift will be persuasive to hospital CFOs.

The report is designed as an execution tool for 2026 planning cycles. It combines market sizing and forecast rigor with applied frameworks and checklists that stakeholders can use immediately:

Validated market sizing (historical 2020–2025, forecast 2026–2032) and a quantified growth model that isolates demand drivers across clinical, research, and service segments.

Procurement playbook covering vendor selection criteria, interoperability test matrices, total cost of ownership templates, and contract clauses to mitigate regulatory and compatibility risk.

Technology roadmap outlining near-term innovation vectors—flexible materials, channel-count economics, dual-tuned designs, and software-enabled coil management—and their expected impact on clinical KPIs.

Competitive intelligence dossiers on leading system OEMs and specialized coil manufacturers, including product positioning, regulatory milestones, and partnership strategies.

Regulatory and compliance checklist aligned to IEC and FDA expectations, with practical guidance on documentation and testing requirements for clinical deployment.

Service and aftermarket playbook for supply chain managers, including repair/refurbishment benchmarks, qualification protocols for contract manufacturers, and strategies for circular-economy initiatives.

Scenario-based financial models and sensitivity analyses to stress-test procurement decisions against variations in adoption rates, reimbursement changes, and technological obsolescence.

For hospital systems: Establish a three-year coil modernization roadmap that phases investments to capture both ergonomic gains and modality upgrades. Prioritize suppliers that can demonstrate cross-platform validation and robust service guarantees.

For imaging OEMs: Invest in open-interface strategies that ease integration of third-party arrays while protecting clinical differentiation through firmware and workflow integration.

For suppliers and innovators: Focus on regulatory-compliant modular designs and pursue targeted 510(k) clearances that expand addressable markets (e.g., pediatric, cardiac, non-proton imaging). Strategic alliances with system OEMs accelerate market access.

For investors and M&A teams: Evaluate targets based on pipeline regulatory readiness, IP protection around element density and flexibility, and service capabilities—these attributes predict defensible growth and attractive margin expansion as adoption scales.

Decisions made in 2026 about phased array coil procurement, development, and partnerships will echo through imaging operations and P&Ls for years. Our study combines granular, vendor-level insight with hands-on decision tools: it translates market growth projections into concrete procurement and R&D actions. The market’s steady CAGR of 6.32% and the forecasted expansion to roughly USD 1.27 billion by 2032 create a clear runway—but realizing that potential requires disciplined product validation, interoperability-first procurement, and reimbursement-aligned deployment strategies.

PW Consulting’s full Phased Array Coil Market Report includes the detailed datasets, vendor matrices, and proprietary models that underpin the analysis summarized here. To access the complete segmentation tables, scenario models, and supplier dossiers that operational teams will use to finalize 2026 action plans, please visit the report page on our website.

For detailed analysis of this topic, please visit the official page:Phased Array Coil Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com