Prescription Dermatology Therapeutics market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-05-21 14:47:13

PW Consulting’s latest market study on Coco Amine Ethoxylate provides an executive-grade lens on a maturing specialty surfactants market as companies enter a pivotal 2026 planning cycle. Anchored to a 2025 base year, the global market has demonstrated steady expansion from the early 2020s and, under our central-case forecast, is projected to grow at a compound annual growth rate (CAGR) of approximately 5.5% through the 2026–2032 horizon. From a strategic perspective, that trajectory signals durable end‑market demand and creates a window for selective investment, portfolio reshaping, and supply‑chain re‑engineering—provided stakeholders act with calibrated priorities and near-term agility.

Coco Amine Ethoxylate Market

Coco amine ethoxylates occupy an intersection between commodity surfactants and specialty functional additives. Demand is driven by several structural factors: the ongoing need for efficacious adjuvants in crop protection formulations, performance improvements in textile processing auxiliaries, and formulation shifts across personal care, home care, and industrial cleaning where cost-to-performance ratios and regulatory compliance matter.

Coco Amine Ethoxylate Market

Macro demand growth through our forecast window reflects both volume expansion and value uplift as higher‑performance EO grades and tailored formulations gain traction in developed and emerging markets. At the same time, cyclical and structural cost pressures—centered on coconut oil, the primary upstream feedstock—introduce a persistent layer of margin risk. Notably, global coconut oil benchmarks and country‑level spikes over 2025–early‑2026 underscore the necessity for robust procurement playbooks (see later section for mitigation tactics).

Coco Amine Ethoxylate Market

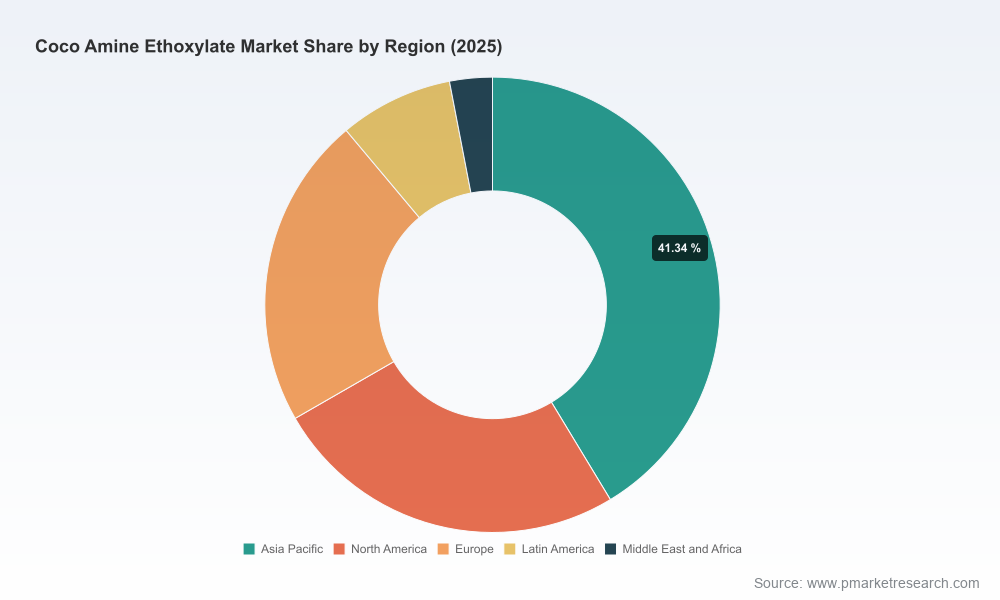

The market exhibits moderate concentration: the three‑player aggregated share sits well below the levels seen in highly consolidated chemistries, while a five‑player block captures a majority portion of the market—enough to influence pricing and commercial terms, but insufficient to eliminate opportunities for nimble challengers. That structure produces predictable outcomes:

Key industry participants profiled in the report include long‑established specialty chemical producers and a cohort of regional manufacturers and exporters. These firms differ along three strategic axes: product breadth (range of EO degrees and finished formulations), channel footprint (direct sales vs distribution), and value‑chain positioning (manufacturing scale vs contract/toll capacity). Tactical implications are clear—global players will focus on premium applications and compliance, while regional players will compete on cost and agility.

Procurement teams must manage two parallel risk sets. First, feedstock volatility: coconut oil, a primary upstream input, has experienced pronounced price swings that materially affect COGS for coco amine ethoxylates. These swings have regional nuances that affect supplier economics and arbitrage patterns. Second, logistics and regulatory constraints: transport classification and safety documentation for amine ethoxylates create handling and storage requirements that raise logistics complexity (for example, established transport categorizations for amine-based formulations and environmental hazard notations are active considerations for shippers and formulators).

On regulation, coco amine ethoxylates presently do not meet PBT or vPvB criteria under prevailing EU‑aligned frameworks, which reduces one layer of regulatory exposure relative to other surfactants; nevertheless, increased scrutiny around biodegradability, aquatic toxicity in agrochemical uses, and supply‑chain traceability (sustainable feedstocks) are emerging themes that will shape procurement specifications and market access over the medium term.

With mid‑single‑digit CAGR expansion and structural headwinds from feedstock cost volatility, companies should prioritize moves that combine defensive resilience with selective growth capture. Below are five recommended actions for leadership teams:

From the profiles in our study, several tactical themes emerge that leaders should monitor:

Our Coco Amine Ethoxylate market study is crafted as a decision‑support tool. Beyond the macro numbers and competitor dossiers, the report includes supplier scorecards, procurement playbooks, and a commercialization checklist designed for immediate use in boardroom deliberations and procurement negotiations. For companies preparing capital allocation requests, the report’s sensitivity dashboards and scenario outputs provide the evidence base required to defend investment theses to internal and external stakeholders.

For practitioners who want to move from strategic intent to operational execution in 2026, PW Consulting offers tailored advisory: rapid supplier due‑diligence, procurement renegotiation support, and M&A target screening informed by our proprietary scoring. The full dataset and actionable segment-level tables—reserved for subscribers—contain the granular inputs needed to build PE‑grade investment models or detailed GTM playbooks.

To unlock the complete intelligence set, including the segment tables, supplier scorecards, and our full scenario models, please consult the full report page. PW Consulting’s Coco Amine Ethoxylate Market study is positioned to be the single authoritative reference for firms that intend to convert 2026 market dynamics into durable competitive advantage.

For detailed analysis of this topic, please visit the official page:Coco Amine Ethoxylate Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com