Fairdeal - Fast Access Platform For Trusted Live Cricket Betting Entertainment And Predictions

Games |

2026-06-01 13:12:50

PW Consulting today publishes an executive briefing drawn from our new Biomass for Power Generation Market report, a decision-grade intelligence product tailored for corporate strategy teams, investors, and policy advisers preparing for 2026. Grounded in a detailed historical reconstruction (2020–2025) and forward-looking scenario modeling to 2032, the report frames a market that has expanded from a multi-decade baseline into a renewed growth phase. Our base-year estimate for 2025 places the global market at USD 111.8 Billion, and our central forecast sees it rising to approximately USD 178.0 Billion by 2032 — a compound annual growth rate of 6.89% across the forecast window. This briefing highlights the strategic implications of those dynamics while reserving the granular segment tables and project-level data for report subscribers.

Biomass For Power Generation Market

Timing matters: 2026 is shaping up as an inflection year. Policy windows, capital allocation cycles, and project lead times converge — companies that finalize strategic choices in 2026 will capture the most favorable incentives and first-mover advantages in the next five years.

Biomass For Power Generation Market

Investment sizing and risk appetite: with a mid-single-digit CAGR and meaningful upside scenarios, the market supports both brownfield conversions and greenfield builds, but returns are highly sensitive to feedstock sourcing, carbon accounting, and long-term offtake arrangements.

Biomass For Power Generation Market

Portfolio alignment: energy and industrial players must decide whether biomass will be deployed primarily for baseload renewable power, combined heat and power (CHP), or as a bridge to low-carbon fuels and carbon removal value chains.

Robust market architecture: a consolidated global market size (2020–2025) and probabilistic forecasts (2026–2032) including base, upside, and stress scenarios.

Project-level mapping: anonymized pipeline analysis and project readiness scoring to help prioritize pursuit lists and divestiture candidates.

Commercial playbooks: contract templates, feedstock procurement strategies, offtake structuring alternatives, and sensitivity-tested LCOE models tailored to common plant configurations.

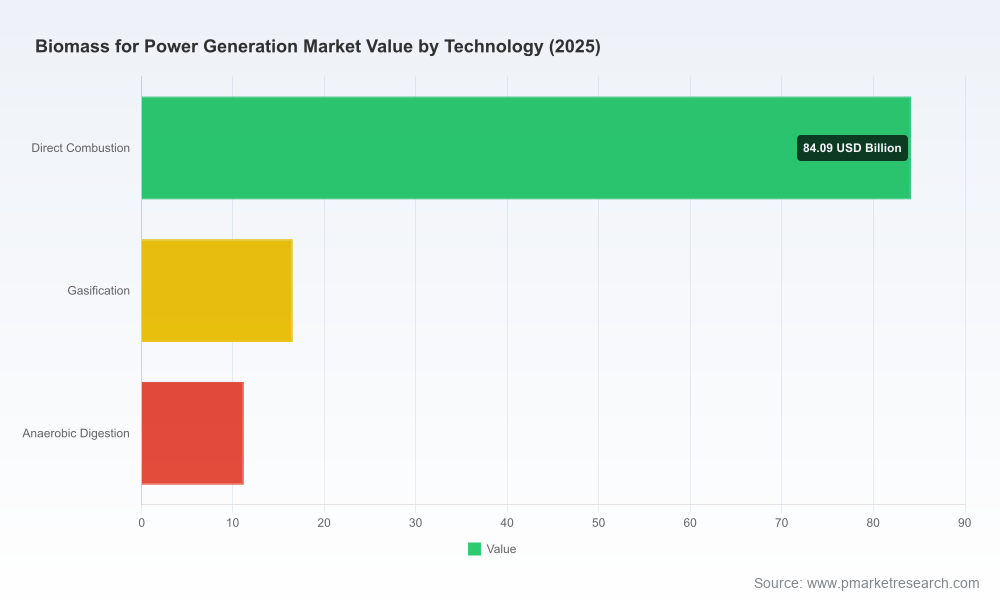

Technology and CAPEX/OPEX benchmarking: vendor scorecards, retrofit cost ranges, and comparative economics of direct combustion, gasification and anaerobic digestion pathways.

Regulatory heatmap and subsidies tracker: jurisdictional analysis for incentive qualification, including criteria likely to affect tax credit eligibility and carbon accounting requirements.

Competitive intelligence: profiles and strategic positioning of leading incumbents and system suppliers, with a focus on partnership synergies and supply-chain exposure.

The market’s recovery and subsequent growth reflect three reinforcing forces: policy-driven incentive alignment, continued commercial interest in coal-to-biomass conversions, and a steady uptick in demand from industrial CHP and distributed generation projects. Our modeling captures a compound trajectory that lifts the market from a mid-sized base in 2025 to a materially larger opportunity set by 2032. While headline growth is attractive, the value lies in where and how that growth materializes — and in the differentiated economics between low-transport-density, locally supplied projects and high-capex, large-scale export-oriented pellet value chains.

Policy tailwinds: Several jurisdictions have expanded technology-neutral clean electricity incentives and are revising eligibility rules for biomass in tax and subsidy frameworks. These policy moves materially affect project IRRs and, crucially, the carbon accounting frameworks that underpin investment approval.

Carbon policy and CCUS: Emerging proposals to broaden carbon-capture tax credits and to incentivize forest-residue products for wildfire mitigation create optionality for biomass projects that integrate capture or supply-chain interventions.

Feedstock and logistics risk: feedstock availability, densification capacity, and transport costs remain the primary determinants of merchant-scale economics. Expect greater vertical integration and strategic JV formation between power producers and pellet/densification suppliers.

Technology mix and retrofit economics: direct combustion continues to dominate deployed capacity due to maturity and relative simplicity of retrofit. Nevertheless, gasification and anaerobic digestion are attracting targeted investment for niche applications and where policy rewards higher lifecycle GHG performance.

The sector shows a mix of large utilities, specialist biopower operators, EPCs, and equipment suppliers — a landscape that remains fragmented at the top. Market concentration metrics indicate room for consolidation and strategic alliances rather than dominant scale by a handful of players. Our analysis of leading firms provides directional insights:

Drax and major European utilities: companies that combined plant ownership with pellet production exemplify the vertical integration playbook. They prioritize feedstock control, price stability, and lifecycle verification to defend market access under tightening GHG rules.

Large utilities transitioning from coal: several incumbent utilities accelerate coal-to-biomass conversions as a near-term route to decarbonize baseload assets. These projects are capital-intensive but leverage existing grid connections and community relationships.

Equipment and EPC suppliers: global engineering firms and boiler specialists are competing on retrofit expertise and performance guarantees. Their value proposition increasingly includes fuel-flexible designs and CCUS-readiness options.

Regional developers and new entrants: a wave of regional project developers in Asia and Latin America is deploying smaller-scale plants tied to agricultural residues and mill by-products, increasing the addressable market and creating acquisition targets for global players.

Recent industry developments — from new plant commissioning in Asia to densification plant investments in Southeast Asia and announcements of mill self-sufficiency projects in Europe — underscore the geographic breadth and technological diversity of current activity. These moves also foreshadow the two-tier market reality: large transnational projects anchored by pellet supply chains and a parallel landscape of localized projects focused on circular feedstock streams.

Rebaseline supply-chain risk: map concentration, seasonality and densification capacity across all prospective feedstock sources; price risk should be modeled under at least three transport and policy scenarios.

Pursue staged decarbonization: design projects with retrofit and CCUS modularity to avoid stranded assets as lifecycle GHG metrics evolve.

Lock in price-flexible offtakes: negotiate contracts that balance long-term stability with indexed clauses to protect against feedstock and carbon-price volatility.

Prioritize verification and LCA: invest early in third-party sustainability certification and transparent lifecycle analysis to ensure eligibility for emerging tax credits and corporate procurement standards.

Consider JV models with densifiers and pellet producers: shared ownership of upstream processing can improve margin capture and reduce delivery risk.

Screen M&A targets strategically: seek smaller regional developers with operating permits and local fuel access, and select OEMs with retrofit IP.

Align finance to policy timelines: structure financing to capture available incentives and safeguard against mid-term policy reversals through covenant design and step-in clauses.

Comprehensive regional demand forecasts and sensitivity runs (2026–2032), with scenario toggles for feedstock price, transport cost and policy shifts.

Detailed supplier and EPC scorecards, with techno-economic benchmarks and retrofit cost ranges.

Project-level pipeline, readiness scores, and opportunity maps for strategic M&A and partnership pursuit.

Policy and incentives dossier, mapping eligibility criteria, compliance pathways, and near-term legislative risks that will affect bankability.

Customized advisory annexes: one-page investment memos, bid/no-bid decision frameworks, and an operational due-diligence checklist for developers and investors.

Biomass for power generation is neither a simple substitute nor a temporary stopgap; it is a strategic option whose attractiveness depends on the interplay of policy, provenance, and project design. For leaders charting their 2026 strategies, the imperative is to blend speed with optionality: secure supply and incentives now, but structure assets to adapt to stricter lifecycle GHG expectations and the potential for CCUS integration. PW Consulting’s full report translates market sizing and scenario analytics into executable moves — from procurement playbooks to M&A screening — enabling clients to convert headline growth into durable return streams.

To access the full dataset, detailed segment analysis, and project-level intelligence referenced in this briefing, visit PW Consulting’s report portal or contact our industry team for a tailored briefing and licensing options.

For detailed analysis of this topic, please visit the official page:Biomass For Power Generation Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com