The Rise of Industrial Noise Control Market Industry Trends and Innovations

Other |

2026-05-12 09:28:35

PW Consulting’s latest market study on the 24 Hour Emergency Roadside Assistance market delivers a concise, high-signal briefing intended to inform boardroom decisions as organizations enter 2026. This press release summarizes the report’s strategic implications and operational playbooks without revealing the proprietary segment-level tables and model outputs reserved for subscribers. The objective here is simple: show the analytical depth and near-term decision levers while directing stakeholders to the full report for the underlying segmentation and scenario datasets.

24 Hour Emergency Roadside Assistance Market

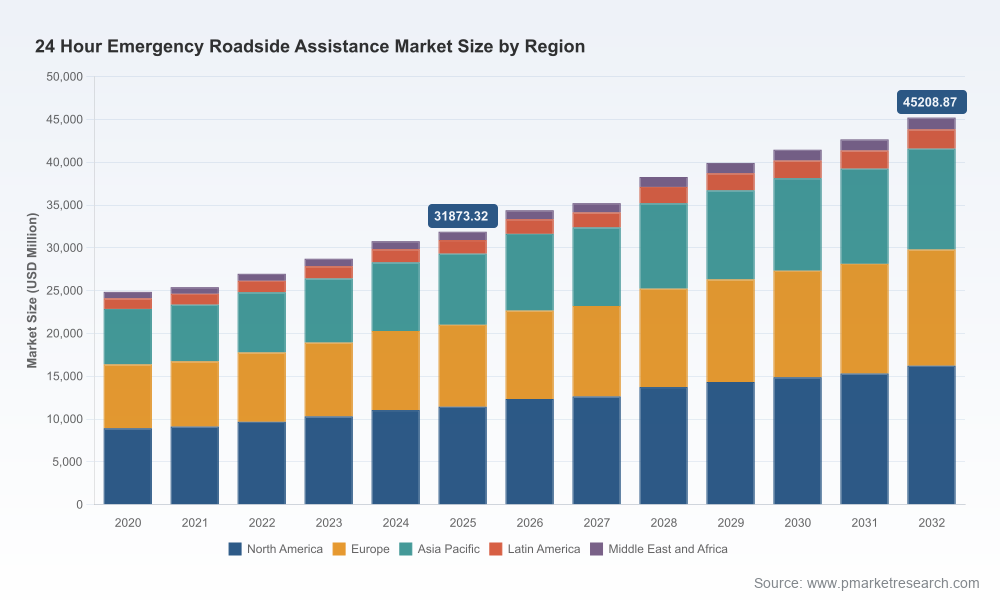

The 24 Hour Emergency Roadside Assistance market has moved from a marginal ancillary service to a core customer-retention and fleet-resilience capability for insurers, OEMs, mobility platforms, and independent service networks. After consistent expansion through 2020–2025, the market stands at a scale that makes it commercially strategic for adjacent industries: insurers use it to reduce claims cost and increase loyalty, OEMs use it to differentiate ownership propositions, and fleet operators treat it as a mission-critical operational KPI.

24 Hour Emergency Roadside Assistance Market

Our top-line model projects continued expansion as the sector transitions from legacy towing and battery-aid services into a hybrid model that blends traditional field operations with digital orchestration, EV-aware interventions, and value-added mobility services. The near-term forecast is underpinned by a mid-single-digit compound annual growth rate (CAGR) across the 2026–2032 projection window, reflecting steady volume growth and increasing per-event monetization tied to premium service bundles and telematics-enabled upsell.

24 Hour Emergency Roadside Assistance Market

The sector remains commercially meaningful for a set of global and regional incumbents that combine scale, brand, and network density with service reliability. Established motor clubs and insurance-affiliated providers retain a durable advantage on membership distribution and trust. At the same time, white-label operators and digital marketplaces are compressing response times and offering tailored fleet solutions.

Recent commercial moves illustrate this dynamic mix: global assistance firms are renewing or extending OEM partnerships to harmonize pan-regional programs; national patrol operators are aligning with new automotive entrants to secure franchise-level service volumes; and fleet services groups are consolidating internal capabilities to present unified fleet service offerings beginning in 2026. These developments validate a two-track competitive thesis—scale and distribution matter, but operational excellence and digital orchestration are accelerating capability differentiation.

Three regulatory and operational trends will define return-on-investment for market participants next year:

For 2026 planning, organizations must incorporate regulatory scenario runs and vintage-specific equipment upgrade plans—particularly for EV extraction, onboard battery management during recovery, and secure storage—to avoid surprise capital outlays later in the forecast horizon.

Leaders planning investments or partnerships in 2026 should align near-term actions to three strategic priorities:

In practice, these priorities translate into three concrete 90–180 day actions for executive teams: (1) complete a network audit against EV-handling requirements and execute a prioritized retrofit plan; (2) pilot a digital-dispatch proof-of-value with a sampling of high-volume accounts; and (3) negotiate at least one OEM or fleet partnership with performance-based pricing to align incentives and reduce unit cost.

Our report is designed as a decision support tool—combining market sizing, scenario models, provider benchmarking, and a tactical implementation playbook. For executives who need to translate strategic direction into operational plans, the report includes vendor scorecards, contract templates, and a regulatory checklist to fast-track compliance actions. For corporate development teams, the study contains a calibrated M&A screen that identifies acquisition targets by capability gaps rather than by geography alone.

To honor the “trailer” principle: this release demonstrates the study’s strategic utility while withholding the proprietary segmentation tables, regional breakdowns, and per-service revenue schedules that underwrite our valuation models. Those outputs are available exclusively in the full report.

We invite senior leaders—CFOs assessing capex, heads of claims and mobility, OEM strategy teams, and private-equity investors—to review the full PW Consulting 24 Hour Emergency Roadside Assistance Market report. The complete publication includes the underlying datasets, interactive scenario models, and confidential annexes that support transaction due diligence and operational transformation programs for 2026 and beyond.

Contact PW Consulting for access to the full report and to schedule a tailored briefing that maps the findings to your organization’s specific business model and risk profile.

For detailed analysis of this topic, please visit the official page:24 Hour Emergency Roadside Assistance Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com