Next-Generation Marine Navigation Solutions Propel Handheld Marine GPS Market Through 2034

Fitness |

2026-06-22 06:00:46

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a high-level, decision-focused briefing drawn from our full Vacuum Atmosphere Furnace Market study. This preview highlights the actionable insights that industrial leaders, investors, and technology partners should prioritize in 2026. It demonstrates the analytical depth of our research while preserving the full, segmented intelligence for readers who access the complete report.

Vacuum Atmosphere Furnace Market

The vacuum atmosphere furnace market has moved from niche, highly specialized applications toward a broader, growth-oriented industrial staple. Our analysis shows the market expanding from the low hundreds of millions (USD Million) in 2020 to roughly USD 612.5 Million in 2025, and, under a base-case scenario, tracking at a compound annual growth rate (CAGR) of approximately 7.85% through the 2026–2032 forecast window. By 2032 the market approaches the billion-dollar mark, signaling both scale and continued technology-driven demand.

Vacuum Atmosphere Furnace Market

Market concentration is moderate: the combined revenue share of the top three and top five suppliers indicates meaningful incumbency advantages but leaves clear room for differentiated entrants. Specifically, the top three account for an estimated portion of market value consistent with mid-market concentration, while the top five broaden the share further—an ideal dynamic for strategic competition centered on technology, service, and supply resilience.

Vacuum Atmosphere Furnace Market

Demand maturation: OEMs and Tier-1 suppliers in aerospace, automotive, and electronics are consolidating heat-treatment specifications and supplier relationships. Buyers increasingly view vacuum processing as a quality and lifecycle-cost play rather than a pure-capex decision.

Technology bifurcation: Energy-efficient designs, high-pressure gas quenching (HPGQ), and modular hot zones are becoming decision criteria that separate premium solutions from legacy offerings.

Regulatory and ESG pressure: Energy use and emissions requirements—especially in Europe—are accelerating investment in low-emissions furnace architectures and monitoring systems.

Supply-chain fragility: Inputs such as high-purity graphite face delivery constraints and pricing volatility that directly affect lead times, cost-of-goods, and strategic inventory planning.

Capital allocation — invest selectively in technology that reduces total cost of ownership. Projects that tangibly cut cycle time, lower energy intensity, or enable HPGQ in a compact footprint offer a faster path to positive ROI than incremental capacity expansion.

Supply resilience — build dual-source strategies for critical materials, consider nearshoring or strategic inventory for graphite and specialty alloys, and negotiate supplier-level service agreements that include priority allocation clauses.

Product & technology roadmaps — prioritize modular designs and digitally enabled controls. Remote diagnostics, predictive maintenance, and data sovereignty features are rapidly moving from value-add to expected supplier capability.

M&A and partnerships — target bolt-on plays that close capability gaps (e.g., gas-quench expertise, atmosphere-control IP), or that offer regional service networks to shorten lead times and strengthen aftermarket revenue streams.

Commercial model evolution — transition from unit sales to performance-based contracts and longer-term service agreements where possible. This captures aftermarket value and aligns incentives to uptime and efficiency.

The competitive set in our study includes global incumbents with distinct value propositions. Understanding their strengths clarifies where new or differentiated players can compete.

Ispen (Ipsen): Known for comprehensive vacuum heat-treating lines with proven series for aerospace and medical markets. Strengths include established brand, broad process portfolios, and aftermarket capabilities—critical when winning long-term OEM contracts.

Solar Manufacturing / Solar Atmospheres: Specialist in energy-efficient and HPGQ-equipped solutions. Recent activity—shipments of large carbide and carburizing systems and facility upgrades—signals a focus on capacity and certification-driven trust (e.g., Nadcap equivalents).

Centorr Vacuum Industries: Differentiates on extreme-temperature capability and bespoke R&D systems. Their engineering-oriented portfolio is attractive to materials research labs and manufacturers pushing high-temperature metallurgy boundaries.

SECO/WARWICK: Offers a broad line of vacuum solutions and benefits from multinational manufacturing and service reach—useful in global supply chains, especially for automotive and heavy industry.

AVS Inc., ECM Technologies, Camco Furnace, ALD-Holcroft: These firms cover niches from custom high-temperature systems to hydrogen-compatible cold-wall furnaces. Their agility and specialized product lines make them preferred partners where standard solutions won’t suffice.

Recent public developments (installations, large shipments, and quality certifications) indicate a market where operational proof-points—demonstrated installations, delivery to aerospace suppliers, and Nadcap or equivalent certifications—drive commercial momentum. We intentionally summarize these trends here; granular transaction and project-level metrics are reserved for the full report.

Raw-material risk: High-purity graphite shortages and export controls have caused price and lead-time shocks. Mitigation: develop supplier scorecards, qualify substitute materials where feasible, and implement forward-buying or consignment programs for critical spares.

Regulatory risk: Energy and emissions standards in key jurisdictions will impose retrofits or replacement of older fleets. Mitigation: prioritize modular retrofits and invest in energy monitoring systems that provide compliance data and enable carbon accounting.

Service and uptime risk: Extended lead times for replacement hot zones or custom parts threaten customer SLAs. Mitigation: scale regional service hubs, offer refurbished hot-zone options, and standardize component families to reduce unique part counts.

Technology obsolescence: As digital controls become baseline, suppliers without a clear IIoT/M2M roadmap risk margin compression. Mitigation: adopt open-architecture controls and partner with analytics providers to accelerate service modernization.

Our full study is structured to support executable decisions in three workstreams: Growth, Resilience, and Differentiation.

Growth playbooks — market-entry and expansion scenarios with prioritized end-markets, buyer personas, and likely procurement timelines.

Product and capability matrices — comparative engineering features, energy profiles, and process fit for primary heat treatments, enabling product managers to align R&D with customer economics.

Supply-chain stress tests — scenario-based analyses that quantify lead-time and cost exposure to graphite and other critical inputs, plus mitigation roadmaps.

Commercial models — pricing and aftermarket service strategies, including servitization templates and contract KPIs to sustain margin while locking in annual recurring revenue.

Regulatory and ESG playbook — compliance impact assessments and retrofit prioritization frameworks to meet regional energy and emissions requirements while optimizing capex sequencing.

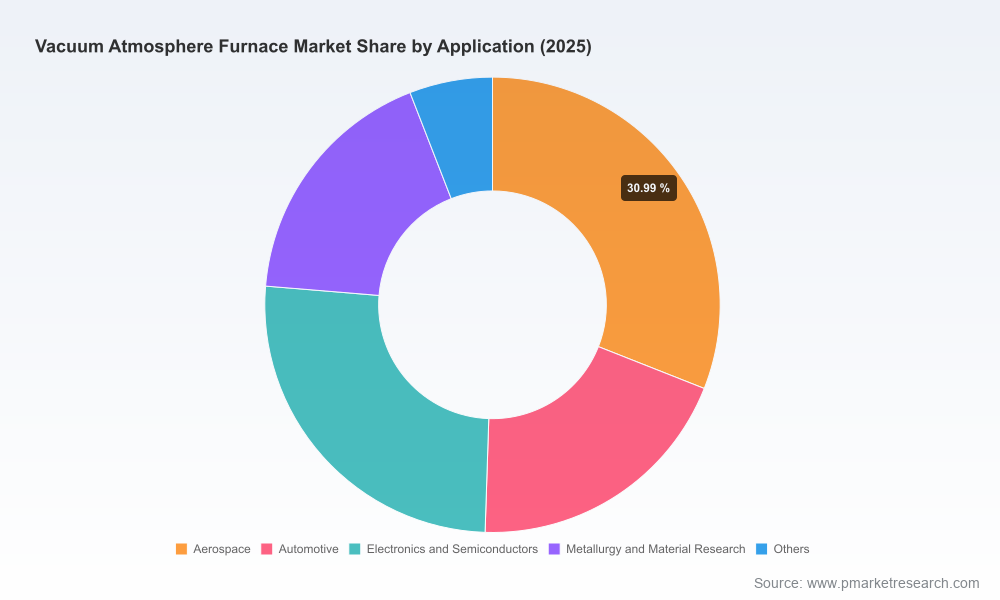

To preserve commercial value and maintain a competitive edge for report subscribers, we publish this executive preview without disclosing detailed regional or application-level shares and the granular tables contained in the full dataset. The comprehensive segment-level tables, vendor-level benchmarking, and scenario spreadsheets are available through the report portal.

CEOs and strategy teams — use the market-size trajectory and moderate concentration metrics to reassess inorganic options and prioritize investments that accelerate service and digital transitions.

Heads of operations — apply the supply-chain stress tests in the report to develop 12–24 month inventory and sourcing plans that reduce production interruptions.

Product leaders — implement the product-capability matrices to accelerate modular designs and to roadmap HPGQ or hydrogen-ready adaptations where customer demand and regulatory context justify.

Commercial teams — adapt pricing and contracting models to capture aftermarket revenue; use evidence-backed win themes (energy efficiency, certification status, lead-time assurance) to negotiate multi-year agreements.

2026 is the year where strategic clarity beats tactical reaction. Our macro findings—solid mid-single-digit-plus CAGR, a market scaling toward billion-dollar status, and a moderately concentrated supplier landscape—point to opportunity for incumbents who modernize and for focused challengers who can combine technology differentiation with robust service propositions.

For executives preparing capital plans, M&A theses, or global service strategies, the full PW Consulting Vacuum Atmosphere Furnace Market report contains the segmented demand maps, supplier scorecards, and scenario worksheets needed to convert insight into action. This preview intentionally avoids publication of detailed regional and application breakdowns so that subscribers retain a commercial advantage.

Access the full report to obtain the proprietary segmentation tables, vendor benchmarking, and actionable templates that will guide your 2026 decisions with precision.

For detailed analysis of this topic, please visit the official page:Vacuum Atmosphere Furnace Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com