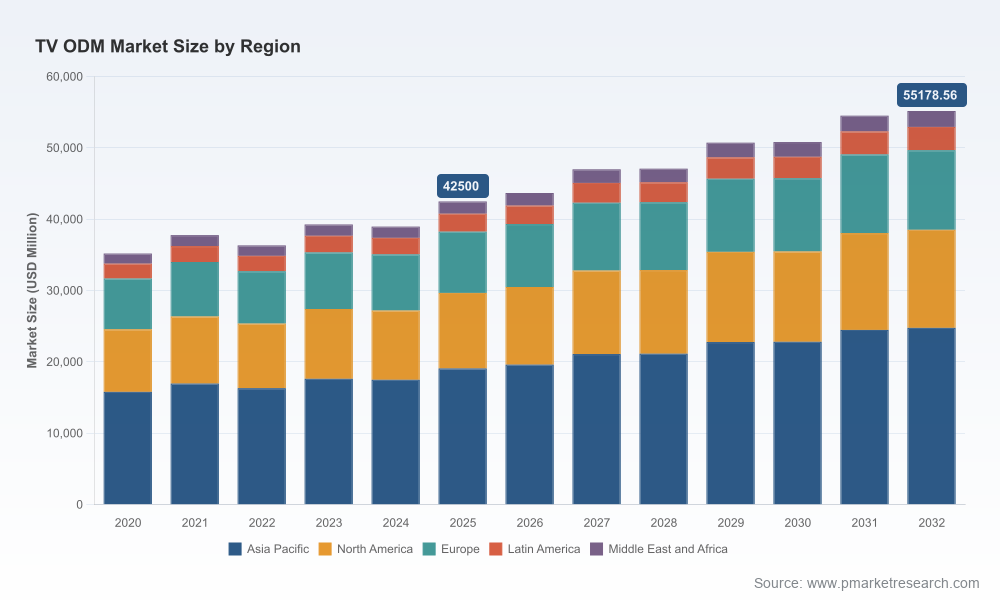

TV ODM Market 2026 Strategic Brief: Navigating a USD 42.5B Industry Toward 2032

As PW Consulting’s lead industry analyst, I am pleased to present a condensed, decision-focused preview of our full TV ODM Market Report (base year 2025). This brief is written for C-suite leaders, corporate strategy teams, procurement chiefs, and investors who need to calibrate 2026 plans against a shifting global supply chain. Our core finding: the TV ODM market sits on a steady growth trajectory — rising from a market size of roughly USD 42.5 billion in 2025 to an expected USD 55.2 billion by 2032 under a 3.8% compound annual growth rate (CAGR) — but the shape of value capture and risk is changing fast.

Tv Odm Market

Why this matters for 2026 decision cycles

- Strategic timing: 2026 is the inflection year for several structural moves — capacity coming online, platform transitions in smart TV software, and renewed pricing pressure from panel supply shocks. Companies that align procurement, product roadmaps, and channel strategies now will disproportionately capture profitable volume through the later part of the decade.

- Margin pressure vs. premiumization: While unit growth is modest, margin differentials are widening between commodity LED sets and higher-value mini-LED/OLED or platform-enabled smart TV products. Cost inflation in key bill-of-materials items (notably display panels and ICs) is creating opportunities for vertical integration, strategic sourcing partnerships, and design-for-cost programs.

- Consolidation and scale: The market remains concentrated among a few large ODMs and display manufacturers. Our concentration metrics indicate meaningful market share aggregation among top suppliers, creating both negotiating leverage and single-point risks for brands and retailers sourcing large volumes.

Macro dynamics shaping the 2026 operating environment

Three cross-cutting forces will determine who wins in the next wave of TV procurement and product launches:

Tv Odm Market

- Input-cost volatility: Display panels continue to represent the single largest manufacturing line item for TVs. Early-2026 panel pricing increases, coupled with rising IC and metal costs, are pressuring conventional price points and forcing OEMs and ODMs to re-evaluate BOM configurations and local buffer strategies.

- Policy and trade risk: Tariff considerations and regional industrial policy debates — including proposals to adjust duties on certain display components — are intensifying supply-chain redesign discussions. For firms selling into protected markets, nearshoring or diversified assembly footprints will move from optional to strategic.

- Platform and software differentiation: Turnkey smart-TV platform partnerships are gaining significance. ODMs that offer robust integration with leading smart-TV OSes extend the value proposition to licensees and channel partners, shortening time-to-market for differentiated consumer experiences.

Competitive landscape — what to watch

The ecosystem of TV ODMs and display suppliers comprises long-established contract manufacturers and ambitious, vertically integrated display firms. Key dynamics we highlight in the full report include capacity additions, strategic client relationships, and technology road maps. Selected observations below summarize the competitive posture of notable players without revealing confidential volume splits.

Tv Odm Market

- MOKA (TCL MOKA): Positioned as a turnkey ODM with deep integration into the TCL ecosystem and a rapidly growing order book. Recent strategic moves include turnkey partnerships for modern smart-TV platforms, enabling licensed brands to accelerate market entry without heavy internal R&D investment.

- AMTC: A major ODM that is prioritizing international channels and capacity expansion in Southeast Asia — a strategic play to serve North American and global demand with flexible sourcing models.

- HKC: A top-tier contractor that continues to scale capacity through large greenfield facilities. Their multi-factory footprint aims to reduce lead times and provide geographic redundancy for major retail and licensed-brand customers.

- Express Luck, TPV Technology, BOE VT, Foxconn, KTC, JPE, Innolux and Mianhong TV: Each occupies a distinct strategic niche — from high-volume commodity supply to premium mini-LED/OLED engineering, and from captive-brand strategies to one-stop global OEM/ODM services. Collectively these players define the competitive fabric, with suppliers differentiating on speed, scale, integration, and access to advanced panel technologies.

Recent corporate developments — indicative signals

- ODM-platform alliances accelerated in early 2026, as evidenced by MOKA’s recent integration with a major smart-TV OS, signaling that software-enabled differentiation is now a procurement consideration as important as hardware specs.

- Large-scale production ramps continued in 2025–2026 with multiple new factories entering operation or expanding capacity, underscoring that the near-term supply picture will be shaped by how quickly demand absorbs fresh volumes.

- Manufacturers are actively marketing flexible ODM propositions to brands seeking to offload complexity; trade show participation and turnkey showcases have become primary channels for securing multi-year supply contracts.

What the full PW Consulting TV ODM Report includes (operational, actionable modules)

Our full report is designed as a working playbook for executives making 2026 decisions. It is structured to move from high-level strategy to actionable implementation levers, and includes:

- Proprietary market model and forecast (2026–2032) built from bottom-up capacity, shipment, and price assumptions — including scenario variants that stress-test outcomes under different panel-cost and tariff environments.

- Supply-chain and unit-economics analysis with sensitivity mapping showing which components drive margin swings and where design or sourcing changes yield the largest profit impact.

- Manufacturing capacity tracker and facility-level intelligence — locations, start-up timelines, and strategic intent — to support sourcing choices and contingency planning.

- Profiles of leading ODMs and panel suppliers with strategic assessments covering technology capability, customer mix, and alliance potential.

- Commercial playbooks for brands and retailers: negotiation templates, payment and inventory financing options, and co-development pathways to accelerate premium product launches.

- Risk register and mitigation playbooks addressing tariffs, raw-material shocks, and demand-side scenarios (e.g., consumer downtick, retail channel flux).

- M&A and partnership decision frameworks to evaluate bolt-on acquisitions, minority investments in upstream suppliers, or long-term offtake agreements to secure volume at defined margins.

Strategic implications and recommended actions for 2026

The following distilled recommendations draw on our forecast and scenario analysis. They are actionable within standard corporate planning cycles and scalable to different balance-sheet sizes.

- Re-price and hedging playbooks: Update BOM-based pricing models to incorporate current panel and IC cost trajectories. Negotiate multi-tiered pricing clauses with suppliers that include explicit pass-throughs, indexation, and breakpoints for volume commitments.

- Prioritize platform partnerships: For brands with limited software capabilities, prioritize ODMs that provide certified integrations with established smart-TV ecosystems to reduce time-to-market and enhance consumer retention.

- Regional sourcing contingency: Construct a two-tier sourcing map — primary partners for scale and secondary partners for geographic redundancy — and model the P&L impact of partial nearshoring under plausible tariff scenarios.

- Invest in BOM engineering: Reallocate a portion of R&D to design-for-cost initiatives (panel size optimization, IC consolidation, firmware feature rationalization) that protect margin without eroding perceived product value.

- Use capacity signals to time product launches: Align major product introductions with expected absorption of new factory output to avoid promotional margin erosion in oversupplied windows.

- Explore financial insurance: For large multi-year contracts, consider working-capital and inventory-financing structures that convert supplier-side volatility into predictable cash flows.

What we are deliberately withholding here (and why you need the full report)

This briefing purposefully omits our granular regional, type, and application-level splits and proprietary tables that quantify channel-by-channel demand and segment-by-segment unit economics. Those details are the operational levers we license to clients because they materially affect sourcing, SKU planning, and contract design. If you are evaluating CAPEX, pricing, or a strategic sourcing decision for 2026, the difference between a good and an optimal decision will depend on the exact segmentation and facility-level numbers contained in the full dataset.

Final note — timing and engagement model

For executives planning FY26 product roadmaps, procurement cycles, or investment committees, the timing is urgent. The combination of capacity coming online, software-platform consolidation, and commodity-cost pressure creates a narrow window where proactive contract design and strategic sourcing can lock in favorable economics.

PW Consulting offers tailored engagements — from a rapid 6-week supplier due-diligence package to an end-to-end commercial transformation and sourcing renegotiation program. For immediate access to the complete market tables, regional forecasts, and the full set of playbooks referenced here, please contact our research distribution team or visit the TV ODM Market page on the PW Consulting portal.

For detailed analysis of this topic, please visit the official page:Tv Odm Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com