How Annual Events Strengthen Brand Identity and Team Spirit

Other |

2026-05-23 06:47:21

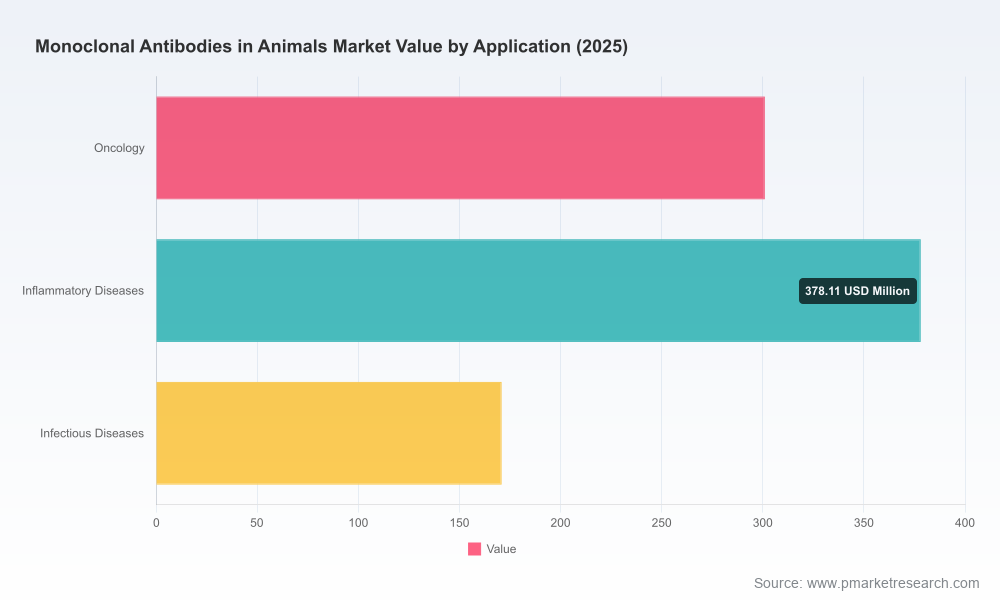

As monoclonal antibody (mAb) therapeutics transition from novel science to commercial veterinary standard-of-care, 2026 represents a pivotal inflection point for investors, animal health CEOs, and R&D leaders. PW Consulting’s forthcoming market study, “Monoclonal Antibodies in Animals Market,” synthesizes longitudinal data (2020–2025) and forward-looking scenario analysis (2026–2032) to equip executive teams with the strategic intelligence needed for decisive action next year. At a macro level, the market reached approximately USD 850 million in 2025 and is projected to exceed USD 970 million in 2026, growing at a compound annual growth rate of 8.2% through our forecast horizon to reach a multi‑hundred‑million‑dollar endpoint by 2032. This preview outlines the report’s strategic value for 2026 decision-making while preserving the granular segment-level intelligence available in the full study.

Monoclonal Antibodies In Animals Market

Timing: 2026 will be marked by regulatory inflection points, accelerated commercialization of companion‑animal mAbs, and early consolidation. Our report decodes the timing and sequencing of these dynamics so leaders can prioritise capital allocation and partnership roadmaps.

Monoclonal Antibodies In Animals Market

Execution: The path from laboratory candidate to veterinary clinic is being reshaped by conditional approval pathways and novel regulatory approaches. PW Consulting maps out operational milestones that materially affect go‑to‑market timelines and cash‑flow models.

Monoclonal Antibodies In Animals Market

Competitive posture: With a concentrated top tier of incumbents and an active mid‑market of biotech licensors, strategic plays for 2026 will prioritize either platform scale or narrow, defensible niches. The report frames those choices against competitive intensity and capability gaps.

Market sizing and trend analytics: validated historical series and multiple forecast scenarios tailored to different adoption and pricing trajectories.

Commercial playbooks: indication prioritisation matrices, veterinarian adoption curves, pricing and reimbursement strategies, channel and distribution blueprints for companion animals and livestock use cases.

Regulatory pathway compendium: decision trees covering FDA, USDA conditional approvals, EMA/Regulation (EU) 2019/6, and VICH guidance—aligned to candidate types and likely approval timelines.

Manufacturing and supply strategy: COGS levers, options for in‑house vs CMO scale-up, fill–finish constraints, and capital phasing to de‑risk launch supply at clinical scale.

Pipeline and partnership maps: validated asset-level profiles, licencing playbooks, and target lists for bolt‑on acquisitions or strategic alliances.

Financial models and scenario planning: interactive models stress‑tested for pricing pressure, reimbursement roll‑out, and accelerated or delayed approval paths.

Risk & mitigation matrix: operational, regulatory, commercial and reputational risks with prioritized mitigations and trigger points for corrective action.

Regulatory evolution: Recent regulatory activity is transforming development pathways. Notable changes include USDA conditional approvals as a practical route for immune‑mediated indications and an FDA‑announced plan to reduce animal testing in mAb development through new approach methodologies. These shifts shorten some time‑to‑market windows but require more sophisticated non‑clinical dossiers and stakeholder engagement strategies.

Cost and reimbursement constraints: High production and quality assurance costs remain a primary adoption barrier in veterinary settings. Payers (including pet insurers and large owners of livestock) will increasingly influence pricing ceilings and uptake cadence.

Therapeutic innovation and differentiation: The pipeline includes both species‑specific biologics and platform technologies (e.g., orally administered antibodies for livestock passive immunity). Differentiation strategies are moving beyond molecule potency to delivery format, duration of effect, and ease of administration in ambulatory settings.

Consolidation pressure: Market concentration metrics indicate a market dominated by a small number of incumbent players, which raises the bar for commercialization infrastructure but creates opportunities for specialist entrants through licensing and targeted M&A.

The market is characterized by a mix of large animal health corporations and specialised biotech licensors. Leading incumbent firms have translated R&D investments into commercially available mAbs for key companion animal indications, and their continued product expansion and regulatory wins will set competitive benchmarks for safety, efficacy, and commercial reach.

Scale players: Established animal health companies with commercial and distribution scale have first‑mover advantages in clinic access and brand trust. Recent regulatory approvals and launches continue to strengthen their position.

Technology licensors and innovators: Specialist companies with proprietary antibody platforms or novel delivery formats are attractive partners or acquisition targets for scale players seeking to broaden pipelines.

Collaborative models: Licensing agreements and acquisitions have accelerated—demonstrating a pragmatic route to expand therapeutic breadth without replicating upstream discovery investment.

Interpretation: Concentration measures show top players holding a significant share of current revenue, implying that new entrants must either partner with incumbents or focus on high‑value niches where platform differentiation reduces head‑to‑head exposure.

Short term (next 12 months): 1) Reassess pipeline prioritisation against regulatory fast lanes (e.g., conditional approvals); 2) Secure flexible manufacturing capacity to support pilot launches; 3) Initiate payer engagement pilots with large veterinary networks and pet insurers to validate acceptable price points.

Medium term (12–36 months): 1) Pursue licensing deals for late‑stage assets that reduce technical risk; 2) Invest in delivery innovation to lower administration barriers in ambulatory veterinary care; 3) Build cross‑functional commercialization playbooks (veterinarian education, sample access programs, and bundled care propositions).

Long term (36+ months): 1) Consider platform consolidation acquisitions to secure IP and reduce per‑unit production costs; 2) Scale global market access with attention to regional regulatory divergence and local manufacturing incentives; 3) Institutionalize a continuous evidence‑generation strategy to transition conditional approvals to full licensure.

Regulatory risk: Changes in non‑clinical requirements or approval standards can delay launches — mitigate by early regulatory dialogue and multi‑jurisdiction submission strategies.

Manufacturing and supply risk: Single‑source CMOs or fill–finish bottlenecks can jeopardize launches — mitigate via dual sourcing and capacity reservation models.

Commercial adoption risk: Veterinarian prescribing behavior and payer constraints can slow uptake — mitigate with targeted veterinarian education, real‑world evidence programs, and innovative pricing pilots.

Competitive and IP risk: Rapid licensing and new entrants can erode value — mitigate by securing defensive IP, exclusivity agreements, and rapid lifecycle management plans.

Beyond headline market trajectories, the report combines proprietary primary interviews with veterinarians, payers, and industry R&D leaders; a validated transactional database of licensing and M&A activity; and interactive financial models that stress‑test commercialization outcomes under alternative regulatory and pricing regimes. For boardrooms and investment committees focused on 2026, the study supplies both the narrative and the executable checklists needed to move from strategy to implementation.

Use the report to set decision gates for 2026 capital deployment: align R&D milestones, manufacturing commitments, and commercial launch timelines with conditional approval opportunities.

Prioritise partnership scouting against the report’s pipeline and licencing maps to accelerate market entry while limiting standalone R&D exposure.

Adopt a “regulatory‑first” development mindset: shape dossiers for non‑animal methodologies where possible, and build evidence packages that facilitate conditional approvals and rapid clinician acceptance.

PW Consulting’s “Monoclonal Antibodies in Animals Market” report is designed as an operational tool for 2026. It offers the strategic frames, implementation roadmaps, and risk‑calibrated financial scenarios necessary to move with confidence in a rapidly maturing market. For the complete dataset, detailed segmentation, downloadable models, and bespoke advisory engagements that translate these insights into a company‑specific plan, please refer to the full report page.

For detailed analysis of this topic, please visit the official page:Monoclonal Antibodies In Animals Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com