Liquid Phenolic Resin Market: Strategic Outlook for 2026 — PW Consulting

Executive preview

PW Consulting’s latest market study on Liquid Phenolic Resin delivers an executive-grade synthesis of market dynamics, competitive positioning, and practical decision frameworks tailored for boards, corporate strategy teams, and commodity procurement leaders preparing for 2026. The market has demonstrated steady expansion through the mid‑2020s — growing from roughly USD 5.9 billion in 2020 to approximately USD 7.4 billion in 2025 — and our baseline forecast anticipates continued expansion to about USD 10.4 billion by 2032 at a compound annual growth rate (CAGR) of 5.01% over the forecast period. This release explains why those topline trends matter for near-term capital allocation, product strategy, and supply‑chain design while preserving the granular, segment-level datasets exclusively for report subscribers.

Liquid Phenolic Resin Market

Why this matters for 2026 corporate decisions

Liquid phenolic resins remain a strategically important polymer family across adhesives, insulation, foundry binders, laminates, and specialty friction and abrasive applications. Three market forces will dominate corporate decision-making in 2026:

Liquid Phenolic Resin Market

- Input cost volatility: phenol feedstock pricing spiked in early 2026 (Northeast Asia spot benchmarks reached approximately USD 1.01/kg in March 2026), creating immediate margin pressure and forcing producers to reassess hedging and pass-through mechanisms.

- Regulatory and sustainability pressure: tightening formaldehyde emission standards and the wider implications of chemical controls (including EU measures affecting related chemistries) are increasing compliance complexity and marginal production costs.

- Strategic concentration and growth pockets: the market structure shows moderate concentration (the three largest firms account for a material but not dominant share), leaving room for focused M&A, regional capacity rebalancing, and differentiation through low-emission or certified product lines.

What PW Consulting’s report delivers (practical highlights)

The report was designed as an operational toolkit rather than an academic exercise. Key deliverables include:

Liquid Phenolic Resin Market

- Robust market sizing and a harmonized forecast to 2032, supporting scenario planning under alternative feedstock and regulatory trajectories.

- Price‑sensitivity and margin modeling with live-case scenarios that quantify the impact of phenol price swings, formaldehyde compliance costs, and tariff interventions on producer economics.

- Supply‑chain risk mapping that aligns asset footprints with logistics and trade-policy shocks, and diagnostic guidance to reduce single-source exposure.

- Competitive benchmarking and capability heat maps for technology, production scale, and sustainability credentials, focused on enabling quick “fit/gap” assessments for partnerships or M&A targets.

- Practical implementation modules: contract clauses for cost pass-through, an R&D roadmap for low‑emission resoles, procurement hedging playbooks, and a checklist for product certification and labelling pathways.

Competitive landscape and strategic implications

The industry combines global chemical majors with specialized regional producers and custom toll-manufacturers. Leading companies profiled in the report include Hexion Inc., Prefere Resins, Sumitomo Bakelite, BASF SE, DIC Corporation, Capital Resin Corporation, Georgia‑Pacific Chemicals, Bakelite Synthetics, Jinan Shengquan Group, and SI Group. Our comparative analysis emphasizes three strategic archetypes:

- Scale integrators (global majors): firms with upstream integration and broad distribution networks, able to absorb feedstock volatility and allocate capacity across regions. These players excel at large industrial accounts and volume contracts but face slower product-agility on emerging low‑emission formulations.

- Regional specialists: Europe- and Asia-focused producers that combine product specialization with regulatory knowledge, enabling faster certification and penetration in application segments where low-emission or certified resins carry a premium.

- Niche/toll manufacturers and formulators: smaller players offering custom liquid phenolic and resorcinol resins, lean on ISO and specialty certifications to serve adhesives, composites, and technical markets where service and customization trump scale.

From a 2026 strategic standpoint, companies should evaluate whether to pursue scale-driven cost leadership, localized differentiation via sustainability certification, or a hybrid approach that pairs global procurement with regional product innovation. The market concentration metrics underscore opportunity: the top-tier players command meaningful shares, yet the overall structure leaves room for bolt-on acquisitions and targeted capacity investments by mid‑sized firms.

Macro and regulatory tailwinds — practical takeaways

Key contextual developments that shaped our modeling and that require executive attention:

- Feedstock trends: Phenol price behavior has been the principal near-term earnings driver. The March 2026 Northeast Asia spot level near USD 1.01/kg (up materially since late 2025) demonstrates how quickly margins can compress. Procurement teams should integrate shorter‑term hedging and longer-term supplier diversification into 2026 budgets.

- Formaldehyde and emissions regulation: Stricter standards are increasing compliance costs for producers, estimated in our analysis to raise per-unit compliance spending by mid-single- to low-teens percentages depending on facility vintage and control technology. R&D and capex planning must prioritize low‑emission formulations and control retrofits.

- Substitution and chemical restrictions: Regulatory moves (example: BPA restrictions and evolving ECHA guidance) have knock-on effects for certain phenolic resin end-uses. Commercial teams must maintain cross-functional product impact assessments to preserve access to sensitive markets.

- Trade policy: Recent tariff actions have introduced material uncertainty into regional sourcing strategies. For companies with Asian supply exposed to reciprocal tariffs, nearshoring or qualifying alternative suppliers should be evaluated as part of a 12‑ to 18‑month mitigation plan.

Actionable recommendations for 2026

We translate the analysis into practical, prioritized moves that boards and senior managers can operationalize in 2026:

- Recalibrate procurement strategy: implement a two‑axis approach combining short‑term financial hedges for phenol with strategic supplier diversification and capacity options in tariff-resilient jurisdictions.

- Accelerate low‑emission product development: prioritize formulations that reduce formaldehyde emissions and secure certifications (e.g., ISCC PLUS where relevant). Early movers capture pricing premiums as regulators and architects favor compliant materials.

- Optimize manufacturing footprint: run a location-cost-ease assessment that incorporates projected compliance capex, logistics disruption risk, and feedstock access — then sequence retrofit and brownfield expansions rather than greenfield projects in volatile markets.

- Pursue surgical M&A: focus on targets that complement core competencies—either by strengthening specialty offerings (e.g., coatings or adhesives with proprietary low‑emission technology) or by providing regional gateway capacity into growth markets.

- Embed regulatory scenario planning into capital decisions: require a regulatory-sensitivity stress test for all 2026 capex approvals, with trigger thresholds tied to realistic emission cost trajectories.

How executives should use this report

Subscribe and lean on the report in three concrete ways:

- Board-level portfolio reviews: use our delivered scenarios to stress-test EBITDA sensitivity to feedstock and compliance shifts, and to set strategic KPIs tied to emissions and certification milestones.

- Commercial and product strategy: use our benchmarking to reprice contracts, prioritize segments with durable demand, and define go‑to‑market plans for low‑emission grades.

- Procurement and operations: adopt the hedging templates and supplier-risk heat maps to reduce short-term margin volatility while protecting long-term feedstock access.

What we intentionally withhold here — and why

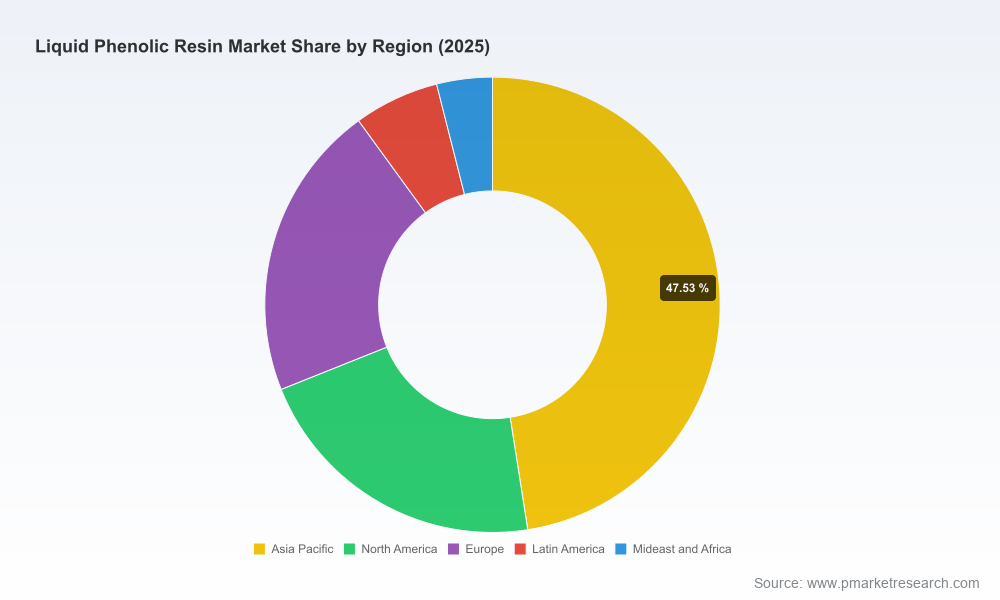

In keeping with a “trailer” approach to this press release, we present the strategic implications and macro drivers while reserving the granular, segment-level tables (regional breakdowns, application and type splits by value, and company-level revenue estimates) for the full report and interactive web‑dashboard. That detailed intelligence is essential for transaction diligence, plant-level investment sizing, and precise pricing strategies — and is available through PW Consulting’s subscription access.

Closing perspective

Liquid phenolic resins will remain a stable-growth industrial polymer through the next decade, but the path to superior returns in 2026 requires a fusion of commodity risk management, regulatory-informed product innovation, and selective strategic investments. Companies that treat the next 12 months as an opportunity to institutionalize feedstock risk controls, secure low‑emission credentials, and realign capacity towards tariff-resilient markets will materially outpace peers when input price volatility and regulatory costs normalize. PW Consulting’s Liquid Phenolic Resin Market report supplies the quantitative backbone and the execution playbooks needed to act decisively.

Next steps

For full access to the report’s datasets, scenario models, company scorecards, and implementation toolkits, visit PW Consulting’s market intelligence portal. Our team is available to present a tailored briefing and to run company-specific scenario analyses to support 2026 budgeting and strategic planning cycles.

For detailed analysis of this topic, please visit the official page:Liquid Phenolic Resin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com