Global Oilseed Processing Market: Industry Analysis, Trends and Future Outlook to 2034

Food |

2026-05-21 09:41:12

PW Consulting today publishes an executive preview of its Consumer IoT Market research, designed to equip executives, investors, and product leaders with the strategic framing they need as they set priorities for 2026. Built on a thorough historical analysis (2020–2025) and forward-looking forecasts (2026–2032), the study quantifies a market that reached approximately USD 208.5 Billion in 2025 and is poised to expand at a compound annual growth rate of 14.85% through the 2026–2032 forecast window. By 2032, the market is projected to more than double from 2025 levels, underscoring both accelerating consumer adoption and rapid technology-driven value creation.

Consumer Iot Market

Timing: 2026 will be a turning point. Technology maturation (edge processing, richer interoperability standards), regulatory inflection (security and consumer protection laws), and evolving consumer expectations (privacy, seamless experiences) converge in ways that will materially affect product road maps, channel economics, and M&A activity.

Consumer Iot Market

Scale and growth profile: With double‑digit CAGR through 2032, the addressable opportunity is large—but not uniformly accessible. Companies that move from isolated product bets to ecosystem plays, subscription monetization, and platform partnerships capture outsized returns.

Consumer Iot Market

Risk-reward balance: Security regulation, standards adoption, and cost pressures create both barriers and differentiation levers. Firms that industrialize secure-by-design processes and interoperability testing will convert regulation from a compliance cost into a market advantage.

This study is designed as a working tool for market-facing teams. Key deliverables include:

Market model & scenario engine — a configurable financial model (USD, Billion unit basis) that maps device line-ups, ASP trajectories, and recurring revenue levers across three demand scenarios to 2032.

Technology and cost playbooks — bill-of-materials level breakdowns (chipset, connectivity module, sensor, enclosure), supplier risk heatmaps, and benchmarked chipset cost ranges for next‑gen connectivity options.

Interoperability and standards checklist — an operational roadmap for Matter, Thread, Wi‑Fi 6E/7 adoption, including integration priorities and certification sequencing for time‑to-market optimization.

Regulatory compliance templates — a compliance roadmap for EU and North American frameworks, pragmatic controls for secure development lifecycles, and audit-ready documentation templates to accelerate market access.

Go‑to‑market playbooks — channel-specific pricing frameworks, carrier and retailer negotiation frameworks, subscription packaging strategies, and field trial kits to accelerate adoption with retailers and service partners.

M&A and partnership scorecards — an actionable shortlist of capability gaps, target archetypes, and valuation sensitivity templates tailored to platform, device, and services acquisitions.

The consumer IoT market exhibits a mix of platform-centric incumbents, device specialists, and aggressive low-cost entrants. The competitive dynamic tilts toward ecosystem builders who can combine hardware with services and recurring software monetization. Our analysis of leading companies yields the following strategic implications for 2026:

Amazon.com, Inc. (Seattle, WA) — Amazon continues to leverage Alexa and device integrations to protect and expand its smart-home gateway role. Recent wearable and display-enabled Echo launches emphasize Amazon’s strategy of owning the voice-and-screen interaction layer. Recommendation: pursue deeper carrier/device bundling pilots and increase focus on premium subscription tiers that lock users into multi-device households.

Google LLC (Mountain View, CA) — Google’s steady Matter adoption in Nest devices pushes interoperability forward and reduces friction for multi-vendor consumer experiences. Recommendation: device makers should prioritize Matter certification roadmaps while negotiating data‑use arrangements that preserve long‑term product differentiation.

Apple Inc. (Cupertino, CA) — Apple’s platform advantages remain in premium user experience and tight hardware‑software integration. HomeKit expansion to third‑party Thread devices signals a more open posture that still preserves premium control. Recommendation: premium device vendors should evaluate joint‑branding and deep integration partnerships with Apple to capture high-margin segments.

Samsung Electronics Co., Ltd. (Suwon, South Korea) — Samsung’s SmartThings platform and recent Wi‑Fi 7 hub certifications position the company for next‑gen home connectivity. Recommendation: ecosystem participants should test SmartThings integrations early to access Samsung’s broad appliance and device channels.

Philips (Signify N.V.) — As a lighting platform leader, Philips remains a durable partner for mainstream smart home integrations. Recommendation: lighting and environmental-sensing vendors should prioritize certified integrations with leading voice and hub platforms to preserve shelf presence.

Sonos, iRobot, Arlo, Wyze, TP‑Link — These firms represent differentiated strategies from premium audio to robotics, security, low-cost disruption, and networking. Recommendation: incumbents should explicitly map each competitor’s threat vector (ecosystem lock-in, price erosion, channel control) and create defensive and offensive options accordingly.

Product and platform evolution — From Amazon’s new wearable Echo frames to Apple’s broader HomeKit integrations and Google’s Matter 1.3 support, vendors are racing to improve user experience and reduce friction across multi‑vendor setups.

Connectivity and performance — Samsung’s Wi‑Fi 7 hub certification and wider Wi‑Fi 6E adoption change the performance baseline for in‑home applications, enabling richer local AI and lower latency experiences. Device makers should model incremental BOM and certification costs against improved engagement metrics.

Robotics and AI — New robotic SKU launches with advanced obstacle avoidance signal renewed consumer interest in higher‑value home automation devices; this alters installed base dynamics and aftermarket service potential.

Regulatory and standards developments are among the highest-impact external forces for 2026 planning:

Security regulation is moving from guidance to enforceable requirements. The EU Cyber Resilience Act introduces mandatory security requirements for devices sold in Europe with phased compliance starting ahead of 2027. North American federal procurement rules and state laws (such as unique default password requirements) add parallel compliance buckets. These create an operational imperative for secure development, signed supply contracts, and post‑sales patching capabilities.

Standards adoption accelerates interoperability. The Connectivity Standards Alliance’s broad uptake of Matter reduces integration friction but increases competition on services and user experience rather than basic connectivity.

Hardware cost dynamics remain a gating factor. Our benchmarking and third‑party sources indicate next‑gen chipsets (e.g., Wi‑Fi 6E) are materially more expensive in high‑volume production than legacy modules, creating short‑term margin pressure but enabling new product value propositions.

Prioritize secure-by-design and OTA assurance: Build an audit-ready SBOM, automated testing, and update pipeline now. Compliance timelines mean retrofitting security is far costlier than building it into product development.

Adopt standards early, differentiate at UX: Certify for Matter/Thread, but use proprietary value layers (privacy-preserving personalization, integrated services) to sustain margins.

Rework commercial models to capture recurring revenue: Pair device sales with subscription services or consumables and quantify LTV uplift in your 2026 planning cycle.

Optimize supply-cost structures: Re-assess BOM sourcing and negotiate tiered commitments for high‑cost connectivity modules; model tradeoffs between marginal BOM increases and reduced churn from better performance.

Prepare M&A and partnership pipelines: Map capability gaps—platform integration, AI-inference at the edge, OTA security—and set contingency valuations for bolt-on acquisitions in 2026.

The market is neither atomized nor tightly consolidated. Top platform companies retain meaningful influence through ecosystems and channel control, but a wide field of specialized device manufacturers, low-cost entrants, and regional players keeps competitive pressure high. For decision-makers this means: defend platform reflexes, but invest selectively in product features and services that are hard to replicate through simple bundling or price competition.

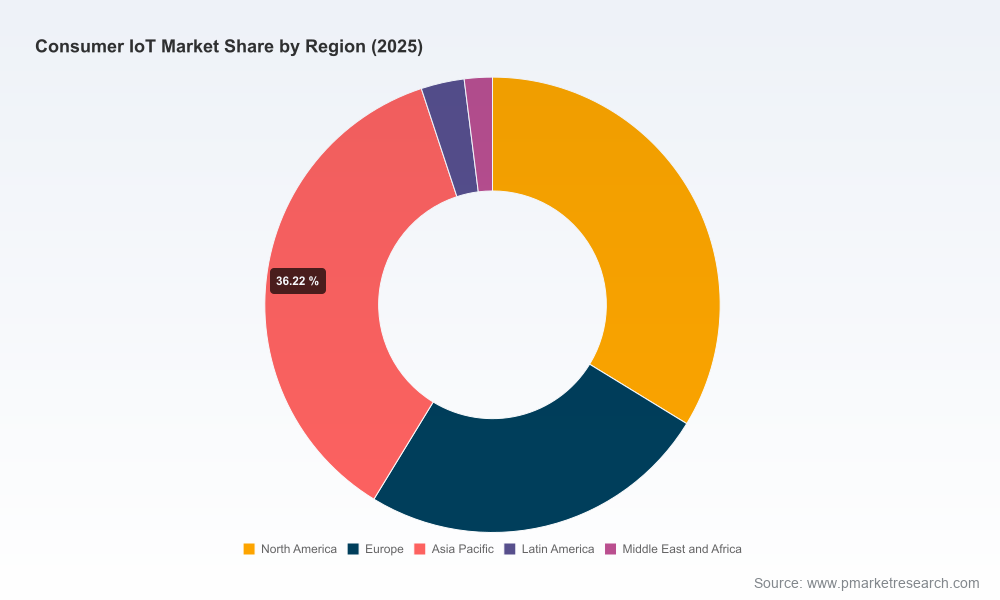

This preview highlights the core strategic choices firms must address in 2026. PW Consulting’s full report provides the proprietary model, detailed scenario outputs, company scorecards, certification readiness matrices, and downloadable tools referenced above. Critical items—explicit regional and application splits, granular capex and revenue forecasts by subsegment, and company market‑share tables—are intentionally reserved for the comprehensive report to ensure clients receive the level of detail required for investment-grade decision making.

To obtain the full Consumer IoT Market report, schedule a briefing, or request custom modeling and advisory support for your 2026 planning cycle, please visit the PW Consulting website or contact your PW Consulting account lead.

PW Consulting advises global technology, consumer goods, and private equity clients on strategy, commercial due diligence, and product-to-market execution. Our Consumer IoT Market practice combines market modeling, device-level engineering insight, and regulatory foresight to deliver actionable strategies that drive growth in a rapidly evolving landscape.

For detailed analysis of this topic, please visit the official page:Consumer Iot Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com