PW Consulting: Strategic Brief — Glycerophosphoric Acid Calcium Salt Market Outlook (2026–2032)

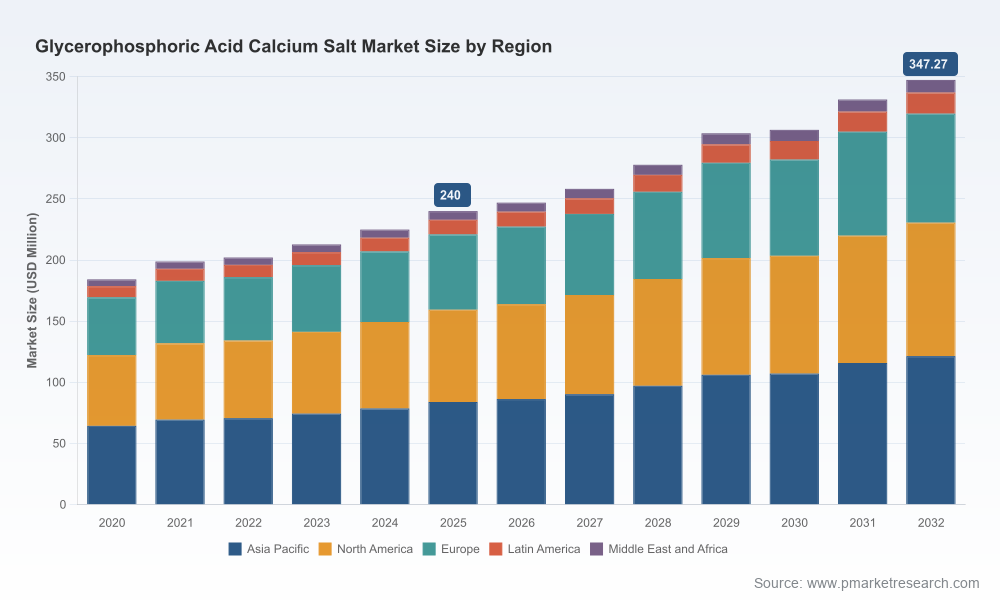

PW Consulting today publishes an executive market brief tied to our full market research report on the Glycerophosphoric Acid Calcium Salt market (commonly marketed as calcium glycerophosphate). Intended as a strategic “trailer” for decision-makers, this release synthesizes the macro trends, competitive dynamics, regulatory context, and executable recommendations that will matter for capital allocation and commercial strategy in 2026. Core subsegment tables and region-by-application revenue breakdowns are intentionally omitted from this briefing; access to the full report provides the complete data set and granular forecasts.

Glycerophosphoric Acid Calcium Salt Market

Market snapshot: growth trajectory and what it means for 2026 planning

- Market scope and tempo: The global market for calcium glycerophosphate has expanded steadily since 2020 and reached an estimated benchmark in our base year 2025. PW Consulting forecasts continued expansion throughout the 2026–2032 horizon at a compound annual growth rate (CAGR) of 5.42% — a pace that supports medium-term capacity investments and product-line diversification without implying hypergrowth risk.

- Implication for 2026 decisions: A mid-single-digit CAGR signals a market that is large enough to sustain new entrants and incremental capacity, yet mature enough that competitive advantage will be won through differentiated capabilities (regulatory approvals, supply reliability, formulation expertise) rather than through volume alone.

- Market concentration: The market exhibits moderate concentration among leading suppliers (three‑player and five‑player concentration metrics indicate a meaningful incumbent presence while leaving space for regional specialists and niche innovators). This dynamic creates opportunities for both selective M&A and focused organic growth strategies.

What this PW Consulting report delivers (practical, transaction-ready content)

Our full report is designed for commercial leaders, corporate development teams, and procurement executives who need both the facts and the playbook. Key deliverables include:

Glycerophosphoric Acid Calcium Salt Market

- Top-down and bottom-up market sizing and a validated forecast model across 2026–2032, enabling scenario analysis for CAPEX and revenue planning.

- Regulatory intelligence and a compliance tracker (GRAS status, relevant pharmacopeia, and cosmetic/ANSM listing implications) that supports product positioning in food, dietary supplements, oral care, and pharmaceutical channels.

- Competitive benchmarking: capability matrices for manufacturers (regulatory certifications, product forms, typical pack sizes, and service-level performance) and a supply-risk heatmap tailored to raw-material sourcing pathways.

- Segment-level opportunity assessments and go-to-market playbooks (including margin sensitivity, price elasticity signals, and distribution channel prioritization) designed for 12–36 month execution cycles.

- M&A/partnership playbook: target screening criteria, synergy modeling templates, and an integration checklist focused on regulatory transfer, quality systems alignment, and customer retention.

- Commercial due diligence appendices: customer interview summaries, sample procurement contracts, and logistics cost models for bulk liquid vs. powder supply chains.

Competitive landscape — strategic interpretation (what leaders and challengers are doing)

The supplier base is geographically and technically diverse. Leading firms combine pharmacopeial compliance and scale, while regional specialists compete on price, customer intimacy, and formulation know-how. Strategic points observed across market participants include:

Glycerophosphoric Acid Calcium Salt Market

- Certification-led differentiation: Manufacturers with pharmacopeial compliance (EP, USP, NF) and recognized GMP/USDMF listings have preferential access to infant nutrition, pharmaceutical, and high-margin oral-care customers where supplier qualification cycles are long and switching costs are high.

- Formulation flexibility as a commercial lever: Firms offering liquid (approx. 50% solutions) alongside dry grades capture both CMO/ingredient routes and direct-to-brand applications. Liquid-form supply capability is a tactical advantage for customers seeking simplified in-line dosing in oral care and functional beverage processes.

- Regional sourcing strategies: Several established players, particularly from India and the U.S., dominate export flows and are scaling to serve growing demand in APAC and North America. European suppliers emphasize pharma-grade credentials and cosmetic listings as a means to protect higher-margin positions.

- Selected players are increasingly publicizing special-use listings (e.g., antimicrobial/anti-plaque cosmetic claims), which can unlock adjacent demand but require robust claims substantiation and quality governance.

Representative company capabilities reflected in our benchmarking (not exhaustive): Global Calcium Pvt Ltd and several Indian manufacturers deliver broad export scale and multi-grade offerings; European firms emphasize pharma-grade and cosmetic certification; U.S. suppliers position on strict cGMP manufacturing and local supply advantages. Readers seeking a full company-by-company capability matrix should consult the full report.

Regulatory and technical dynamics that will shape 2026 market moves

- Regulatory clarity supports adoption: Calcium glycerophosphate continues to be recognized for specific food and supplement uses under established frameworks. Recent regulatory confirmations reinforce its acceptability as a nutrient supplement when manufactured under current good manufacturing practices.

- Cosmetic and pharmaceutical pathways require distinct evidence: Cosmetic listings that position calcium glycerophosphate as an anti-plaque/anti-caries adjunct expand addressable applications, but they demand targeted clinical or in-use substantiation and regulatory filings in each jurisdiction.

- Raw-material and process dependencies: Production involves neutralization chemistry; feedstock quality (glycerophosphoric acid and calcium sources) and process controls directly impact impurity profiles and shelf stability. These technical constraints mean that quality control and supplier qualification are non-trivial and often create long qualification lead times.

- Supply resilience considerations: Liquid vs. powder logistics impose different warehousing and transit risk profiles — a strategic decision between CAPEX-light distribution and CAPEX-intensive localized formulation hubs.

Strategic priorities for 2026 — ten actionable recommendations

- Prioritize supplier qualification early. For products targeting infant nutrition or pharmaceuticals, allocate extended lead time and audit budgets for supplier audits and pharmacopeial dossier transfers.

- Secure flexible supply forms. Maintain access to both liquid and dry grades to serve broad customer requirements and to reduce dependency on a single logistics model.

- Use regulatory status as a barrier to entry. Invest in certifications (pharmacopeial listings, GMP) where premium channels are strategic to avoid competing on price alone.

- Pursue selective M&A or JV to close capability gaps (e.g., a local GxP-compliant manufacturing node) rather than broad horizontal rollups in 2026 when the market is predictable but not overheated.

- Differentiate with formulation science. Funding targeted R&D to improve bioavailability, taste masking, or stability in aqueous systems will be rewarded by oral care and beverage customers.

- Design pricing strategies around delivery economics. Account for freight, cold-chain/non‑cold chain handling for liquids, and inventory carrying costs to protect margins.

- Monitor claim substantiation pathways. Where cosmetic or functional claims are used commercially, lock-in clinical partners early and map out regulatory submission timelines.

- Build contingency for feedstock variability. Assess dual-sourcing for glycerophosphoric acid precursors and evaluate backward integration only when economics support multi-year returns.

- Deploy a customer-segmentation playbook. Target channels with longer contract tenors and higher switching costs (pharma, infant nutrition, national oral-care brands) for priority account management.

- Operationalize sustainability improvements selectively. Small reductions in process emissions or improved solvent recovery can be marketed effectively to large food and personal-care customers without large CAPEX.

Strategic M&A and partnership signals to watch in 2026

Given moderate market concentration and the differentiated value of certifications and formulation know-how, we anticipate acquisition activity that is:

- Targeted (add-on assets to secure regional supply or specific regulatory approvals).

- Valuation-sensitive (buyers will price for near-term synergies in logistics and customer contracts rather than speculative top-line growth).

- Execution-focused (technical transfer and quality system harmonization are common sources of post‑close value leakage; prioritize integration roadmaps that lock in customer contracts and quality continuity).

How PW Consulting can accelerate your 2026 playbook

Our full report, model files, and advisory services translate the above insights into executable programs — from supplier selection matrices and procurement RFP templates to M&A diligence playbooks and regulatory submission planners. We combine primary interviews with leading suppliers, a validated bottom-up supply model, and an outcomes-oriented forecast to guide both commercial and capital decisions.

Note: This briefing intentionally omits the detailed regional and application revenue splits, grade-level forecasts, and company-level revenue streams. Those granular tables, along with scenario-ready financial models and customer willingness-to-pay data, are available exclusively in PW Consulting’s full report and subscriber portal.

Next steps

- Immediate: Download the full report for the complete dataset, including interactive forecast models and the supplier capability matrix.

- For advisory engagement: Contact PW Consulting to arrange a tailored 2‑hour strategy workshop focused on supplier qualification, commercial prioritization, or M&A target screening for calcium glycerophosphate.

PW Consulting’s analysis equips boards, commercial leaders, and procurement executives to convert a reliable mid-single-digit market growth profile into differentiated commercial advantage in 2026. For the complete intelligence package and tactical execution tools, access the full report on our website or reach out to our industry advisory team.

For detailed analysis of this topic, please visit the official page:Glycerophosphoric Acid Calcium Salt Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com