2,5-Dimethyl-2,4-Hexadiene: Strategic Imperatives for 2026 — PW Consulting’s Market Outlook and Executive Playbook

Executive snapshot

As global chemical value chains reconfigure in response to shifting feedstock availability, regulatory scrutiny, and demand reframing toward higher-margin specialty applications, 2,5-dimethyl-2,4-hexadiene (henceforth “2,5-DMHD”) is emerging as a strategically relevant intermediate for manufacturers, distributors, and downstream formulators. Our new market study—anchored on 2025 as the base year and projecting through 2032—documents a steady expansion. After a recovery phase through 2020–2025, the overall market is poised to grow at a compound annual growth rate (CAGR) of 4.51% in the 2026–2032 forecast window, moving from mid‑tens of millions of USD in total revenue in the early 2020s to a market exceeding USD fifty million by 2030 and approaching the high‑fifties by 2032.

2,5-Dimethyl-2,4-Hexadiene Market

Why this report matters for 2026 decision cycles

- Timing. 2026 is a pivot year for procurement cycles, CAPEX approval processes and strategic sourcing initiatives across chemical companies. The market trajectory and scenario analyses in this study provide the timely inputs procurement directors, R&D heads and corporate strategy teams need to validate or recalibrate 3–5 year plans.

- Signal clarity. The report isolates the demand drivers that matter (end‑use shifts, purity specifications, and packaging/lot size economics) and correlates them with upstream feedstock constraints—enabling executives to prioritize interventions with quantifiable ROI.

- Actionability. Beyond headline forecasting, the study delivers executable playbooks: supplier risk matrices, sample contractual clauses for volume stability, and decision frameworks for build vs. buy debates.

What the report contains — pragmatic, transaction‑ready analysis

Readers will find deep, operational insight tailored to executives who must act in 2026 and beyond. Key deliverables include:

2,5-Dimethyl-2,4-Hexadiene Market

- Comprehensive market sizing and trend analysis (2020–2025 historical, 2026–2032 forecasts) with sensitivity scenarios that isolate the impact of feedstock stress, regulatory shifts and demand re‑segmentation.

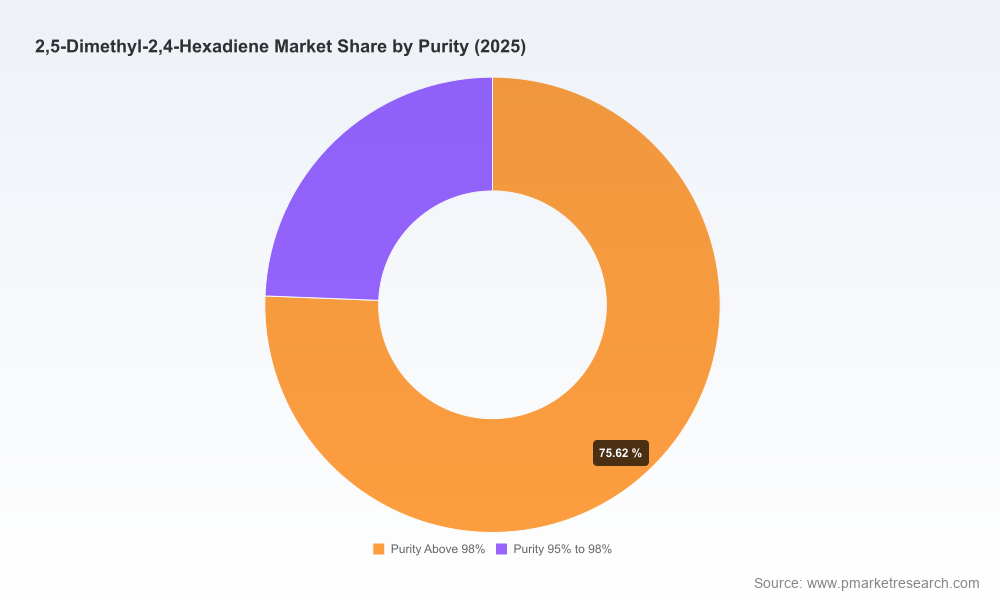

- A granular supplier taxonomy that differentiates reagent‑grade distributors, small‑scale traders, and bulk manufacturers—mapped against packaging, typical purity tiers, lead times and credit profiles.

- An upstream value chain diagnostic that traces synthesis routes, identifies critical bottlenecks and quantifies exposure to C4 hydrocarbon stream availability.

- Commercial playbooks: procurement scorecards, quality acceptance test (QAT) templates, and contract structures suited to both spot and long‑term procurement strategies.

- Investment and M&A heuristics, including target profiles for bolt‑on M&A (manufacturing scale vs. technology play) and scenarios identifying when on‑site production or tolling makes strategic sense.

- A downloadable financial model (Excel) that allows users to run custom sensitivity analyses on price, volume and feedstock shocks.

Competitive landscape — types of players and strategic postures

The 2,5-DMHD market is characterized by a mix of specialty distributors and commodity/bulk suppliers. The competitive map highlights three archetypes:

2,5-Dimethyl-2,4-Hexadiene Market

- Research/reagent distributors: globally recognized suppliers that service laboratory and high‑purity requirements, offering small packaging options and consistent batch documentation. Their value proposition centers on traceability, regulatory support and fast delivery to R&D customers.

- Domestic bulk traders/manufacturers: regionally focused suppliers, often based in Asia, that provide larger package sizes and commoditized pricing for industrial users. These players compete on volume flexibility and cost but vary in documentation and product stewardship.

- Mid‑tier distributors and formulators: companies that bridge laboratory needs and industrial demand by combining inventory services with packaging options and limited value‑add processing.

Market concentration is material: the top three firms control a substantial majority of the market while the top five capture an even larger share. This structure creates both opportunity and risk—stable, reliable supply through established names but limited contestability for large, long‑term contracts.

Supply chain and feedstock dynamics

The prevailing commercial synthesis pathways for 2,5-DMHD tie closely to C4 hydrocarbon streams—historical and technical literature point to acid‑catalyzed condensation routes using C4 derivatives such as isobutylene or isobutyraldehyde. As a result:

- Feedstock interdependence: availability and pricing for 2,5-DMHD correlate strongly with C4 throughput in petrochemical refineries and olefin crackers.

- Vulnerability to refinery economics: shifts in refinery utilization, changes in gasoline/delayed coking demand, or reallocation of C4 streams to higher‑value products can compress supply or introduce price spikes.

- Switching costs: for downstream processors specifying narrow purity and impurity profiles, switching suppliers is non‑trivial—requiring requalification, stability work and regulatory documentation.

Demand drivers and risk vectors

Demand is multi‑channel. A significant portion originates from the agrochemical space where 2,5-DMHD serves as an intermediate in certain insecticidal chemistry. Specialty organic synthesis—covering flavors, fragrances and fine chemical intermediates—represents a smaller but higher margin bracket that places a premium on consistent quality and traceable supply. Key risks and uncertainties that corporate leaders must weigh include:

- Regulatory shifts in pesticide approvals and formulations that could materially alter baseline consumption patterns.

- Feedstock supply shocks tied to refinery cycles or geopolitical disruptions in petrochemical hubs.

- Quality incidents and recalls that disproportionately penalize suppliers lacking robust batch testing and certification.

- Sustainability pressures: customers increasingly prefer intermediates with lower upstream carbon intensity or those produced via greener routes, which could re‑rank suppliers.

Strategic recommendations for 2026 (prioritized)

We advise chemical executives to treat 2026 as a year of proactive positioning. Priorities—ranked by immediacy and expected impact—are:

- Immediate (0–12 months): Strengthen procurement governance. Implement dual‑sourcing for critical grades, require full batch certificates and origin declarations, and negotiate short‑term volume collars to stabilize supply while preserving upside flexibility.

- Near term (12–24 months): Launch supplier qualification programs with preferred vendors that combine price, technical capability and ESG credentials. For organizations reliant on research‑grade inputs, prioritize distributors that can provide full traceability and expedited deliveries.

- Medium term (24–36 months): Evaluate tolling or captive capacity options where demand concentration and margin profile justify capital spend. Use our financial model to compare threshold volumes and payback under conservative feedstock price scenarios.

- Strategic/M&A (36+ months): Consider bolt‑on acquisitions of regional producers or long‑term offtake partnerships with feedstock owners to secure C4 streams. Alternatively, invest in R&D for less feedstock‑dependent synthetic routes that reduce exposure to petrochemical cycles.

Operational playbook — sample actions for commercial and technical teams

- Commercial teams: adopt a tiered contracting strategy—short‑term flexible buys for innovation projects, medium‑term agreements with volume options for production, and long‑term fixed‑price or indexed contracts for core volumes.

- Quality & technical teams: standardize acceptance testing and impurity thresholds; require supplier FAR (failure analysis reports) and set up periodic on‑site audits for strategic suppliers.

- R&D teams: prioritize impurity impact studies for the most common downstream chemistries and explore catalytic alternatives that could use more widely available feedstocks.

- Finance teams: stress‑test capex and supplier credit exposures against scenarios of elevated feedstock inflation and reduced availability in our downloadable model.

Regulatory and sustainability considerations

While 2,5-DMHD itself is an intermediate rather than an end product, two regulatory trends merit immediate attention: (1) tighter scrutiny on active ingredients and intermediates used in agrochemicals in several jurisdictions, and (2) the growing procurement preferences for low‑carbon intermediates in flavor, fragrance and pharmaceutical supply chains. Executives should incorporate supplier environmental metrics and regulatory roadmaps into vendor selection criteria—an approach that will increasingly differentiate trusted suppliers from pure price plays.

How PW Consulting’s study reduces execution risk

Where many market reports stop at high‑level forecasting, this study bridges to execution. Clients receive not only topline projections but also transaction‑grade artifacts: supplier scorecards, contract templates, QAT matrices, and the financial model mentioned above. For 2026 planning, these tools reduce ambiguity and accelerate decision cycles—turning strategic intent into operational commitments within fiscal timelines.

Concluding perspective and next steps

2,5-DMHD’s market is relatively small in absolute dollar terms but strategically important because of its role in higher‑value chemistries and its exposure to petrochemical feedstock dynamics. The market’s steady growth at a ~4.5% CAGR through 2032 masks meaningful volatility pockets that will drive winners and losers over the next 24 months. Companies that move early—by shoring up supplier relationships, formalizing quality regimes, and testing strategic sourcing or integration options—will preserve margin and optionality.

For corporate development teams, procurement leads and R&D directors preparing 2026 budgets and roadmaps, PW Consulting’s full report provides the granular, transaction‑ready intelligence needed to act with confidence. To access the complete dataset, supplier directory and downloadable scenario model, please visit our official report page or contact our industry practice for a tailored briefing.

For detailed analysis of this topic, please visit the official page:2,5-Dimethyl-2,4-Hexadiene Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com