Professional Printer Market Overview: Key Drivers and Challenges

Networking |

2026-02-20 10:43:52

PW Consulting today publishes an executive briefing that frames the strategic choices facing chemical formulators, specialty-mineral producers, and resource investors as the hectorite clays market moves from niche specialty ingredient to commercial-scale, performance-driven commodity. Built on a 2025 base year analysis and a detailed 2026–2032 forecast, our report synthesizes market sizing, competitive structure, technology developments, regulatory context, and actionable go‑to‑market playbooks designed to inform high‑stakes decisions in 2026.

Hectorite Clays Market

Hectorite is no longer an obscure laboratory clay. Between 2020 and 2025 the global market expanded noticeably, and our modelling projects continued growth across the 2026–2032 forecast window at a compound annual growth rate of 4.82%. That growth is uneven by end‑use but clear in aggregate: formulators in personal care, paints and coatings, drilling fluids, adhesives, and selected pharmaceutical applications are increasingly migrating to hectorite‑based rheology modifiers for their performance benefits. For buyers, suppliers and investors, the next 18 months will determine who captures premium formulation share and who remains a cost‑driven commodity supplier.

Hectorite Clays Market

Recovery and premiumization. After a cyclical trough in 2024, demand dynamics in 2025‑2026 show recovery driven by higher‑value personal care formulations and performance coatings. Premium product introductions and targeted marketing to cosmetic OEMs are supporting upgraded price structures in selective pockets of the market.

Hectorite Clays Market

Supply‑side differentiation. The sector is divided between natural hectorite (characterised by a scarce high‑grade natural resource base) and engineered synthetics / organo‑modified derivatives. Buyers are increasingly making sourcing decisions based on purity, sustainability credentials and lot‑to‑lot consistency rather than raw cost alone.

Technology & materials science. Recent peer‑reviewed work and industrial R&D are lowering technical barriers to producing mesoporous or tailored‑structure hectorite analogues. These developments expand application envelopes (e.g., adsorption, targeted release in pharma, enhanced dispersion in low‑VOC paints), creating product differentiation opportunities for early movers.

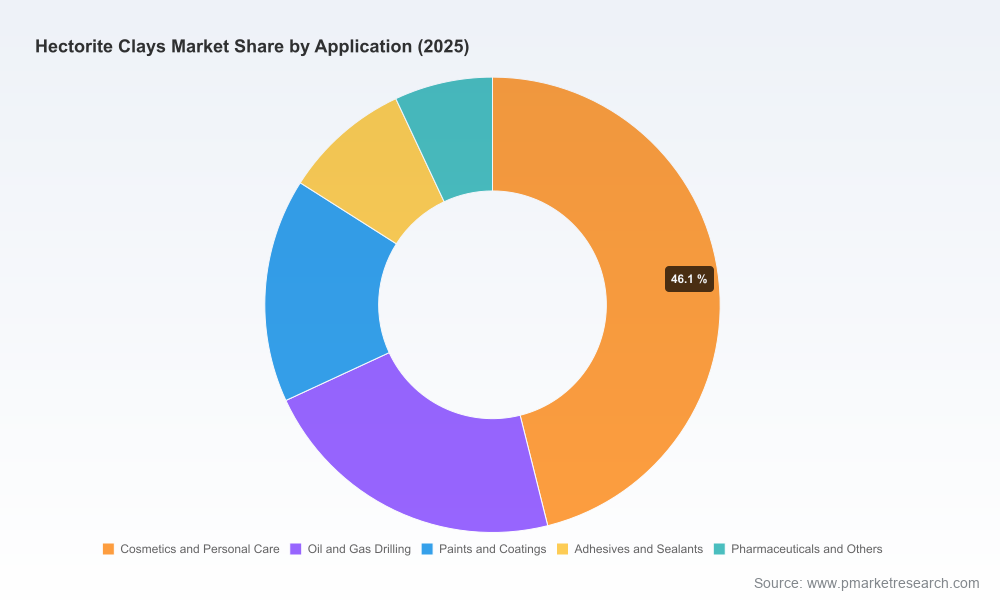

The hectorite market is best understood as three interlocking markets: native mineral hectorite, synthetic hectorite materials, and organically‑modified variants used for enhanced rheology and suspension. Application demand is anchored by cosmetics & personal care, and industrial uses such as drilling fluids, coatings, adhesives and pharmaceutical excipients. Rather than disclosing granular share numbers here, we highlight the strategic tensions:

Natural vs synthetic: Natural high‑purity hectorite confers a sustainability and marketing edge, particularly in regulated markets where environmental constraints favour mine‑certified sourcing. The Newberry Springs deposit — the primary high‑grade natural source currently in commercial production — provides a multi‑decadal resource base, but single‑source reliance introduces supply‑security risk that needs active mitigation.

Regulatory framing: Cosmetic formulators retain significant latitude: long‑standing safety assessments permit alkonium‑modified hectorite use at substantive concentrations in makeup preparations. That regulatory clarity supports innovation but also raises product stewardship expectations for suppliers around impurity profiles and traceability.

Environmental & ESG pressures: Stricter extraction standards in Europe and North America are shifting purchaser preference toward suppliers who can document responsible mining, lower life‑cycle emissions and reclamation commitments. This is creating commercial value for vertically integrated producers who can demonstrate compliance.

The commercial hectorite value chain is moderately concentrated. Our concentration metrics indicate that the top three firms capture a clear majority of market value, with the top five firms representing an even larger cumulative presence. That configuration produces defensible positions for established players, yet also leaves tactical spaces where specialized innovators can capture premium niches.

Elementis plc — With ownership and operation of the only major commercial high‑grade hectorite mine, Elementis occupies a unique upstream position. Its BENTONE family has been extended with targeted launches (including a new Hydroluxe line and custom Bentone ULTIMATE grades), signalling a deliberate strategy to translate upstream resource control into differentiated, high‑margin formulation solutions for personal care and coatings.

Asia‑based formulators and producers — Firms such as Zhejiang Camp‑Shinning and Jiangsu Hemings are focused on cost‑effective synthetic and organoclay solutions, competing on scale, formulation support and fast time‑to‑market for industrial applications including drilling and paints.

Specialty additives groups — Players including BYK (ALTANA), AMI, Tolsa, Kunimine, Minerals Technologies, Laviosa and dedicated cosmetic suppliers in China leverage formulation expertise, global distribution networks and customer partnerships to defend share. Several of these organisations also hold ISO and quality certifications that are decisive in industrial procurement.

Recent corporate activity underscores tactical priorities: Elementis’ product launches in 2024–2025 emphasise “natural activation” and bespoke rheological performance for personal care; parallel technical publications in 2026 describe steam‑assisted crystallization routes to mesoporous hectorite analogues—an innovation that could alter cost/performance tradeoffs between natural and synthetic offerings.

For boards and strategy teams, the choice set is clear: invest in capability or cede profitable niches to more focused competitors. PW Consulting recommends a seven‑point decision framework for 2026:

Secure diversified sourcing now. Even with a long resource life at primary natural deposits, single‑source exposure creates procurement risk. Multi‑sourcing strategies, long‑term offtakes and strategic inventory buffers are prudent.

Define a clear natural vs synthetic portfolio stance. Premium cosmetic and regulated European/NA channels are increasingly receptive to verified natural claims; industrial customers still prioritise consistency and cost. Align your commercial organisation accordingly.

Invest selectively in R&D partnerships. Technical advances such as mesoporous synthesis expand addressable markets. Early licensing or co‑development deals with universities or specialist producers can accelerate differentiated product timelines.

Embed ESG metrics into commercial contracts. Buyers are now asking for traceability, reclamation plans and emissions intensity. Suppliers who can certify these elements command a margin premium and faster acceptance in corporate tender processes.

Pursue bolt‑on M&A to close capability gaps. Given the sector’s concentration, targeted acquisitions of formulation houses, organoclay producers or regional distributors can be faster and more cost effective than organic scaling.

Operationalise regulatory certainty for marketing advantage. Where safety assessments exist (for example, documented cosmetic use concentrations), convert that into sales enablement tools for customers rather than mere compliance checklists.

Price & value engineering. Move beyond commodity bidding and develop value‑based pricing for performance attributes—suspension stability, tactile feel, low‑shear viscosity—backed by customer‑level WTP evidence.

Our full report is structured for decision execution, not just diagnosis. Highlights include:

Transparent market sizing and multi‑scenario forecasts from 2026–2032, with sensitivity analysis for material prices and regulatory shifts.

Competitive benchmarking across technical capability, upstream integration, certification, and channel coverage — with supplier positioning maps and defensible acquisition targets.

Procurement playbooks including recommended contract structures, hedge approaches, and inventory policies for different risk tolerances.

Product and formulation playbooks: specification templates, performance test protocols, and commercialization roadmaps tailored to cosmetics, coatings and industrial markets.

Regulatory and sustainability tracker that operationalises compliance checklists and ESG KPIs for procurement and product teams.

Scenario modelling tools for M&A and CAPEX decisions that quantify returns under alternate market growth pathways.

To preserve the strategic value of our analysis and to encourage direct engagement, we intentionally omit detailed segment‑level tables and certain proprietary splits from this press summary. Those granular asset‑level insights, supplier scorecards and price trajectories are provided in the full report and accompanying datasets available through PW Consulting.

If your 2026 planning cycle includes raw‑material sourcing, new product roadmaps or M&A screening, this is the right moment to turn market intelligence into a three‑year action plan. PW Consulting can mobilise a focused engagement to: stress‑test your supplier portfolio, assess acquisition targets, or design a product launch supported by formulation trials and customer willingness‑to‑pay studies. Contact our industry team via the PW Consulting portal to request the full Hectorite Clays Market report and the data workbook that underpins our forecast and supplier analysis.

Hectorite presents both a performance advantage and a strategic sourcing puzzle. Organisations that align procurement, innovation and sustainability in 2026 will capture disproportionate value as the market matures.

For detailed analysis of this topic, please visit the official page:Hectorite Clays Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com