Paper Laminates Market 2026: Strategic Intelligence for Executive Decision‑Making

Executive preview

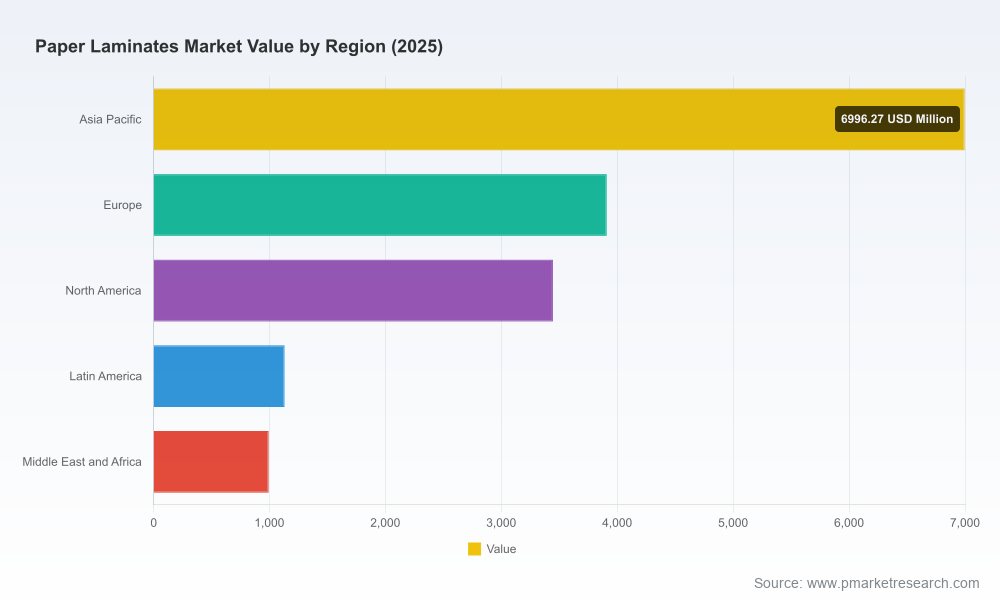

PW Consulting’s newest market study on Paper Laminates—anchored on a 2025 base year and covering historical performance (2020–2025) with forecasts to 2032—delivers the actionable intelligence senior teams need to set strategy for 2026 and beyond. The global paper laminates market is projected to continue expanding at a mid-single‑digit trajectory (compound annual growth rate: 5.48% over the forecast window), with total market value reaching the multi‑billion USD scale by the end of the period. This release is designed as a “trailer”: it surfaces the strategic signals, risk vectors and competitive moves that matter for near‑term choices, while directing decision‑makers to the full report for transaction‑grade segment and regional tables.

Paper Laminates Market

Why this report matters for 2026 decisions

- Timing for capital allocation: The market’s steady CAGR and uneven regional demand curves mean capacity, retrofit and M&A timing will materially affect returns. Executives must translate demand momentum into staging and sizing decisions in 2026.

- Regulatory inflection points: New mandates on recyclate content and extended producer responsibility are changing product specifications and provider responsibilities—companies that act early will gain time‑to‑market advantages.

- Margin management in a volatile input environment: Raw material cost swings are compressing gross margins for exposed players. Procurement and pricing playbooks are now central to commercial strategies.

- Innovation and certification are table stakes: Recyclability, mass‑balanced solutions and certification (e.g., ISCC) are rapidly becoming procurement filters for large brand owners and retailers.

Key takeaways—what senior teams should know now

- Growth is resilient but heterogeneous: Overall market value has expanded through 2025 and is projected to grow through 2032 at ~5.5% CAGR. Demand drivers include packaging substitution (paper for certain plastics), construction and furniture refurbishment cycles, and growth in aseptic and foodservice formats.

- Fragmented competitive structure: The paper laminates landscape remains moderately fragmented—top players capture a meaningful share but do not dominate end‑to‑end value chains in all geographies. This opens opportunities for focused scale plays and niche differentiation.

- Input cost volatility is a strategic lever: Key benchmarks show notable price points for primary inputs—bleached hardwood kraft pulp and LDPE resin have seen meaningful movement in recent quarters—creating both margin pressure and arbitrage opportunities for vertically integrated operators.

- Regulatory deadlines are predictable breakers: Binding targets on recycled content and packaging EPR timelines compel product redesign and supplier engagement plans that cannot be deferred beyond 2026 without commercial consequences.

What the report contains—practical, operational intelligence

The PW Consulting report is structured to convert insight into action. Core deliverables include:

Paper Laminates Market

- Top‑down market sizing and a bottoms‑up, SKU‑level demand model that rolls up to regional and global forecasts (2026–2032). The model is delivered as a configurable spreadsheet so clients can run bespoke scenarios.

- Price‑and‑cost build‑ups for common laminate constructions, reflecting current pulp and polymer benchmarks and variable logistics inputs to calculate margin sensitivities.

- Regulatory heatmaps and a compliance road‑map by jurisdiction that translate mandates (recyclate targets, EPR, single‑use plastic rules) into product action items and capex timelines.

- Commercial playbooks for product positioning, tendering strategies and channel segmentation—designed for CPGs, converters and paper producers alike.

- A supplier ecosystem map, with capability matrices and readiness scoring against sustainability and barrier performance criteria.

- Deal playbooks and valuation guidance for acquisition targets, including a check‑list of technical, compliance and integration risks.

Note: the public summary above intentionally omits the granular regional and end‑use split tables contained in the full deliverable. Those datasets and model access are available via the report page.

Paper Laminates Market

Competitive landscape—profiles and strategic moves

The market is shaped by a mix of traditional paper and packaging majors, specialty laminators and technology licensors. Key incumbents covered in the report include:

- Mondi Group (Vienna, Austria) — https://www.mondigroup.com — A global leader in paper‑based packaging solutions, Mondi is pushing recyclable flexible packaging with new peel & seal laminate formats that balance consumer convenience with recyclability.

- WestRock Company (Atlanta, GA, USA) — https://www.westrock.com — With strong extrusion coating and carton capabilities, WestRock is focused on high‑barrier fiber‑based laminates targeted at shelf‑stable and greasy food formats.

- Smurfit Kappa Group (Dublin, Ireland) — https://www.smurfitkappa.com — A major supplier of laminated paperboard, Smurfit Kappa has recently advanced recycled‑content credentials through ISCC PLUS certification, accelerating acceptance among sustainability‑driven buyers.

- International Paper Company (Memphis, TN, USA) — https://www.internationalpaper.com — Strong in corrugated and specialty laminates, International Paper continues to leverage polymer film laminates for enhanced barrier products and industrial uses.

- DS Smith plc (London, UK) — https://www.dssmith.com — DS Smith emphasizes sustainable extrusion‑laminated papers for e‑commerce and food, aligning packaging performance with recyclability targets.

- Tetra Laval (Tetra Pak) (Pully, Switzerland) — https://www.tetrapak.com — A specialist in aseptic multi‑layer laminates, Tetra Pak remains the reference for liquid carton technology and increasingly hybrid materials that balance barrier and recyclability.

- Stora Enso Oyj (Helsinki, Finland) — https://www.storaenso.com — Advancing renewable laminates and barrier coatings as plastic alternatives, Stora Enso’s commercial scale‑ups of mass‑balanced laminates change competitive dynamics for high‑value applications.

Recent corporate activity underscores three strategic themes: certification and recycled content wins (e.g., ISCC updates), new product launches aimed at recyclable flexible packaging, and capacity investments for mass‑balanced solutions. These moves are shifting supplier selection criteria from price alone to combined sustainability performance and supply reliability.

Market dynamics and near‑term signals to watch

- Raw material dynamics: Bleached hardwood kraft pulp and polyolefin laminates remain core cost drivers. For example, industry indexes reported notable pulp prices in late 2025 and LDPE resin prices in early 2026—both creating short‑term margin pressure for non‑integrated producers and input arbitrage opportunities for vertically integrated players.

- Regulatory regime shifts: The European Packaging and Packaging Waste Regulation (PPWR) sets minimum recycled content targets that will materially change compositional standards by the end of the decade. In the U.S., state‑level initiatives (e.g., California’s EPR rules) already require supply‑side planning and financial provisioning.

- Recyclability thresholds and design rules: Circularity standards and single‑use plastic restrictions are forcing technical redesigns—some laminate constructions will be non‑compliant in certain markets unless reformulated or accompanied by recovery systems.

- Procurement and retailer dynamics: Large retail consolidators and brand owners are increasingly scoring suppliers on certification, mass‑balance reporting and traceability; these non‑price criteria are becoming gatekeepers for preferred supplier lists.

Strategic recommendations for 2026

- Prioritize certification and product redesign: Invest in third‑party certification and pilot recyclable constructions now. The cost of delayed compliance will be higher than early reengineering.

- Hedge input risk and consider vertical moves: Locking in pulp and polymer supply through contracts or JV arrangements reduces margin volatility. For some players, selective upstream or downstream integration can unlock margin and security benefits.

- Segment‑focused commercial plays: Use channel and application analyses to allocate R&D and sales resources; not all end uses will grow equally, and premium segments reward value‑added barrier performance and sustainability credentials.

- Data‑driven M&A and partnerships: Target acquisitions that deliver either technical competencies (barrier chemistries, lamination lines) or rapid access to certified feedstock and recovery systems.

- Prepare flexible manufacturing and conversion capacity: Design retrofit road‑maps that allow shifts between laminate constructions without large downtime, enabling response to regulatory changes or customer specification shifts.

How to use this report

Senior management teams will find the report useful for board briefings, investment committee reviews, procurement renegotiations and product roadmap prioritization. The included scenario model lets teams stress‑test assumptions—price shocks, regulatory timelines and technology adoption curves—and produce finance‑grade forecasts for capex and working capital planning. For transaction teams, the supplier benchmarking and integration checklist reduce due diligence time and surface deal breakers early.

Next steps & access

This executive preview highlights the strategic vantage points our Paper Laminates Market report offers to organizations making critical choices in 2026. The full report contains the granular regional and application split tables, supplier scorecards, and downloadable forecasting model referenced above. To obtain the complete study or to commission a tailored briefing and model‑customization workshop, please contact PW Consulting via our report page.

Methodology note

Our analysis combines primary interviews with manufacturers, converters and brand procurement leads, transaction databases, and price series from industry indexes. Forecasts are built on a mixed top‑down and bottoms‑up approach, stress‑tested across three adoption scenarios. The historical series covers 2020–2025 with a base year set at 2025, and forecasts extending through 2032.

For detailed analysis of this topic, please visit the official page:Paper Laminates Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com