PW Consulting Releases Strategic Brief: Hydrocracker Market Outlook to 2026–2032

PW Consulting today publishes a forward-looking industry brief that distills our Hydrocracker Market research into a strategic playbook for decisions companies must make in 2026. Built on a detailed base-year analysis (2025) and a seven-year forecast horizon (2026–2032), the brief translates macro momentum into concrete choices for refiners, petrochemical licensors, catalyst suppliers, and capital providers. The global hydrocracker market—having reached roughly USD 75.7 billion in 2025—is projected to sustain mid-single-digit growth and move meaningfully higher through 2032 (our forecast indicates the market will exceed USD 110 billion by 2032 at a 5.5% CAGR). This trajectory creates windows for capacity investments, technology upgrades, and supply-chain repositioning that will determine winners over the next decade.

Hydrocracker Market

Why this report matters for 2026 corporate strategy

- Capital prioritization: With constrained balance sheets and competing low-carbon investments, refinement of CAPEX timing and scope for hydrocrackers is now table stakes.

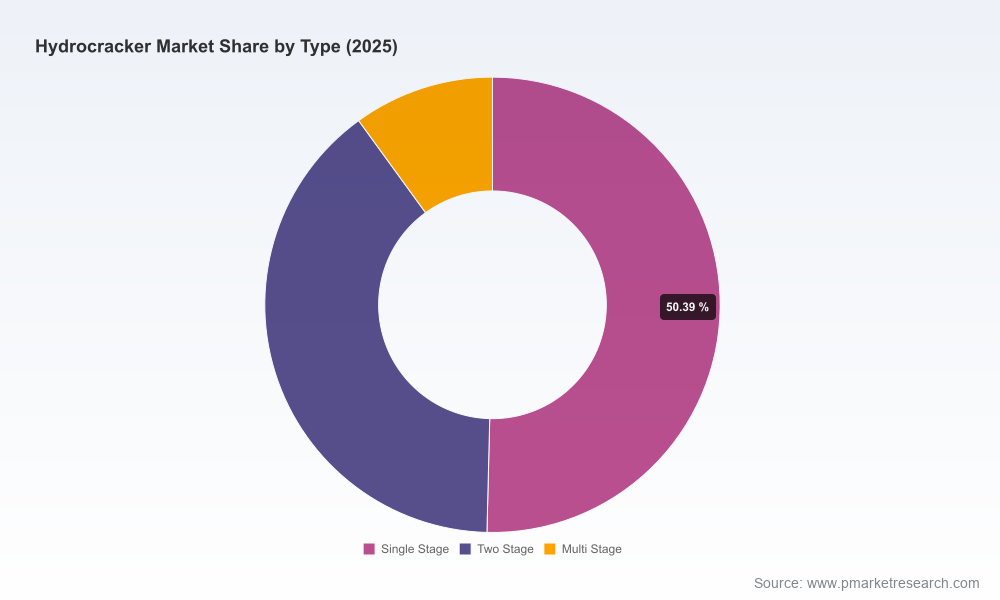

- Technology selection under uncertainty: Licensing choices (fixed-bed vs. ebullated-bed, single-stage vs. multi-stage architectures) have multi-decade implications for yield flexibility and feedstock tolerance.

- Feedstock and product mix risk: The shift toward heavier crude slates and the simultaneous need for ultra-low-sulfur middle distillates force a re-evaluation of feedstock procurement and product off-take strategies.

- Supply-chain resilience: Catalyst lead times, licensing partnerships, and local manufacturing capacity will shape both project schedules and operating economics.

- Regulatory compliance and market access: Tightening fuel-quality standards and evolving IMO and national regulations change the return profile for hydrocracking projects across different markets.

What the PW Consulting Hydrocracker report delivers (practical modules)

- Investment Prioritization Framework — a decision matrix that aligns project size, desired product slate, and feedstock risk with expected return profiles under multiple scenarios.

- Staged CAPEX and Execution Roadmaps — phased implementation plans to de-risk construction, align with hydrogen availability, and optimize commissioning schedules.

- Technology Selection Toolkit — comparative assessments of proven licensors and process families for common refinery objectives (middle distillate maximization, naphtha push, base oil integration), with pragmatic guidance on when to favor ebullated-bed vs. fixed-bed solutions.

- Catalyst Procurement & Risk Playbook — strategies for dual sourcing, inventory sizing, on-site regeneration options, and negotiating performance guarantees that minimize unplanned downtime.

- Feedstock Sensitivity Models — scenario-driven outputs that translate changes in crude slate and vacuum residue availability into yield and margin impacts.

- Regulatory Compliance Pathways — checklists and country-specific compliance triggers to align financing and build timelines with enabling legislation and fuel standards.

- Competitive Benchmarking & Vendor Heatmaps — qualitative and quantitative supplier profiles designed to inform partner selection without exposing confidential contract-level data.

- Case Studies & Field Validation — project-level learning from recent unit start-ups and expansions that validate best practices for commissioning and early operations.

Market dynamics shaping 2026 decisions

Several structural forces converge to make 2026 a pivotal year for hydrocracking strategy. First, tightening clean-fuel regulations continue to drive demand for ultra-low-sulfur diesel and jet fuel. Second, refiners in regions processing a rising share of heavy and extra-heavy crudes need technologies that can convert low-value residues into high-value middle distillates and naphtha. Third, the rise of integrated crude-to-chemicals complexes is increasing strategic demand for naphtha, altering the traditional refinery product-mix calculus. Finally, the technology landscape is itself evolving: licensors and catalyst houses are introducing process families and catalyst formulations optimized for flexibility and higher convertibility, enabling refiners to pivot product slates in response to market signals.

Hydrocracker Market

Competitive landscape — who matters and why

The hydrocracker ecosystem is shaped by a set of technology licensors, catalyst manufacturers, and large operating refiners whose strategies create both competitive pressure and partnership opportunities. The market exhibits a moderate-to-high level of concentration: a handful of established licensors and catalyst suppliers routinely dominate licensing flows and aftermarket sales, while national and integrated players deploy in-house capabilities at scale.

Hydrocracker Market

- Honeywell UOP (Des Plaines, Illinois, USA) — a long-standing licensor of Unicracking and related hydrocracking process families. Their value proposition centers on mature licensing packages, strong catalyst portfolios for distillate and naphtha pathways, and global aftermarket support. For firms prioritizing proven routes and predictable commissioning, UOP remains a core option.

- Axens (Rueil-Malmaison, France) — notable for its H-Oil ebullated-bed residue hydrocracking and HyK distillate hydrocracking offerings. Axens’ track record in high-conversion, naphtha-maximizing units makes it a natural partner for crude-to-chemicals strategies and projects seeking flexibility between distillates and naphtha.

- Shell Catalysts & Technologies (Houston, Texas, USA) — emphasizes zeolite-based catalysts that drive distillate selectivity and flexibility; attractive to operators seeking high-performance catalyst suites alongside process know-how for complex slates.

- Chevron Lummus Global (Richmond, California, USA) — with Isocracking and LC-Fining families, CLG is often selected by firms requiring deep residue upgrading and fixed-bed/ebullated-bed hybrid approaches.

- Topsoe (Lyngby, Denmark) — positions itself on reliability and high-performance catalysts that enable flexible product distribution (naphtha, diesel, base oils). Topsoe’s offerings are compelling for projects where uptime and product-quality consistency are prioritized.

- Albemarle, BASF, Johnson Matthey, Sinopec Catalyst and others — these catalyst specialists and manufacturers supply the performance-critical chemistries that determine unit run length, regenerability, and selectivity. Their commercial strategies (local manufacturing, long-term supply agreements, performance guarantees) will be decisive inputs to procurement choices.

- ExxonMobil and major integrated refiners — as both operators and licensors, large integrated players can alter competitive dynamics through proprietary process adoption, scale economics, and in-house upgrading projects.

Recent field activity reinforces the momentum we model. Notable starts and contract awards in the last 24 months reflect both demand and the tangible deployment of new units and catalyst supply chains. These real-world developments validate the forecasting sensitivity embedded in our models and highlight the practical timeframes teams should expect from sanction to commercial operation.

Actionable recommendations for 2026 decision-makers

- Prioritize flexible technologies that allow toggling between naphtha push and distillate maximization; flexibility is a hedge against demand and regulatory volatility.

- Secure catalyst supply arrangements early, with clauses for performance-based replacement and secondary sourcing to mitigate lead-time shocks.

- Structure CAPEX in phases aligned to hydrogen availability and carbon management solutions; avoid full upfront exposure when alternative decarbonization pathways remain uncertain.

- Integrate feedstock scenarios into commercial negotiations—counterparties often underprice the operational uplift that hydrocrackers provide to heavy-slates.

- Evaluate licensing partners not only on technical fit but on aftermarket service footprints and local manufacturing capability for critical spare parts and catalysts.

- Use modular contracting and EPC frameworks that allow scope adjustments during engineering without derailing schedules—especially important for greenfield projects tied to larger petrochemical expansions.

- Embed fuel-quality regulatory triggers into sanction criteria so that financing, construction, and commissioning are aligned with market access timelines.

How PW Consulting’s Hydrocracker report helps you act

This strategic brief is an executive distillation of a comprehensive report that combines legacy project intelligence, vendor benchmarking, and scenario models. Subscribers receive:

- Interactive financial models (base / upside / downside) calibrated to actual start-up timelines and hydrogen cost assumptions.

- Vendor heatmaps and negotiation playbooks to shorten procurement cycles and reduce commercial risk.

- Implementation roadmaps that translate sanction decisions into 12, 24, and 36-month milestones with contingency options for feedstock and regulatory shifts.

- Scenario-driven sensitivity analyses that quantify the margin impact of feedstock quality and product slate choices without exposing proprietary segment-level data.

PW Consulting’s Hydrocracker Market research is purpose-built for executives and investment committees who must make binding decisions in 2026 that will shape their competitive position for the rest of the decade. The research demonstrates where value is emerging, which technology paths are defensible, and how to operationalize supply-chain resilience. For organizations considering new units, upgrades, or strategic partnerships, the report supplies the decision templates and risk-calibrated scenarios needed to move from analysis to action.

To access the full data suite, vendor benchmarking matrices, and scenario models—including the detailed annualized market projections and our proprietary baseline assumptions—please refer to the report landing page. PW Consulting stands ready to provide tailored briefings and modelling workshops to support your 2026 sanction decisions and beyond.

For detailed analysis of this topic, please visit the official page:Hydrocracker Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com