Gamma Knife Radiosurgery (GKRS) Market Research: Strategic Preview for 2026 Decision-Makers

PW Consulting today releases a strategic preview of our upcoming Gamma Knife Radiosurgery (GKRS) Market Research report — a practical intelligence product built to support hospital system leaders, device manufacturers, private equity investors, and technology strategists making consequential GKRS decisions in 2026. The global GKRS market has demonstrated resilient expansion through the mid‑2020s and, under a conservative base-case trajectory, is forecast to sustain above‑market growth into the early 2030s. Our analysis combines clinical program insight, capital‑equipment economics, regulatory dynamics, and competitive mapping to translate market signals into executable choices — without revealing the proprietary segment tables reserved for the full report.

Gamma Knife Radiosurgery Gkrs Market Research

Why 2026 Is a Strategic Inflection Point

- Capital cycles: Several health systems are updating imaging and radiosurgery suites after pandemic‑era deferments; 2026 procurement timelines will determine vendor share for the next decade.

- Clinical expansion: Emerging indications and newly cleared indications are shifting the value proposition of GKRS beyond traditional tumor care into functional neurosurgery pathways.

- Payer scrutiny and price signalling: Reimbursement variability and procedure-level technical charges are influencing hospital service line economics and capacity planning.

- Source management and compliance: The unique radiation‑source lifecycle for GKRS systems creates long‑lead regulatory and decommissioning considerations that must be embedded in 2026 CAPEX decisions.

Macro Takeaways — Market Scale and Trajectory

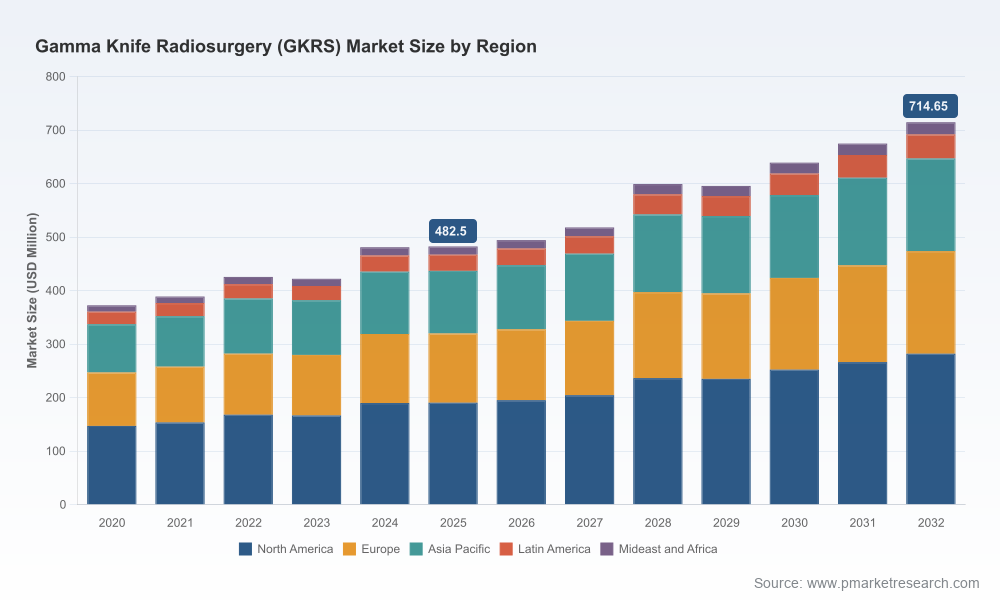

PW Consulting’s base-year analysis positions the global GKRS market at roughly USD 482.5 million in 2025. From a five-year historical perspective, the market tracked steady recovery and selective acceleration across clinical and geographic pockets. Looking forward through our 2026–2032 forecast horizon, the market is expected to expand at a compound annual growth rate (CAGR) of approximately 5.76%, with the market size increasing meaningfully by the end of the period under base‑case assumptions.

Gamma Knife Radiosurgery Gkrs Market Research

Competitive concentration in GKRS remains high — the segment is dominated by a small number of established suppliers with deep installed bases and specialized clinical ecosystems. This concentration has concrete implications for procurement leverage, aftermarket margins, and the structure of maintenance and service agreements.

Gamma Knife Radiosurgery Gkrs Market Research

What the Report Delivers — Practical, Transactional, and Operational Components

PW Consulting designed this research product as an actionable playbook for the 2026 decision‑maker. Key practical deliverables included in the full report are:

- Decision trees for buy vs. partner vs. outsource scenarios, with sensitivity analyses for patient volume, payer mix, and treatment mix.

- Capital planning frameworks that quantify total cost of ownership across equipment options, including acquisition, installation, radiation‑source management, facility retrofit, and end‑of‑life decommissioning pathways.

- Reimbursement mapping and payer engagement templates that translate procedure economics into revenue and margin scenarios for single‑fraction GKRS programs versus multi‑purpose linac alternatives.

- Regulatory and radiation safety checklists tailored to hospital operators and vendors, outlining compliance milestones and timeline risks specific to cobalt‑60 source management.

- Operational playbooks for clinical program deployment: referral pathway development, multidisciplinary governance, throughput optimization, and staffing models for neurosurgery and radiation oncology teams.

- Service contracting models and aftermarket strategies: benchmarking of standard service terms, SLA constructs, spare parts provisioning, and lifecycle revenue levers.

- Investor and M&A guidance: screening criteria, valuation sensitivities, and integration risks for strategic and financial buyers targeting GKRS platform owners or service providers.

- Scenario planning: upside and downside cases driven by regulatory changes, reimbursement shocks, and disruptive technology entrants.

Competitive Landscape — What Matters Beyond Brand

The GKRS supplier landscape is characterized by a combination of long‑tenured platform leaders and regional alternatives. Institutions selecting GKRS solutions should evaluate three supplier dimensions beyond headline brand: installed clinical evidence and site references; aftermarket and service economics; and strategic breadth of indications supported by product roadmaps.

- Elekta AB (Stockholm, Sweden) — Elekta remains the incumbent and primary supplier of Leksell Gamma Knife systems. Its portfolio depth of platform variants and consumable accessory ecosystems creates high switching costs for established programs. Notably, Elekta received regulatory clearance in mid‑2025 to expand an important therapeutic label into adult refractory mesial temporal lobe epilepsy (MTLE), a development that materially broadens potential procedural volumes for centers that can operationalize cross‑discipline pathways.

- MASEP Medical Science & Technology Development (China) — MASEP’s rotary gamma systems represent a regional alternative with cost and deployment tradeoffs. For organizations considering regional supply diversification or lower-capex entry points, these entrants warrant capability and lifecycle evaluation against full‑service incumbents.

- American Radiosurgery Inc. (United States) — Offers a rotating gamma system positioned for radiosurgery applications. For U.S. operators, domestic manufacturers can present logistical and service advantages in terms of training, spares, and regulatory alignment.

Across these suppliers, the strategic questions for hospitals and buyers in 2026 will center on indications expansion, aftermarket certainty, and platform flexibility versus dedicated intracranial specialization.

Dynamics to Watch — Reimbursement, Regulation, and Clinical Positioning

- Reimbursement variance: Procedure‑level reimbursement and hospital chargemaster differentials create notable economic asymmetry between patient pathways using dedicated GKRS platforms and multi‑purpose linear accelerators. Hospitals must model not only per‑case reimbursement but the downstream revenue impact from referrals and program reputation.

- Regulatory safety and lifecycle obligations: GKRS systems that use radioactive sources carry regulatory obligations for installation, operation, and decommissioning that can extend over decades. These obligations materially affect project timelines, capital provisioning, and vendor selection criteria.

- Clinical evidence and indication growth: The 2025 clearance expanding GKRS indications into refractory epilepsy illustrates how regulatory approvals can unlock new patient cohorts. Translating such approvals into incremental volumes is an operational exercise requiring alignment across neurosurgery, neurology, radiation oncology, and payer strategy.

Strategic Recommendations for 2026 Decision-Makers

- Embed lifecycle cash flows into procurement decisions. Do not evaluate purchase price in isolation — include installation, source management, decommissioning, and opportunity costs from OR/IMAGING footprint constraints.

- Negotiate service‑first agreements. Given the high aftermarket share in GKRS economics, buyers should prioritize transparency on parts pricing, consumables, and multiyear SLA performance guarantees.

- Design clinical programs around referral capture and payer contracting. Successful GKRS programs are those that convert regulatory and clinical advantages into durable payer arrangements and referral networks.

- Assess strategic optionality vis‑à‑vis platform specialization. For systems expecting to prioritize intracranial radiosurgery volume and long‑term clinical differentiation, dedicated GKRS platforms may deliver superior outcomes; for organizations that need flexibility, multi‑purpose linac solutions may offer better capital utilization.

- Factor concentration risk into supplier selection. High market concentration means vendor outages or shifts in service strategy can have outsized local operational impacts — develop contingency plans for parts and cross‑training.

- Use staged deployment playbooks. For greenfield programs, adopt a phased approach that ties incremental capital commitments to achievement of clinical and revenue milestones.

How to Use the Full Report

This press preview highlights the analytical themes and the practical utility our full GKRS Market Research delivers. The comprehensive report contains the proprietary segmentation matrices, detailed regional and indication modeling, vendor revenue/market‑share estimates, and downloadable financial models that underpin the scenarios referenced above. PW Consulting’s clients use these materials to stress‑test procurement decisions, structure vendor negotiations, and prioritize target lists for strategic investments or partnerships heading into 2026.

If your organization is preparing a capital or clinical investment case for GKRS, PW Consulting’s full report is designed to accelerate decision velocity while reducing execution risk. Visit our report page to review the executive summary, request a tailored briefing, or obtain the full dataset and model access for use in board‑level deliberations.

PW Consulting — translating GKRS market complexity into clear, executable strategies for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Gamma Knife Radiosurgery Gkrs Market Research

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com