Gymivorbereitung Zürich – Erfolgreich lernen mit Effektiv Lernen

Other |

2026-06-29 07:34:14

PW Consulting’s new market study, “High Performance Fibers For Defense Market,” provides an actionable intelligence package for executives and procurement leaders preparing 2026 strategies. Built on a validated historical baseline (2020–2025) and a forward-looking forecast (2026–2032), our proprietary model shows the defense-focused high-performance fiber market growing at a sustained compound annual growth rate (CAGR) of 8.52% from the 2025 base. By 2032, the market is expected to be materially larger than today — a trajectory that reshapes supplier selection, qualification timelines, and capital allocation choices across defense primes, tier-1 suppliers, and national agencies.

High Performance Fibers For Defense Market

Timing of procurement and qualification. Qualification timelines for defense-grade materials remain lengthy (commonly 2–5 years). Decisions made in 2026 will determine supplier footprints and material availability for programs launching in the second half of the decade.

High Performance Fibers For Defense Market

Supply resilience vs cost pressure. Raw-material volatility and manufacturing capital intensity are converging to create differentiated supplier economics — a key input to long-term sourcing strategies and risk hedging.

High Performance Fibers For Defense Market

Technology inflection points. Recent product and grade introductions are accelerating the substitution of legacy solutions, forcing engineering and procurement teams to reconcile performance gains with qualification risk and total cost of ownership.

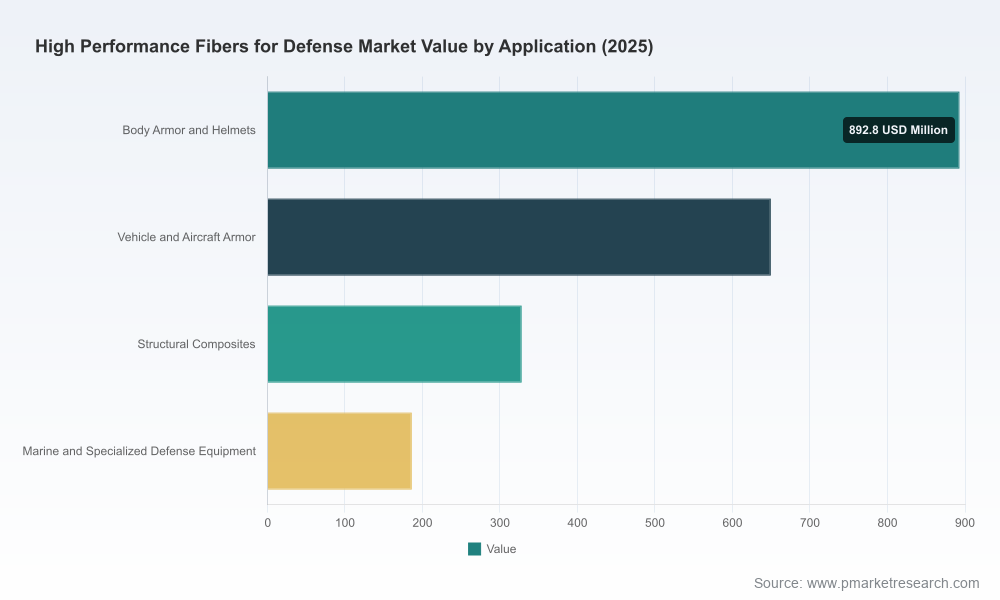

The market’s mid-single-digit-to-high-single-digit growth path reflects several durable defense demand drivers: modernization of personnel protective systems, increased adoption of fiber-reinforced composites for air and ground platforms seeking weight reduction, and expanding requirements for specialized marine and protective equipment. Policy-backed defense procurement budgets and modularization of platforms underpin predictable volume growth for the foreseeable horizon.

From a strategic viewpoint, an 8.52% CAGR implies that suppliers able to scale production reliably and partners who secure long-term material access will capture outsized commercial opportunities. Conversely, late entrants and actors with limited qualification pipelines risk missing multi-year program windows even if their materials offer compelling laboratory performance.

Market concentration and negotiating leverage: The sector shows notable concentration among established incumbents. That dynamic supports disciplined price realization for trusted suppliers while creating procurement friction for buyers seeking greater competition. Strategic sourcing must therefore balance competitive tension with the operational realities of supplier scale and qualification status.

Raw material and process sensitivity: Para-aramid precursors (e.g., PPD/TPC feedstocks) and UHMWPE gel-spinning routes expose manufacturers to petrochemical and solvent cycles. These upstream sensitivities can compress margins or spur price pass-throughs during commodity shocks — a factor critical to contract design and budget forecasting in 2026.

Capital intensity and manufacturing footprint: UHMWPE and advanced carbon fiber production require high-capex lines and solvent recovery systems. Decisions to invest in greenfield capacity or to enter supply agreements should weigh lead times, environmental permitting, and the long tail of qualification testing.

Regulatory and export complexity: Export controls and defense-related trade restrictions materially influence where certain specialty fibers can be shipped and processed. For program architects and global primes, this adds a layer of geopolitical supply planning that must be embedded in sourcing policies.

Product innovation is accelerating along two vectors: higher specific strength/modulus and system-level integration (e.g., hybrid laminates, shield architectures). Recent notable industry moves illustrate this trend — suppliers have announced high-modulus carbon fiber grades, extended supply agreements to secure capacity, and portfolio expansions of ballistic aramids and UHMWPE variants. These initiatives are not just incremental: they affect substitution dynamics between fiber classes, enable lighter systems, and shorten lifecycle costs when engineering trade-offs are correctly assessed.

The market is anchored by a set of established players with complementary capabilities across para-aramids, UHMWPE, and carbon fibers. Each brings a distinct strategic posture:

Incumbent aramid leaders provide certified ballistic fibers widely qualified for military and law enforcement programs; their value proposition is reliability and legacy qual histories.

Large chemical and advanced-material groups combine R&D scale with global manufacturing footprints to execute long-term supply agreements and support major aerospace suppliers.

Specialist UHMWPE producers leverage gel-spinning mastery to deliver ultra-light ballistic solutions — but their high capex per ton makes capacity additions selective and often backed by long-term offtakes.

Recent strategic developments in the sector reinforce these dynamics: long-term supply agreements to secure capacity, launches of higher-performance carbon fiber grades geared to aerospace defense, and portfolio expansions within ballistic aramids. These moves validate that market leaders are preparing for a materially larger, higher-performance defense materials market over the next decade.

Designed as a working toolkit for 2026 decision cycles, the report blends quantitative forecasting with executable recommendations and templates. Key deliverables include:

A transparent market model (base year 2025) with top-down and bottom-up scenario runs across the 2026–2032 forecast window, enabling buyers and investors to stress-test program-level demand.

Supplier benchmarking and capability mapping: manufacturing technology, qualification readiness, lead times, margin profiles, and strategic posture.

Cost build-ups and sensitivity analyses that isolate raw-material exposure, solvent/recovery economics, and labor/capex impacts for different fiber classes.

Procurement playbooks and contract archetypes: recommended clauses for price adjustment, capacity reservation, quality audits, and exit/transition planning aligned to multi-year defense programs.

Qualification acceleration templates: test matrices, trusted test houses, and realistic timelines to compress the typical 2–5 year qualification window where feasible.

Risk heatmaps covering regulatory constraints, supply shock scenarios, and mitigation strategies (dual sourcing, buffer inventory, regionalized supply).

Short term (0–12 months): • Accelerate supplier audits and lock strategic framework agreements for critical fibers; • build staged safety stock aligned to program milestones; • secure price mechanisms tied to raw-material indices with defined floors/caps.

Medium term (1–3 years): • Invest in qualification pipelines for promising alternative fibers or hybrid architectures; • consider joint ventures or capacity-sharing with established suppliers to reduce time-to-market; • deploy scenario-based capex plans reflecting the report’s 8.52% CAGR baseline and upside contingencies.

Capability bets to evaluate: recycling/closed-loop recovery for composite waste, solvent recovery modernization for UHMWPE, and selective vertical integration into precursor chemistry where supply constraints and economics justify it.

The study synthesizes primary interviews with material suppliers, defense OEMs, and testing authorities; proprietary shipment and capacity datasets; plus bottom-up cost models. Our base-year calibration uses audited 2025 industry performance and aligns to macro procurement cycles to produce actionable scenarios for 2026 planning. Importantly, the report intentionally withholds certain granular segmentation tables and line-item forecasts from this preview to preserve the practical commercial value for subscribers.

For leaders shaping offensive and defensive material strategies in 2026, the choice is clear: treat high-performance fibers as a strategic input rather than a commodity. The market’s projected growth and the concentrated supplier landscape create both opportunity and vulnerability. PW Consulting’s full report equips you with the granular segmentation, supplier scorecards, and contract templates needed to move from awareness to implementation — while our scenarios help you align procurement cadence, manufacturing investment, and technology partnerships to program timelines.

To access the complete dataset, segmented forecasts, supplier profiles, and downloadable procurement templates, visit the report landing page. The core segmented forecasts and supplier-level financials are available exclusively in the full publication and are intentionally omitted from this preview to preserve strategic value.

For detailed analysis of this topic, please visit the official page:High Performance Fibers For Defense Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com