PW Consulting: Strategic Brief — Submarine Air-Independent Propulsion (AIP) System Market Outlook to 2032

Executive overview

PW Consulting today publishes an executive-level preview of our forthcoming Submarine AIP System Market report (base year 2025). The market for submarine AIP systems has demonstrated resilient, structural growth through recent years and — driven by diversified procurement programs, incremental fuel-cell adoption, and targeted platform integrations — is projected to continue expanding across the 2026–2032 forecast window.

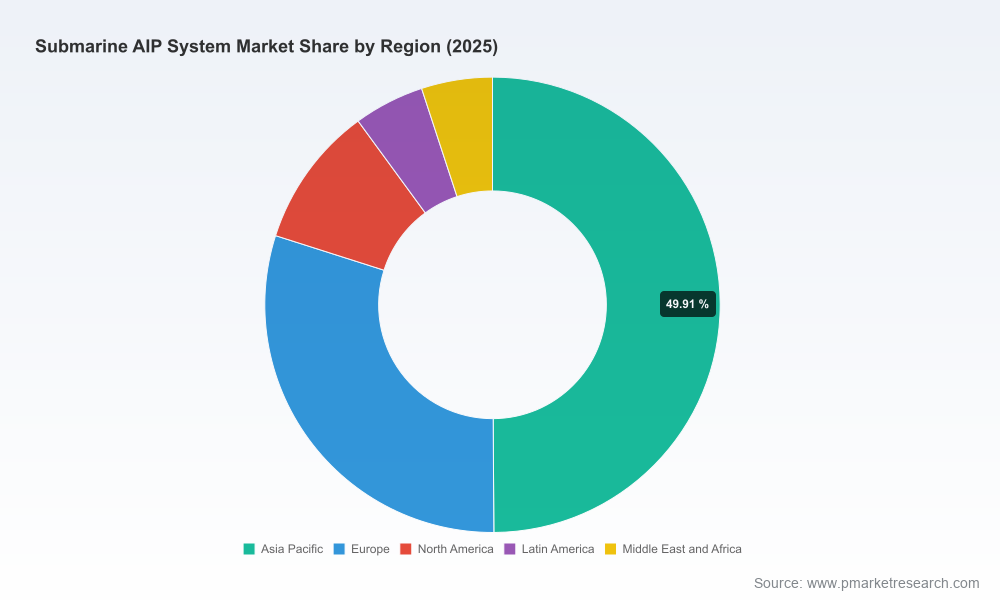

Submarine Aip System Market

Key macro metrics (USD, revenue unit: Million): historical market sizing covers 2020–2025 and our forecast horizon extends through 2026–2032. Highlights from the market trajectory include:

Submarine Aip System Market

- 2020 market size: 312.45 (USD Million)

- 2025 market size (base year): 392.21 (USD Million)

- 2026 forecast: 395.08 (USD Million)

- 2032 forecast: 509.21 (USD Million)

- Compound annual growth rate (forecast 2026–2032): 3.8%

These figures reflect the combined value of AIP hardware, integration and systems-of-systems work, lifecycle sustainment contracts, and selected retrofit programs captured in our model. The growth is steady rather than exponential — indicating a market driven by sovereign procurement cycles, incremental capability upgrades, and selective export demand rather than broad-based commercial adoption.

Submarine Aip System Market

Why this matters for 2026 decision-makers

For defense planners, prime contractors, Tier-1 suppliers, and strategic investors assessing priorities in 2026, the report provides a decision-grade synthesis of commercial signals and operational levers. Our research shows three immediate strategic implications:

- Procurement timing and platform selection: Governments planning new-build or mid-life upgrade programs must weigh the marginal endurance benefit against integration complexity and sustainment burden. The market’s steady growth profile means there is a window to optimize specifications and supplier selection without being forced into hasty platform choices.

- Technology-path hedging: Fuel cells, Stirling-cycle solutions, diesel-reforming approaches and hybrid combinations each present distinct risk-reward profiles. Investors and primes need modular planning that preserves upgrade pathways for future fuel-cell iterations while managing near-term operational readiness.

- Supply chain resilience and cost control: Raw-material constraints and geopolitically driven supply interruptions (notably in specialty metals) are already shaping production lead times and capex assumptions. Buyers who embed supply-chain risk mitigation in procurement contracts materially reduce schedule and budget risk.

What the full report delivers — practical content for executable choices

Our intent with the report is explicitly operational: we translate market sizing and scenario analysis into procurement-ready guidance and commercial playbooks. Key deliverables include:

- Detailed market model and forecasts (2020–2032) with sensitivity testing across price, adoption rate and regulatory scenarios.

- Decision matrices for new-build versus retrofit investments, including integration complexity scoring, expected time-to-operational capability, and sustainment cost vectors.

- Technology roadmaps for AIP variants (fuel-cells, Stirling engines, MESMA-style systems, hybrid architectures) that align R&D milestones with procurement cycles.

- Supplier profiles and capability heatmaps for headline OEMs and strategic suppliers, with practical vendor selection criteria for Ministries of Defence and system integrators.

- Supply-chain risk register covering critical raw materials, hydrogen storage and cryogenics, and specialty manufacturing bottlenecks — with mitigations and dual-sourcing playbooks.

- Regulatory and export-control impact assessments tied to realistic program timelines.

- M&A and partnership opportunity scans identifying targets by capability gap, integration readiness, and cost-to-scale metrics.

- Template procurement language and KPIs suitable for acquisition teams seeking to embed performance and obsolescence protection clauses in AIP contracts.

Competitive landscape: focus on capability, integration, and export-readiness

The Submarine AIP market is characterized by a constrained supplier ecosystem where a small set of engineering-intensive firms set technology roadmaps and capture the majority of program value. Our qualitative concentration assessment shows a market where top-tier integrators and technology originators collectively control a dominant share; this creates a competitive environment where partnership strategy, proprietary technology, and aftercare services determine win rates more than price alone.

Selected company profiles and strategic positioning (high-level):

- Saab AB (Kockums) (Sweden) — Renowned for Stirling-cycle AIP implementations in Gotland-class and A26 designs. Saab’s strength rests in acoustic stealth and a mature integration pedigree; its platform-centric approach appeals to customers prioritizing quiet endurance and minimal operational disruption.

- thyssenkrupp Marine Systems (TKMS) (Germany) — Focused on PEM fuel-cell solutions through strategic technical partnerships. TKMS’s integration of fuel cells into Type 212/214 families and export variants underscores its ability to pair propulsion innovation with proven hull architectures.

- Siemens AG (Germany) — A primary provider of PEM fuel-cell modules and associated power electronics. Siemens competes on module maturity and systems engineering, positioning itself as a technology supplier to naval shipyards and integrators.

- Naval Group (France) — Developer of MESMA and second-generation fuel-cell concepts, including onboard hydrogen generation through diesel reforming. Naval Group’s R&D emphasis is integration of energy-generation options to reduce onboard logistics burden.

- Hanwha Ocean (South Korea) — Emerging as a competitive exporter, Hanwha integrates hybrid AIP approaches (notably fuel-cell hybrids) into KSS-III and export platforms. Recent design approvals and launches have elevated Hanwha’s export-readiness profile.

- Navantia (Spain) — Pursuing bioethanol-based AIP processing for the S-80 program and collaborative export initiatives. Navantia’s differentiator is alternative-fuel approaches reducing dependence on specialized hydrogen logistics.

- China Shipbuilding Industry Corporation (CSIC) (China) — Deploys indigenous AIP technologies across domestic submarine classes; scale advantages and integrated shipbuilding capabilities present different strategic dynamics for regional procurement markets.

Recent program-level developments underscore the market’s practical momentum and the tactical choices facing buyers:

- Integration milestones in 2026 showing indigenous fuel-cell efforts moving from lab to hull for naval operators seeking strategic autonomy.

- Export design approvals and launches in 2025–2026 reflecting rising demand from navies seeking modern AIP capability without full fuel-cell industrial ecosystems.

- Additional sovereign orders for PEM fuel-cell-equipped designs indicating selective acceleration among early adopters.

Supply-chain realities and geopolitical friction

Procurement decisions in 2026 must be contextualized against two structural headwinds: raw material risk and regulatory/geopolitical fragmentation. Western sanctions and export controls have disrupted supplies of specialty metals used in pressure hull components, high-performance batteries and some AIP subsystems. At the same time, technical complexity and cost of hydrogen storage (including metal hydride systems and liquid-oxygen support systems) materially influence both unit production costs and program schedules.

Our report models the capex and opex impact of three distinct supply-chain shock scenarios and provides concrete mitigation strategies: localised supplier qualification plans, modular subsystem procurement to reduce single-vendor lock-in, and contract structures that share commodity-price risk between buyers and prime contractors.

Using the report as a 2026 playbook

Leaders who will most benefit from this work include: defense acquisition authorities setting AIP requirements; prime contractors balancing platform sales and systems integration; component suppliers positioning for qualification; and private-equity or strategic investors assessing consolidation opportunities.

Practical uses for the report in 2026:

- Benchmarking procurement timelines and cost envelopes against comparable programs and sensitivity-tested forecasts.

- Developing RFPs that explicitly trade off endurance, acoustic signature and sustainment cost over multi-decade life cycles.

- Designing supply agreements and JV structures to de-risk access to critical materials and hydrogen-handling expertise.

- Prioritising R&D spend on the most operationally leverageable technologies (e.g., next-generation PEM stacks, compact cryogenics, and hybrid power-management systems).

Trailer and next steps — where to access the full intelligence

This brief deliberately emphasizes strategic direction and actionable implications while withholding the complete granular segment breakdowns and proprietary model outputs that make direct program-level decisions defensible. The full report contains the exhaustive segment-level forecasts, supplier share estimates, procurement KPIs, and downloadable model files that procurement teams, C-suite decision-makers and program offices will require to execute with confidence.

PW Consulting’s Submarine AIP System Market report is designed as a decision-support product for 2026 procurement windows and beyond: a single, defensible source that aligns technical, commercial and geopolitical analysis into acquisition-grade recommendations. To obtain the full dataset, segment tabulations, and model access, please request the report through PW Consulting’s research portal or contact our industry desk for an executive briefing and licensing options.

Data notes: base year = 2025; historical years included 2020–2025; forecast period 2026–2032; currency USD, revenue unit = Million; CAGR (2026–2032) = 3.8%.

For detailed analysis of this topic, please visit the official page:Submarine Aip System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com