Closed Caption Services Market 2026: Strategic Preview for Decision Makers

As PW Consulting’s Senior Strategic Advisor and Chief Industry Analyst, I present a concise, forward-looking briefing on our latest Closed Caption Services Market study (base year 2025; historical window 2020–2025; forecast 2026–2032). This executive preview emphasizes the report’s strategic value for enterprise leaders planning investments, procurement, and compliance actions in 2026. It highlights macro trajectories, competitive dynamics, regulatory inflection points, and the practical frameworks we provide — while deliberately withholding core segment-level datapoints to preserve the full strategic value of the proprietary dataset available through our report portal.

Closed Caption Services Market

Market trajectory in one line

The global closed caption services market expands steadily: from an assessed market size of approximately USD 550.0 million in 2025, the market is projected to approach close to USD 955.0 million by 2032, reflecting a compound annual growth rate (CAGR) of about 8.2% over the 2026–2032 forecast period.

Closed Caption Services Market

Why this matters to corporate decision makers in 2026

- Regulatory timing creates immediate programmatic deadlines. With regulatory compliance windows maturing in 2026 — notably a major administrative compliance milestone scheduled for August 17, 2026 addressing display accessibility and discoverability — organizations must prioritize captioning readiness across device and content delivery ecosystems now. Delay risks both fines and service disruptions for customer-facing content.

- Growth with constraints. The market’s mid-single-digit to high-single-digit CAGR signals robust demand and new business models (AI-driven automation, hybrid services, live captioning) — but growth coexists with operational cost pressures such as rising cloud and data-center energy costs that can materially change unit economics for captioning services.

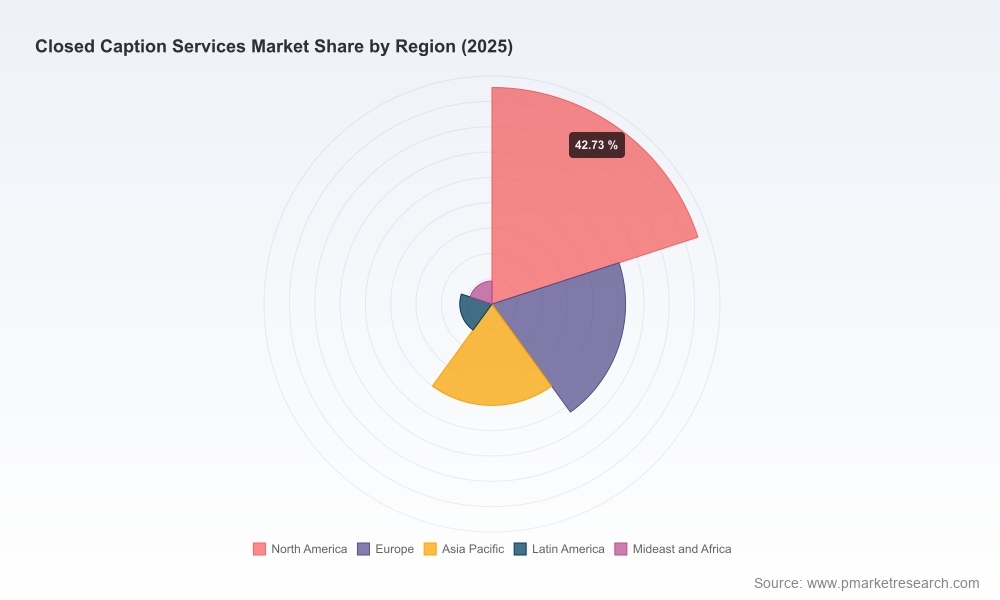

- Fragmentation equals strategic opportunity. Market concentration is low (CR3 approximately 18.5%; CR5 approximately 24.8%), indicating room for entrants, niche specialists, and roll-up strategies. Buyers can leverage this fragmentation to negotiate pricing, secure specialized quality, and construct multi-vendor sourcing strategies that balance cost, compliance, and live-capability risk.

Key industry dynamics shaping 2026 decisions

- Regulatory inflection points: The FCC and other regulators remain active. Recent rulings and notices have tightened display and accessibility expectations, and additional regulatory reviews on automated captioning services are underway. Organizations must track both national mandates and jurisdictional divergence following legal rulings that shift regulatory authority toward states and legislatures.

- Tech evolution — automation vs. human augmentation: Enterprises face trade-offs between cost, speed, and accuracy. Automated solutions drive scale and lower per-minute costs, while human-mediated services maintain higher accuracy and legal defensibility in sensitive applications (broadcast, court reporting, high-stakes public sector content). The optimal operating model for most organizations will be hybrid: automated pre-processing plus human QA for defined content classes.

- Live captioning remains strategically valuable but operationally intensive: Demand for live, high-accuracy captioning across news, sports, event streaming, and hybrid workplaces is growing. Live services require human-in-the-loop workflows and robust low-latency infrastructure — making them a premium offering and a margin lever for specialist providers.

- Cost pressure from infrastructure: Skyrocketing data-center energy demand and associated electric costs are altering cloud economics for continuous media processing workloads. Buyers should incorporate energy-driven TCO scenarios into vendor comparisons and consider architectural strategies such as edge processing, scheduled batch workflows, and multi-cloud arbitration to stabilize costs.

- Talent pipeline constraints: Labour-market indicators show modest absolute openings for court reporters and simultaneous captioners, suggesting that scaling pure human-heavy models at pace will be constrained without investment in training and retention programs.

What the PW Consulting report delivers (practical, action-oriented)

- Integrated market model: A transparent forecasting engine covering 2026–2032 with scenario toggles for regulation impact, energy cost escalations, and automation adoption curves.

- Vendor scorecard and procurement playbook: Comparative matrices that evaluate providers across accuracy, live capability, compliance coverage, SLAs, scalability, and commercial models — plus negotiation levers and contract clauses to mitigate supply risk.

- Use-case TCO and pricing benchmarks: Role-based TCO templates (broadcast operations, enterprise learning, event services, public sector) that combine capex/opex, QA, latency, and accessibility risk premiums.

- Technology landscape assessment: Detailed evaluation of automated captioning engines, hybrid workflows, quality assurance tooling, and integration patterns for streaming and VOD platforms — with recommended architecture patterns for high-availability live captioning and offline batch processing.

- Regulatory readiness checklist: Practical steps for achieving 'readily accessible' display settings and discoverability across devices and MVPDs, and a compliance-runway planner for August 2026 deadlines and beyond.

- M&A and partnership playbook: Valuation heuristics for roll-ups in a fragmented market, target screening criteria, and integration templates to capture synergies in live-capability, language coverage, and enterprise accounts.

- Risk register and mitigation strategies: Scenarios for congestion/cost shocks, supply-chain concentration, and litigation exposure — with prioritized mitigation actions and monitoring KPIs.

Competitive landscape — what buyers and investors need to know

The ecosystem combines specialized human-first providers, platform-led automated vendors, nonprofit service organizations, and regionally focused real-time captioning pioneers. This variety enables tailored sourcing — from high-accuracy broadcast captioning to scalable automated captioning for massive archive processing. Core players exemplify distinct strategic positions:

Closed Caption Services Market

- Human-first premium providers: Some companies continue to own reputation assets built on high-accuracy, human-mediated workflows and SLA-backed services for broadcasters and enterprise customers. Their value proposition centers on legal defensibility, accessibility consulting, and premium live capability.

- Automated and hybrid innovators: Several vendors combine AI-driven engines with human QA overlays, enabling lower marginal costs while maintaining acceptable accuracy for many commercial applications. These firms are racing to improve domain adaptation, speaker diarization, and multi-language support.

- Nonprofit and public-interest entities: Organizations in this cohort prioritize broad accessibility and coverage across public media, often with deep domain expertise in compliance and longstanding relationships with regulatory bodies.

- Regional and legacy live-caption specialists: Established regional providers remain critical partners for local news, court reporting, and event services where latency and human verification are non-negotiable.

We profile a representative sample of market participants within the report, evaluating each on capability, scale, vertical focus, and strategic intent. For example, profiles include providers known for high-accuracy human captioning and compliance depth, AI-led firms with strong live and translation integrations, longstanding live-news specialists with deep operational playbooks, and nonprofit captioning institutes focused on public service accessibility.

Strategic recommendations for 2026 action plans

- Immediate compliance and discovery program: Launch a cross-functional accessibility sprint to align product/device UX with regulatory ‘readily accessible’ standards; prioritize the most visible consumer touchpoints and MVPD integrations. Use a two-track remediation: quick UX fixes for immediate compliance and a systemic architecture plan for long-term discoverability and persistence of caption settings.

- Adopt hybrid sourcing now: Implement a mixed-vendor strategy that leverages automated processing for bulk VOD and human QA for broadcast and legally sensitive content. Contractually reserve live capacity with specialist vendors and layer in automation where latency tolerances allow.

- Embed energy-aware TCO into procurement: Update vendor scorecards to include projected cloud/dc energy exposure and unit energy cost assumptions. Negotiate pricing clauses tied to supplier energy cost indices or consider workload-resilience strategies (batching, off-peak processing, edge pre-processing).

- Invest in workforce resilience and upskilling: Build internal captioning competency where it creates competitive advantage (e.g., training programs for real-time captioners, QA teams, and automation trainers) and partner with vendors on shared labor pipelines.

- Explore M&A selectively: Given market fragmentation and modest concentration, pursue tuck-in purchases to secure live-captioning capability, language coverage, or enterprise accounts — prioritizing accretive targets with strong operational playbooks.

Risk outlook and KPIs to monitor

- Regulatory drift: Monitor federal and state-level rulemaking that could broaden or narrow obligations; track pending administrative filings concerning automated captioning services.

- Cost volatility: Watch energy indices and cloud provider pass-throughs; include energy cost sensitivity in quarterly planning.

- Quality delta: Track accuracy metrics (word error rate, speaker attribution accuracy) across automated engines and human QA; define acceptable thresholds by content class.

- Capacity and labor availability: Monitor hiring pipelines and partner capacity for live captioning to avoid service disruptions during peak event periods.

Closing note — how to use the full PW Consulting report

This preview is curated to give leaders a strategic window into the dynamics that should shape 2026 decisions: compliance calendars, hybrid sourcing imperatives, cost-structure shifts, and the tactical levers that buyers and investors can pull. The full PW Consulting report contains the complete dataset, segmented forecasts, vendor scorecards, contract templates, and downloadable TCO models — essential tools for operationalizing the recommendations above. To access the proprietary segmentation, regional and vertical breakouts, and vendor-by-metric tables needed for purchase approvals and board-level planning, please consult the report landing page.

For leaders who need a tailored briefing (procurement-ready vendor shortlists, a compliance remediation roadmap, or an M&A target-screen), PW Consulting offers rapid advisory packages that leverage the dataset and modelling in this report to create executable 90-day plans.

For detailed analysis of this topic, please visit the official page:Closed Caption Services Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com