Digital Ureteroscopes Market — Strategic Outlook 2026: What Healthcare Leaders Need to Know

PW Consulting presents an executive briefing drawn from our latest market research report on the Digital Ureteroscopes market. This briefing is designed to help executives, strategy teams, investors, and procurement leaders rapidly assess the commercial imperatives shaping 2026 decisions. It synthesizes our proprietary market-sizing, trend analysis, competitive mapping, regulatory context, and scenario-driven recommendations — while preserving the granular, segment-level datasets and models for clients who access the full report.

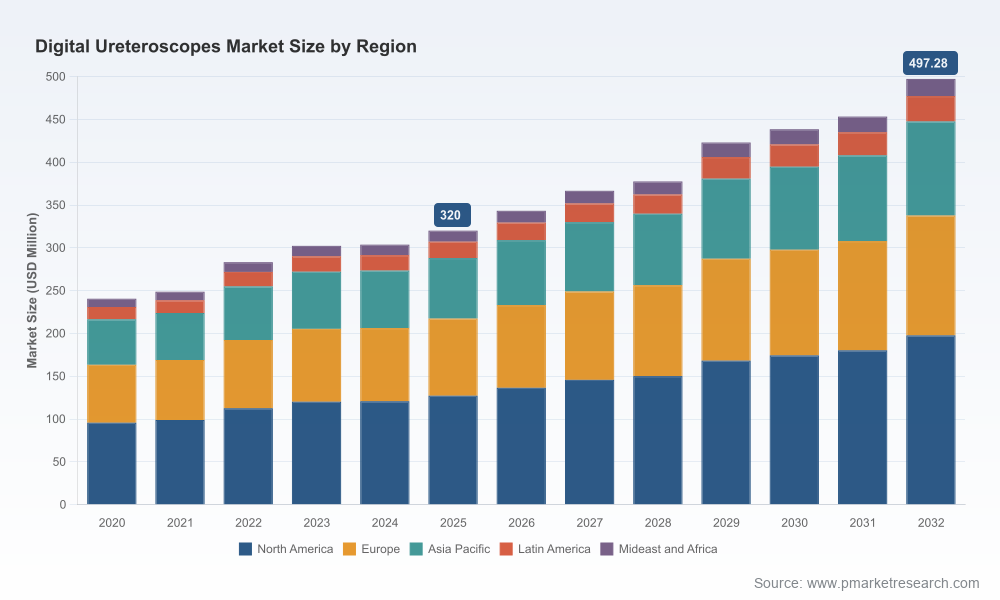

Digital Ureteroscopes Market

Executive Summary

The Digital Ureteroscopes market is in a steady growth phase driven by technology substitution, procedural volume growth in endourology, and shifting purchasing economics between reusable and single‑use platforms. Our model (base year 2025, historical range 2020–2025, forecast period 2026–2032) quantifies current scale and the trajectory underpinning near‑term investment choices. On a headline basis, the market reached a robust level in 2025 and is projected to expand through the forecast window at a compound annual growth rate (CAGR) of 6.5%. By 2026 our top‑line projection reflects continued expansion, and by 2032 the total market approaches a materially larger opportunity relative to 2025.

Digital Ureteroscopes Market

Market structure remains concentrated: the top three vendors control a substantial portion of revenue (CR3 ~65%), and the top five firms account for an even higher share (CR5 ~85%). This concentration, together with fast-rising single‑use adoption, creates differentiated prospects for new entrants, component suppliers, and strategic buyers.

Digital Ureteroscopes Market

Why this matters for 2026 decision cycles

- Capital allocation and R&D prioritization: Organizations must reconcile investment in imaging, miniaturization, and disposable platforms against cost pressures and reimbursement dynamics. Our report models where R&D yields the fastest commercial payback under multiple adoption scenarios.

- Go‑to‑market timing: Product launches and regulatory clearances (notably in 2024–2025) have altered competitive positioning. An action window exists in 2026 for products offering clear clinical differentiation (improved visualization, intrarenal pressure monitoring, slimmer distal tips) to capture share before market consolidation accelerates.

- M&A and partnership strategy: High concentration levels make bolt‑on acquisitions or JV structures attractive ways for mid‑tier firms to supplement channel reach or fill portfolio gaps without competing head‑on with CR3 players.

- Provider procurement and ASC strategies: Hospitals and ambulatory surgery centers must refine procurement policies to balance unit cost, reprocessing overhead, and infection control imperatives — decisions that will materially affect supplier selection in 2026.

Market dynamics and drivers

Key dynamics shaping the market include:

- Technology substitution: Continued migration from fiberoptic to high‑resolution digital imaging (CMOS and related technologies) is improving diagnostics and therapeutic accuracy, which supports premium positioning for products that demonstrably reduce procedure time or improve outcomes.

- Single‑use vs. reusable economics: Single‑use digital flexible ureteroscopes mitigate cross‑contamination risks and eliminate reprocessing and repair costs. Our cost models compare lifecycle economics across typical hospital and ASC usage profiles and demonstrate the inflection points where single‑use becomes preferable from a total cost of ownership perspective.

- Regulatory and reimbursement environment: Digital flexible ureteroscopes are classified as Class II devices under relevant US regulations and typically subject to 510(k) clearance. Established procedure coding and payment structures support both device types, but subtle changes in reimbursement and hospital procurement rules can alter relative value propositions.

- Clinical drivers: Rising incidence of urolithiasis and expanding indications for ureteroscopic intervention are underpinning volume growth. Device features such as intrarenal pressure monitoring and enhanced deflection are increasingly cited by clinicians as determinants of clinical preference.

Competitive landscape — what the leading firms are doing

The market is currently shaped by a mix of large incumbent medtech groups and specialized innovators. Companies at the forefront include well‑known global device manufacturers and several focused single‑use specialists. Recently observed moves illustrate how vendors are staking claims along the technology and channel dimensions:

- Boston Scientific Corporation — Expanded configurations of single‑use digital platforms with regulatory clearances and features such as real‑time intrarenal pressure monitoring. These capabilities speak directly to safety and efficiency narratives favored by hospital procurement teams.

- KARL STORZ — Continues to reinforce reusable high‑resolution digital platforms with its Flex‑XC lineup, emphasizing imaging quality for centers that prioritize durable capital equipment.

- Olympus — Focused on durable flexible video ureteroscopes with an emphasis on image quality and device longevity, appealing to high‑volume centers seeking low per‑case cost via reusables.

- Dornier MedTech — Aggressively pursuing the single‑use segment with new slim models and accessory systems, including recent commercial launches in the Americas.

- Ambu — Committed to single‑use strategies with products cleared for market and integrated imaging systems aimed at simplifying OR workflows.

- OTU Medical, Richard Wolf, Stryker — Each balances reusable and single‑use approaches, with OTU and Richard Wolf emphasizing visualization advances and Stryker leveraging broad endoscopy portfolios to cross‑sell into urology.

Notably, 2024–2025 featured several regulatory clearances and product launches that have shifted tactical positioning (for example, multiple 510(k) clearances and new single‑use introductions). These events are covered in our timeline and competitive battlecards within the full report.

What the PW Consulting report contains (practical, actionable elements)

Our full report is structured to support real decisions in 2026 and beyond. Key deliverables include:

- Market sizing and bottom‑up revenue models (base year 2025; historical 2020–2025; forecast 2026–2032, CAGR 6.5%) with scenario sensitivity to price, volume, and replacement cycles.

- Segment economics and adoption curves distinguishing reusable vs. single‑use strategies, device classes, and procedure types (detailed segment splits are available in the client portal).

- Competitor profiles and strategic capability maps, including product roadmaps, manufacturing footprints, and IP posture.

- Regulatory and reimbursement playbook: pathway maps, typical 510(k) considerations, CPT code impacts, and payer levers that affect adoption in hospital vs. ASC settings.

- Buyer‑side playbook for hospitals and ASCs: procurement scorecards, cost‑of‑ownership calculators, and recommended trial frameworks for assessing single‑use pilots.

- M&A valuation frameworks and a short‑list of targets for strategic buyers, plus integrated due diligence checklists.

- Scenario planning and stress tests: how pricing pressure, accelerated single‑use uptake, or a step‑change in reimbursement would alter 2026 revenue plans.

- Primary research appendices: KOL interviews, end‑user survey analytics, and surgeon preference matrices.

To preserve the value of our proprietary segmentation and price curve models, the full dataset and the granular regional/application revenue splits are provided exclusively in the full report package.

Strategic recommendations for 2026

Our recommendations are organized for four primary audiences: manufacturers, investors, provider procurement teams, and distributors/partners.

- For manufacturers:

- Prioritize features that reduce procedure time and demonstrably lower complication or reprocessing costs (e.g., intrarenal pressure monitoring, slimmer distal tips, robust CMOS imaging).

- Build modular platform strategies to serve both single‑use and reusable preferences; flexibility reduces channel risk as provider preferences diverge.

- Invest selectively in regulatory and clinical evidence generation — 510(k) clearances remain necessary but not sufficient; robust real‑world evidence wins formulary positions.

- For investors and private equity:

- Target mid‑market players with differentiated disposable technologies or service contracts; consolidation opportunities remain given high market concentration among top players.

- Use our scenario models to stress test investment returns under accelerated single‑use adoption and varying price erosion assumptions.

- For hospitals and ASCs:

- Run controlled single‑use pilots with rigorous cost‑of‑care tracking (OR time, reprocessing, repair, infection outcomes) before committing to broad fleet changes.

- Negotiate bundled pricing and shared‑risk agreements where possible; vendors are increasingly open to outcome‑linked contracts to drive adoption.

- For distributors and channel partners:

- Expand value‑added services around training, consumables, and digital integration to maintain margins as device unit economics shift.

- Position as clinical and economic advisors — partners who can run TCO analyses for providers will be preferred by vendors and purchasers alike.

How PW Consulting can help

PW Consulting’s Digital Ureteroscopes report combines quantitative forecasting with actionable strategy tools. Clients receive the underlying model (modifiable for custom scenarios), competitor battlecards, reimbursement playbooks, and a practical procurement toolkit. For teams making 2026 capital, product, or acquisition decisions, our work reduces uncertainty by translating clinical trends and regulatory noise into investment‑grade insights.

Note: This briefing highlights high‑level findings and themes. The full report contains the proprietary, segment‑level revenue schedules, regional and application splits, and downloadable models referenced above. Contact PW Consulting to access the complete dataset, executive workshop options, and tailored scenario analyses to support your 2026 strategy.

For detailed analysis of this topic, please visit the official page:Digital Ureteroscopes Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com