Aspirin Market: Insights, Key Players, and Growth Analysis

Networking |

2026-06-16 03:37:26

PW Consulting today releases a focused industry brief accompanying our full market research report on the Cosmetic Grade Sorbitan Esters market. Built from a structured analysis spanning 2020–2025 (base year 2025) and a forward-looking forecast period through 2032, this briefing distils the high-impact strategic implications that senior executives, procurement leaders, and R&D heads must internalize when setting priorities for 2026.

Cosmetic Grade Sorbitan Esters Market

Sorbitan esters are foundational emulsifiers and co-emulsifiers in personal care formulations, with usage stretching across skin care, hair care, decorative cosmetics and toiletries. The market has recorded steady expansion from the early 2020s, moving from roughly USD 388 million in 2020 to about USD 505 million in 2025. Our model projects continued expansion through the forecast horizon, with the market advancing toward approximately USD 732 million by 2032 driven by a compound annual growth rate (CAGR) of 5.45% over 2026–2032.

Cosmetic Grade Sorbitan Esters Market

For corporate strategists, these headline dynamics translate into three immediate imperatives for 2026:

Cosmetic Grade Sorbitan Esters Market

At the macro level, market growth is being fueled by: sustained demand in advanced personal care segments, product innovation that leverages sensory and stability benefits of sorbitan esters, and formulators’ appetite for multifunctional ingredients that support cleaner-label and wellness positioning. These drivers are balanced by structural constraints—raw-material volatility, regulatory scrutiny in adjacent categories, and incremental price sensitivity in mature geographies.

Feedstock dynamics are a decisive near-term force. Sorbitol, the upstream carbohydrate feedstock for sorbitan esters, experienced marked pricing dispersion across sourcing geographies in early 2026 and notable price correction in late 2025. This creates a two-speed cost environment for manufacturers and private-label formulators: those who can access advantaged feedstock or who operate integrated upstream positions will enjoy meaningful margin flexibility; those without such levers will face a squeeze unless they pass costs through or optimize formulations.

Regulatory and safety narratives are also influential. A June 2025 EFSA opinion re-affirmed the established safety profile of sorbitan monostearate in contexts relevant to personal care, while U.S. agency work on PFAS in cosmetics (reported in late 2025) has not implicated sorbitan esters. These developments reduce short-term regulatory tail risks for cosmetic-grade sorbitan esters, but they amplify the premium on traceability, documentation and supplier governance as brands differentiate on safety & transparency.

The market exhibits moderate concentration: the three largest suppliers together account for a meaningful share of volume, and the top five add further clustering—creating buying-power asymmetries and supply-side choices that matter for 2026 contracting strategies. Our qualitative review of headline suppliers identifies a mixed ecosystem of global specialty-chemicals leaders, regional specialists and local commodity producers.

For 2026 procurement leaders, supplier selection must be multi-dimensional: price is necessary but insufficient. Evaluate partners on regulatory documentation, capacity flexibility, geographical redundancy, and co-development capability. In many cases, hybrid strategies—combining partnership with global majors for core SKUs and regional suppliers for spot coverage—offer the best risk-adjusted outcome.

Formulation teams face simultaneous pressures to improve sensory profiles, extend shelf stability, and align to sustainability narratives. Sorbitan esters are attractive because they can simultaneously deliver W/O emulsification, stabilize complex actives, and support clean-label claims when paired with natural feedstocks.

Raw-material volatility is not a short-term curiosity. In January 2026, sorbitol FOB price points demonstrated material geographic variance; and in Q4 2025, North America witnessed a double-digit quarter-over-quarter decline in sorbitol pricing indices. The practical implications for 2026 procurement strategies include:

Recent regulatory commentary has, to date, left sorbitan esters in a relatively secure position. EFSA’s re-evaluation of sorbitan monostearate sustained its safety profile for related applications, and U.S. PFAS screenings in late 2025 did not implicate these esters. Nevertheless, teams should not interpret this as a mandate for complacency. Instead, treat regulatory stability as a platform to harden governance:

Our full report moves beyond headline growth to provide operationally-relevant tools and playbooks. Highlights include:

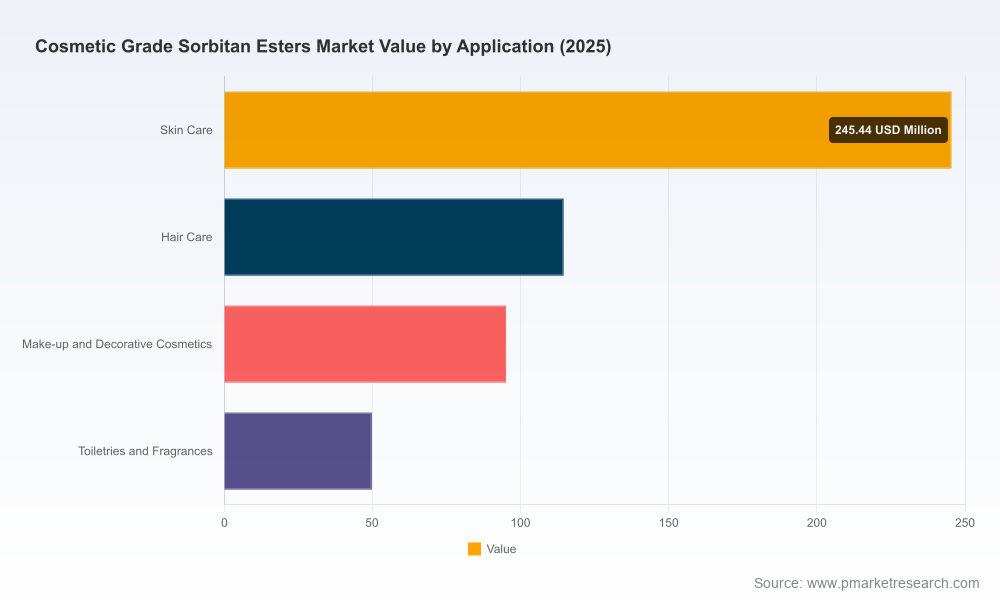

To preserve strategic value for paying clients while still enabling informed decision-making, the briefing intentionally omits granular regional and application-level splits. The full dataset, including detailed segment forecasts, growth pockets by application and regional demand trajectories, is available through PW Consulting’s report portal.

Leaders should treat the coming 12–18 months as a window to execute three tangible actions:

PW Consulting’s Cosmetic Grade Sorbitan Esters market research synthesizes historical performance, a forward-looking 2026–2032 forecast (5.45% CAGR, base year 2025), supplier landscape analysis, and actionable operational playbooks. The analysis is purposely layered: this public briefing communicates the high-conviction implications you need to act in 2026 while preserving the full, segment-level evidence base for report subscribers.

For procurement RFPs, M&A diligence, formulation roadmaps, and regulatory preparedness, the full report provides the granular segmentation, supplier-level benchmarks, and downloadable tools your teams will use in execution. Contact PW Consulting or visit our report page to access the complete dataset and client-only advisory services.

For detailed analysis of this topic, please visit the official page:Cosmetic Grade Sorbitan Esters Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com