Advanced Optical Testing Technologies Strengthen Silicon Photonic Test System Market Outlook

Food |

2026-06-10 06:30:53

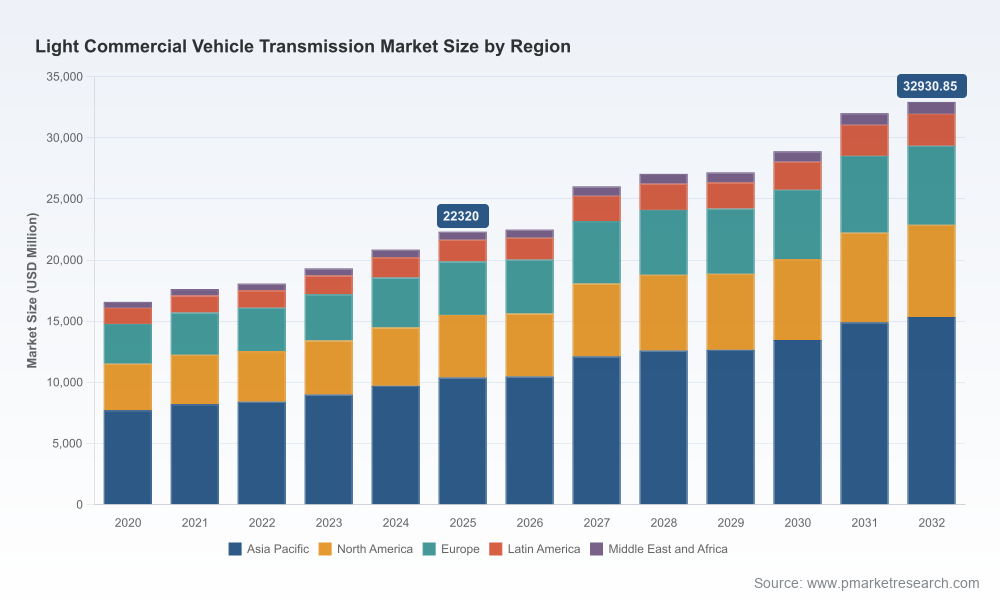

As global logistics patterns and regulatory regimes converge on efficiency and electrification, the Light Commercial Vehicle (LCV) transmission market has transitioned from steady growth to strategic inflection. Our new PW Consulting market study — anchored on a 2025 base year and a forecast horizon through 2032 — shows the industry expanding at a compound annual growth rate (CAGR) of approximately 5.71% over the forecast window. The market grew from about USD 16,580 Million in 2020 to USD 22,320 Million in 2025 and is projected to reach roughly USD 32,931 Million by 2032.

Light Commercial Vehicle Transmission Market

These headline figures capture the macro momentum: sustained demand driven by last‑mile logistics, regulatory-driven fuel‑efficiency upgrades, and an accelerating shift toward hybrid and electrified drivetrains. But beneath the topline lie structurally different pathways for incumbent transmission suppliers, OEMs, and new entrants — pathways that will determine winners and followers across the next investment cycle.

Light Commercial Vehicle Transmission Market

Decision timing: With 2026 budgets and product roadmaps being finalized, companies need precise, actionable scenarios that translate macro trends into program-level implications (sourcing, validation timelines, pricing and warranty reserves).

Light Commercial Vehicle Transmission Market

Regulatory acceleration: Stricter emissions and fuel economy rules in major markets are forcing earlier adoption of multi‑speed and electrified transmissions in LCV platforms — decisions that have multi‑year development and capital timelines.

Supply-chain disruption & protectionism: New trade measures and tariff schedules since late 2025 materially change landed costs for imported transmission assemblies, prompting re-evaluation of nearshoring, dual-sourcing and supplier footprint strategies.

Technology convergence: Hybrid modules, compact dual‑clutch units and integrated e-transmission architectures require different supplier capabilities and IP ownership strategies compared with legacy mechanical gearbox programs.

Market structure: Concentration metrics indicate a moderately consolidated market (CR3 ~38.5%; CR5 ~52.7%), meaning moves by Tier‑1 leaders have outsized effects on technology roadmaps and price benchmarks.

The PW Consulting study is designed as an operational toolset for commercial and technical leaders. Key deliverables include:

Forecast engine and scenario models: Interactive, downloadable files that run alternate demand, price and regulation scenarios for 2026–2032 so you can stress-test program economics.

Supply‑chain risk matrix: Granular supplier mapping, lead‑time sensitivities, tariff exposure analysis and recommendation tiers for nearshoring, dual-sourcing and inventory hedging.

Technology readiness framework: Comparative assessment of automatic, manual, automated‑manual, DCT and electrified transmission variants against cost, weight, NVH and integration complexity for LCV use cases.

Commercial playbooks: Go‑to‑market templates for OEMs and Tier‑1s including pricing strategies, warranty design, aftermarket and reman programs, and fleet‑operator value propositions.

M&A and partnership scorecards: Target screening templates with capability gaps, valuation ranges and integration risk checklists focused on e‑transmission modules and software‑defined powertrain firms.

Regulatory impact maps and compliance timelines: Market-by-market regulatory milestones and the program-level implications for homologation and certification.

Raw‑material sensitivity tools: Steel and aluminum price pass‑through models with break‑even and margin scenarios for suppliers and OEMs.

Vendor benchmarking and RFP templates: Operational KPIs, test protocols and scoring rubrics to accelerate supplier selection under compressed procurement cycles.

To preserve commercial discretion in this announcement we are not publishing the full segmentation tables or vendor-level market shares in-line; the report includes those granular datasets and the forecast workbook for clients and authorized licensees.

The LCV transmission arena is being reshaped by incumbents extending their product scopes and specialist firms seizing electrification opportunities. Highlights from our competitive mapping and the latest industry developments:

ZF Friedrichshafen AG (Germany) — continues to push multi‑speed automatic architectures into medium and heavier LCV platforms with recent launches targeted at improved packaging and fuel efficiency. ZF’s March 2026 introduction of an 8‑speed PowerLine transmission onto a medium‑duty OEM platform signals intensified competition in integrated powertrain offerings.

Aisin Corporation (Japan) — remains focused on compact, robust automatic units and hybrid‑compatible modules. Aisin’s announcements around compact dual‑clutch EV transmissions reflect a play to capture light-truck electrification programs where packaging and thermal management are critical.

Allison Transmission (USA) — leverages long-standing strength in automatic transmissions for delivery and utility fleets; its product positioning emphasizes durability and low‑downtime service footprints for fleet operators prioritizing uptime.

Eaton Corporation (Ireland) — is advancing automated manual and dual‑clutch systems for light‑duty segments, exemplified by its 2025 Advantor‑6 introduction for buses and trucks; Eaton’s modular control strategies are a differentiator for mixed‑fleet customers transitioning to electrified hybrids.

BorgWarner, Dana, Magna — each plays a strategic role in electrified powertrain modules and componentization. Their R&D and acquisition activity is targeted at e‑transmissions, motor‑integrated gearboxes and high‑voltage integration capabilities that reduce complexity for OEMs.

Smaller regional players and OEM captive programs continue to erode some aftermarket margins, but the shift to electrified and software‑defined transmissions creates new high‑margin service opportunities for capable suppliers.

Mar 2026 — ZF’s 8‑speed PowerLine deployment on a medium‑duty platform tightens competition in the mid‑segment and raises the integration bar for fuel‑efficiency claims.

Sep 2025 — Eaton introduced the Advantor‑6 automated manual transmission aimed at light trucks and buses, strengthening choices for fleet electrification pathways.

2025 — Aisin and other leaders announced compact DCT and EV transmission modules targeted at light‑truck electrification programs; suppliers that can offer turnkey motor+gearbox+software solutions are increasingly preferred by OEMs.

2025 — Regional OEMs initiated new production starts with automatic gearbox variants, underscoring the rapid productization cycle in last‑mile and urban delivery segments.

Raw‑material volatility (steel, aluminum) is pressuring component margins and testing supplier contractual terms — firms must model metal price elasticity into bid strategies and warranty reserves.

Regulatory tightening in the US, EU and China is accelerating adoption of advanced multi‑speed and electrified transmissions, shortening acceptable development lead times for OEMs and Tier‑1s.

Protectionist measures — notably tariffs enacted in late 2025 — increase landed costs for some imported transmission parts, making regional sourcing and local manufacturing more attractive for mitigating risk.

Growing fleet electrification and software‑defined powertrain requirements are shifting value from mechanical IP to control software and system integration capabilities.

Reassess sourcing footprints: run a rapid two‑week sourcing and landed‑cost assessment that includes tariff scenarios and alternative supplier qualification timelines.

Protect gross margins: institute metal‑price pass‑through clauses, short‑term hedges and dynamic pricing triggers for long‑term contracts to avoid margin erosion.

Accelerate electrified product roadmaps: prioritize modular e‑transmission demonstrators and software integration pilots to secure program slots with OEMs seeking turnkey powertrain suppliers.

Adopt scenario‑based capex: condition manufacturing investments on pre‑defined volume and contract milestones; use flexible automation to limit stranded capacity risk.

Pursue selective partnerships and bolt‑on acquisitions: target software, thermal management and motor‑integration capabilities to close capability gaps quickly.

Commercial readiness: implement aftermarket and reman strategies now to monetize serviceable life across hybrid and mild‑EV LCV fleets.

PW Consulting combines market analytics, engineering insight and transaction advisory to help clients convert the report’s findings into executable plans. We offer rapid diagnostic workshops, bespoke forecast model licensing, supplier due‑diligence support, regulatory compliance mapping and M&A diligence tailored to transmission and e‑powertrain targets.

This press release provides a strategic overview and tools menu; detailed segmentation tables, regional and application breakdowns, model‑level forecasts and vendor share data are reserved for the full report and client downloads. To access the full dataset, forecast workbooks and the vendor‑level analysis that underpin these recommendations, please visit the PW Consulting report page or contact our industry practice for an executive briefing.

— PW Consulting, Automotive & Mobility Practice

For detailed analysis of this topic, please visit the official page:Light Commercial Vehicle Transmission Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com