Departmental Picture Archiving and Communication System (PACS) Market: Size, Share, and Future Growth

Other |

2026-05-14 06:04:19

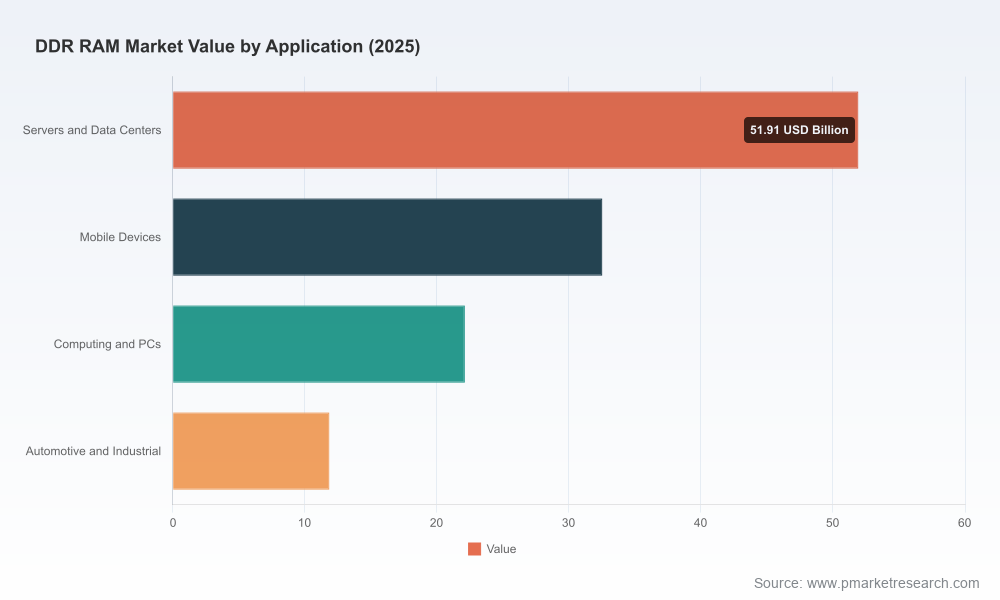

As global compute architectures accelerate toward AI‑first workloads and edge intelligence expands, memory markets have moved from steady commodity cycles into a period of strategic scarcity and rapid product transition. PW Consulting’s latest DDR RAM Market Research—anchored on a 2025 base year and a 2026–2032 forecast horizon—frames those shifts into an actionable decision toolkit for boards, procurement chiefs, product architects, and private equity teams preparing plans in 2026. The report models a market that is expanding from an estimated USD 118.4 billion in 2025 and is projected to grow at a compounded annual growth rate of 12.18% through the forecast window, with the total market size more than doubling by the end of the period.

Ddr Ram Market Research

Timing is now strategic: supply reallocation to high‑margin HBM and AI accelerators, combined with selective extensions of legacy DDR4 production, has created asymmetric availability and price volatility. This is a decisive environment for procurement and R&D scheduling.

Ddr Ram Market Research

Standards and performance ceilings have shifted. Recent JEDEC updates to DDR5 and new LPDDR specifications are changing qualification timelines for enterprise and mobile platforms; these updates materially affect module validation, system architecture, and product roadmaps.

Ddr Ram Market Research

Concentration matters. The supply base remains highly consolidated (high CR3/CR5 concentration), which amplifies pricing power, capacity allocation decisions, and the impact of single‑vendor production shifts on global supply chains.

The market’s near‑term profile is driven by three interacting forces. First, an AI‑led consumption wave is creating outsized demand for higher‑performance DRAM, prompting major manufacturers to redirect wafer starts toward HBM and other high‑margin products. Second, suppliers have selectively extended legacy DDR4 lines into late 2026 to balance server and client demand against production shifts—this has not been accompanied by major new capacity for standard DDR, creating a supply tightness. Third, price behavior in late 2025 and continuing into 2026 has been atypical for DRAM markets: contract and spot price escalations materially exceed historical cycles, and our pricing scenarios assume continued upward pressure through the first half of 2026 before stabilization under multiple demand/capacity outcomes.

Geopolitical and regulatory dynamics compound operational risk. New policy moves related to processed critical minerals and ongoing export controls on advanced semiconductor manufacturing equipment are altering the timeline for capacity expansion and disrupting traditional sourcing strategies. For corporate decision‑makers this means that technology roadmaps and supply agreements must be stress‑tested against policy shocks as rigorously as against demand uncertainty.

Forward‑looking market sizing and high‑granularity scenario models—top‑level CAGR and market-size trajectories to 2032, plus alternative supply/demand and price scenarios calibrated to recent capacity shifts.

Supplier scorecards and strategic profiles—benchmarks for manufacturing scale, technology roadmap, product mix strategy, and go‑to‑market posture across the major DRAM producers.

Procurement playbooks—contracting templates, hedging approaches, and inventory strategies tailored for OEMs, hyperscalers, and enterprise buyers operating under volatile DRAM pricing.

Technology migration advisories—decision frameworks for DDR4 → DDR5 transitions, LPDDR adoption in mobile and edge devices, and module qualification sequencing aligned with JEDEC standard updates.

Supply‑chain resilience and risk registers—raw-material sensitivity analysis, alternative sourcing maps, and contingency protocols for export control and trade policy disruptions.

M&A and partnership readiness—criteria and playbooks for strategic investments, capacity access deals, and vertical partnerships that can be executed to shore up supply or capture margin upside.

The DDR RAM ecosystem is led by a small set of large producers and a cohort of regional and specialty suppliers. Leading global manufacturers continue to prioritize next‑generation DDR5 and HBM capacity while maintaining selective legacy output to capture near‑term pricing opportunities. Key dynamics we highlight in the report include:

Integrated global leaders continue to control a dominant share of capacity and technological leadership, enabling them to manage allocation between commodity DDR and higher‑margin products; their choices dictate market tightness and pricing trajectories.

Regional and specialized suppliers are increasing their relevance as alternative sources for selected product classes, especially where qualification windows and cost structures align with customer requirements.

Competitive behavior will be shaped by margin optimization, customer lock‑in through long‑term contracts, and targeted capacity investments tied to public policy incentives and export regimes.

Representative profiles included in the report (with operational insights and strategic scenarios): Samsung Electronics (Suwon, South Korea), SK hynix (Icheon, South Korea), Micron Technology (Boise, USA), CXMT (Hefei, China), Nanya Technology (Taiwan), and Winbond Electronics (Taiwan). For each, we map product portfolios, DDR5 ramp strategies, capacity allocation decisions (including HBM trade‑offs), and implications for customers seeking supply security.

JEDEC’s recent updates to DDR5 and LPDDR specifications materially affect product validation cycles and architectural choices. These standards expand performance envelopes and introduce new compliance and reliability vectors—particularly for server and AI data‑center modules. Procurement and engineering teams must harmonize qualification timelines with module availability forecasts; failing to sequence these correctly risks delayed product launches or expensive redesigns.

Immediate procurement triage: classify next‑12‑month purchases into critical, hedgable, and opportunistic buckets. Lock in strategic demand via prioritized long‑term contracts for critical SKU families while using spot markets selectively for opportunistic buys.

Accelerate qualification windows for DDR5 where performance is strategic; retain DDR4 fallback plans for cost and continuity through 2026 as suppliers phase capacity.

Operationalize alternative sourcing: expand approved vendor lists to include emerging regional suppliers and specialized module houses; build parallel qualification paths to reduce single‑source exposure.

Adopt staged inventory buffers tied to product launch cadence: small, targeted buffers for high‑value server platforms; leaner approaches for commodity client modules to minimize capital tie‑up.

Integrate policy scenario planning into supply‑chain and capex decisions—run “export control” and “raw material restriction” scenarios in capital planning to adjust timelines for new fabs and tool procurements.

Explore strategic partnerships or minority investments where securing capacity or preferential allocation is mission‑critical—this can be more cost‑effective than pure greenfield capex in the current geopolitical climate.

This research is designed for C‑suite and operational leaders across device OEMs, cloud and hyperscale providers, enterprise IT organizations, and financial sponsors evaluating investment or divestiture decisions in semiconductor and systems supply chains. The practical tools and playbooks are engineered to convert market insight into near‑term procurement and architectural actions while informing medium‑term strategic investment.

Consistent with our “trailer” approach to executive briefings, this public summary deliberately presents the strategic narrative, decision frameworks, and company‑level implications without publishing the report’s granular segmentation tables, per‑region/application percentage splits, or supplier‑level capacity and price schedules. Those detailed tables—critical for negotiating contracts, running internal price‑sensitivity models, or executing supplier scorecards—are available in the full report and accompanying data appendices.

For teams preparing 2026 procurement cycles, product launches, or investment reviews, the full PW Consulting DDR RAM Market Research package provides the scenario models, downloadable data sets, supplier scorecards, and contracting templates needed to act decisively. Contact our team to arrange a briefing, obtain the complete dataset, or commission a custom sensitivity run tailored to your SKU mix and supply‑chain topology.

For detailed analysis of this topic, please visit the official page:Ddr Ram Market Research

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com