How Is Open-Source Development Accelerating Growth in the Python Package Software Market?

Networking |

2026-03-12 05:09:46

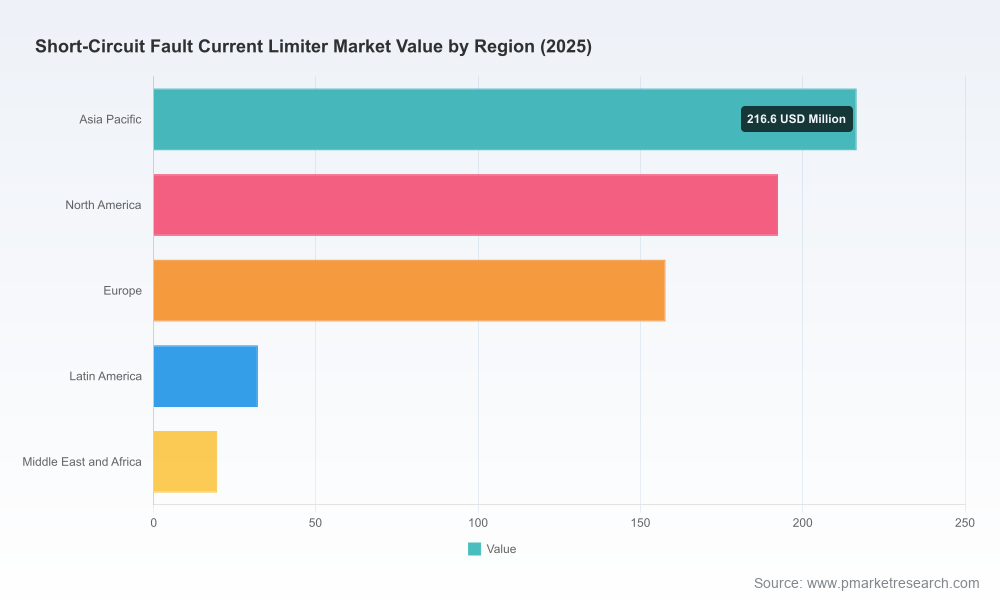

As the electricity system accelerates toward higher shares of inverter-based resources, distributed generation and aggressive decarbonization targets, fault current dynamics are rapidly evolving. PW Consulting’s Short Circuit Fault Current Limiter (FCL) Market report — base year 2025, historical review 2020–2025 and forecast through 2032 — provides the actionable intelligence executive teams need to move from defensive compliance to strategic advantage in 2026. The global market reached USD 618.5 Million in 2025 and, driven by grid modernization, renewable integration and rising protection complexity, is forecast to grow at a compound annual growth rate (CAGR) of 8.21% to exceed USD 1.07 Billion by 2032. This preview summarizes the report’s strategic value without releasing the detailed segment tables — a deliberate “trailer” designed to orient decision-makers and prompt direct engagement for the full dataset and vendor benchmarking.

Short Circuit Fault Current Limiter Market

Grid-code transitions and the proliferation of inverter interfaced resources are no longer theoretical drivers: regulators and system operators are tightening requirements for fault ride-through, controlled fault-current contribution and grid-forming capability. These changes convert FCLs from niche protective devices into core elements of secure grid architecture.

Short Circuit Fault Current Limiter Market

Capital planning cycles that begin in 2026 will determine converter and protection architectures for a decade. Procurement timelines for utilities, large IPPs and industrial microgrids must now factor in lead times, demonstration outcomes and evolving standards — delaying decisions risks stranded assets or costly retrofit programs.

Short Circuit Fault Current Limiter Market

Technology convergence — superconducting, solid-state, pyrotechnic/isolation-based and inductive/magnetic solutions — is creating multiple valid implementation paths. Each path has distinct CAPEX/OPEX, lifecycle, and integration trade-offs that must be evaluated against long-term strategy rather than short-term price signals.

Structural demand. The market’s mid-decade expansion is being driven by large-scale grid upgrades, renewables-heavy interconnections and data-center resiliency programs. These drivers are persistent, creating a multiyear replacement and retrofit opportunity rather than a one-off surge.

Regulatory tightening. Evolving grid codes emphasize fast fault response, harmonic and unbalance management, and grid-forming behavior — all of which raise the bar for protection schemes and favor FCLs that can be validated against rigorous test regimes.

Technology cost curve and materials risk. High-temperature superconductor (HTS) tape remains a key cost and supply factor for resistive SFCL designs. Advances in conductor usage and cryogenic systems targeting liquid-nitrogen operating envelopes are reducing barriers, but material availability and input cost volatility remain real procurement risks.

Interoperability and systems integration. Demonstrations combining SFCLs with rapid mechanical DC breakers and advanced control systems have shown promising technical synergy. Systems-level thinking — not component-only procurement — is increasingly essential.

Market sizing and validated forecasting model (2020–2032) with scenario pathways and sensitivity testing. The model is designed to be used by planners to stress-test budget assumptions under alternative renewable uptake and regulatory pathways.

Technology deep-dive modules that compare superconducting, solid-state, inductive, and pyrotechnic/IS-limiter approaches on performance metrics that matter in procurement: fault mitigation effectiveness, recovery time, thermal behavior, maintenance cadence, and integration requirements.

Vendor due-diligence framework and scorecards. The report’s practical templates allow buyers to evaluate vendors across product maturity, field experience, interoperability, service network and supply-chain exposure without having to invent evaluation criteria in-house.

Procurement toolkits: contract clauses for long-lead components, acceptance testing protocols, factory and site commissioning checklists, and standardized test specifications calibrated to contemporary grid codes.

Economic frameworks: total cost of ownership calculators, simple ROI models, and payback scenarios that capture capex, opex, downtime risk and avoided equipment upgrades. These are constructed so finance, asset management and engineering can converge on a single decision metric.

Case studies and technology validations. The report integrates recent high‑voltage validation results and early deployments to ground recommendations in operational performance rather than vendor claims.

PWC’s competitive analysis shows a market with moderate concentration: the three largest firms together account for a significant portion of market value and the top five capture a clear majority share. This dynamic creates both concentration risk and an opportunity for fast followers and specialists to capture niche value through technology differentiation and service excellence.

ABB Ltd. (Switzerland) — Positioned as a systems integrator with modular medium-voltage FCL offerings that emphasize compact indoor/outdoor deployment and solutions for critical, high-requirement nodes. ABB’s strength is integration into broader protection and automation portfolios.

Siemens AG / Siemens Energy (Germany) — Offers holistic fault-current solutions embedded in grid-stability product lines; its play is to leverage existing OEM relationships and system-level engineering to scale FCL adoption in transmission and distribution projects.

Schneider Electric (France) — Focused on medium- and low-voltage protection systems and industrial deployments, leveraging strong customer channels in industry and commercial segments.

Eaton Corporation (Ireland) — Emphasizes compliance-driven current-limiting for machine builders and power systems, aligning products to short-circuit current rating (SCCR) frameworks and industrial safety standards.

Nexans (France) — A leader in superconducting fault-current limiter development with high-profile alliances in rail and distribution systems, pursuing commercialization of SFCLs as a differentiator for complex networks.

LS Electric Co., Ltd. (South Korea) — Supplies rapid-action FCLs tailored to networks where conventional breakers cannot contain initial fault current, emphasizing grid operational resilience.

G&W Electric (United States) — Targets distribution-level fault management with systems designed for medium-voltage distribution networks and a field-service footprint in select markets.

GridON Ltd. (Israel) — Competes with cost-effective and modular interrupting solutions aimed at grid operators and IPPs, leveraging agility and competitive pricing.

American Superconductor Corporation (AMSC) (United States) — Develops HTS wire-based SFCLs and positions superconducting approaches as a route to resilient, compact protection schemes for meshed grid topologies.

Rongxin Power Electronic Co., Ltd. (China) — Focused on power-electronic-based FCLs optimized for power-quality uplift and short-circuit management in high-growth Asian markets.

Recent validation and early deployments underline the technology momentum. For example, high-voltage testing that combined resistive SFCLs with mechanical DC breakers demonstrated substantive fault current limitation in HVDC contexts, and a strategic alliance targeting superconducting FCL deployment for rail applications has moved into field commissioning phases. These developments serve as proof points but should be read alongside lifecycle cost, maintainability and local service coverage when forming procurement decisions.

Start with system-level requirements, not product specs. Specify the operational outcomes (e.g., maximum permissible fault contribution, restoration timeframe, interoperability with converter controls) and let suppliers demonstrate compliance through standardized tests.

Invest in staged pilots. Prioritize short, instrumented pilots that validate supplier claims in representative operating conditions. A successful pilot should de-risk integration and clarify longer-term TCO implications.

Adopt a portfolio approach. Combine technologies where appropriate — e.g., superconducting elements for key nodes and solid-state or inductive solutions where speed or modularity are paramount — to balance cost, availability and performance.

Hedge material and supplier risk. For SFCL pathways, secure long-term agreements or strategic partnerships for HTS tape or other critical inputs. Consider local assembly or regional supply nodes to reduce lead-time exposure.

Embed contractual performance guarantees. Require measurable acceptance tests, defined recovery behavior, and service-level agreements tied to grid-code compliance and plant availability.

Align internal stakeholders early. Protection engineers, system planners, procurement, and regulators should be aligned on acceptable test protocols and lifecycle cost expectations before issuing RFQs.

This preview is crafted to equip executives and technical leaders with the strategic framing needed to prioritize FCL decisions in 2026. The full PW Consulting Short Circuit Fault Current Limiter Market report contains the detailed regional and application segmentation, vendor scorecards, downloadable modeling files, step-by-step procurement templates and test-spec annexes you will need to convert strategy into contracts and installations. It also contains deep-dive analyses on supply-chain risks and scenario-priced pathways calibrated to the forecast through 2032.

For teams preparing capital plans, this report functions as a decision-accelerant: it reduces analysis time by delivering validated market sizing, risk-adjusted forecasts and operational playbooks that align engineering, commercial and regulatory requirements. If you are about to authorize pilots, update protection standards, or issue an RFP for FCLs in 2026, PW Consulting’s full dataset and vendor benchmarking will materially shorten your path to a defensible, auditable decision.

PW Consulting’s preview establishes why FCLs matter now and how 2026 decisions will shape grid resilience and cost profiles for the decade. Our full report is the operational roadmap to execute those decisions with confidence.

For detailed analysis of this topic, please visit the official page:Short Circuit Fault Current Limiter Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com