Diabetes Telemedicine Technology Market: Strategic Imperatives for 2026 — A PW Consulting Preview

As organizations plan budgets, partnerships, and go-to-market strategies for 2026, understanding where diabetes telemedicine technologies will create measurable clinical and commercial value is non‑negotiable. PW Consulting’s Diabetes Telemedicine Technology Market research — grounded in a 2020–2025 historical review and a 2026–2032 forecast — illuminates those inflection points. The global market reached an estimated USD 5,650 Million in 2025 and is projected to expand to approximately USD 13,709 Million by 2032, reflecting a compounded annual growth rate (CAGR) of 13.5% over the forecast window. This briefing explains the report’s strategic value for enterprise decision‑makers while intentionally omitting the granular segment tables that are reserved for the full report.

Diabetes Telemedicine Technology Market

Why this analysis matters for 2026 planning

- CapEx and R&D prioritization: The market trajectory indicates accelerated investment in connected glucose sensing, integrated insulin delivery, and software platforms that enable remote care. Companies must decide whether to build, buy, or partner to capture near‑term adoption waves.

- Reimbursement and commercialization timing: Policy shifts in the United States in late 2025 and early 2026 materially change the revenue calculus for RPM and asynchronous diabetes services. Capturing newly billable pathways will be a first‑mover advantage.

- Provider and payer engagement: With clinicians increasingly reliant on continuous data feeds and decision support, vendors need clear integration and clinical‑workflow strategies to achieve traction among health systems and payers.

- M&A and competitive positioning: The market exhibits measurable concentration among the largest vendors, creating both acquisition targets and strategic barriers for challengers. Executives must balance organic scale‑up against inorganic consolidation.

Report scope — What PW Consulting delivers (actionable, not academic)

- Market sizing and high‑level growth projection (2020–2032), including scenario analysis and sensitivity testing to stress‑test demand assumptions under alternative reimbursement and adoption pathways.

- Commercial playbooks for three commercialization archetypes: device OEMs, software/platform providers, and services/virtual care operators — each with prioritized GTM steps, pricing levers, and channel strategies geared to 2026 timelines.

- Regulatory and reimbursement navigator: practical checklists, coding capture templates, and payer engagement sequences tied to the latest CMS policy moves that materially affect RPM and diabetes self‑management reimbursements.

- Integration and technical deployment blueprints: EHR interfacing approaches, API evaluation scorecards, and a phased interoperability roadmap to minimize deployment friction in health systems and home care settings.

- Commercial diligence materials: buyer/seller playbooks, valuation multipliers calibrated to current market concentration and revenue growth profiles, and a shortlist of capability gaps that most often drive M&A activity.

- Seven real‑world case studies showing operational KPIs (onboarding time, clinician time‑savings, adherence uplift) and a model P&L for three go‑to‑market scenarios (pilot, regional roll‑out, national scale).

Competitive landscape: what the leading players are doing and why it matters

The competitive set spans device manufacturers, platform providers, and virtual care specialists. Each plays a distinct role in shaping clinical workflows and commercial channels. PW Consulting’s report synthesizes partner playbooks and competitive moats based on recent product launches, integrations, and regulatory events:

Diabetes Telemedicine Technology Market

- Dexcom and Abbott: As leaders in real‑time continuous glucose monitoring, their emphasis on data sharing, cloud analytics, and interoperability is driving expectations for always‑on monitoring in remote care pathways.

- Medtronic: The combination of insulin delivery systems and CGM integration is accelerating closed‑loop and hybrid automated insulin delivery adoption; regulatory approvals for device integrations strengthen propositions for home‑based, clinician‑supervised care.

- Teladoc Health (Livongo): The virtual care operator model — integrating coaching, supplies, and telehealth encounters — highlights the value of bundled chronic‑care subscriptions that ladder into population health contracts.

- Glooko: As a platform aggregator, its device‑agnostic syncing and EHR integrations reduce clinician friction and become pivotal in multi‑vendor deployments across health systems.

- Virta Health: Demonstrating clinical outcomes via continuous remote care, Virta’s model underscores the commercial upside of outcome‑linked contracts and digital therapeutics approaches for type 2 diabetes.

- Podimetrics: A focused remote monitoring niche — preventing diabetic foot complications — illustrates how verticalized RPM solutions can unlock payer interest and differentiated reimbursement pathways.

Recent strategic moves underscore near‑term priorities: Podimetrics launched an expanded SmartMat+ product in late 2025 to broaden complication prevention capabilities; Medtronic secured regulatory clearance to integrate a leading sensor with its automated delivery system in 2025; and U.S. policy changes in early 2026 expanded RPM codes and telehealth flexibilities relevant to diabetes self‑management. Together, these events compress time‑to‑value for companies that can operationalize new billing pathways and integrate devices into clinical workflows.

Diabetes Telemedicine Technology Market

Regulatory and reimbursement dynamics — the near‑term levers

- Policy updates have extended Medicare telehealth flexibilities and introduced new RPM codes that shorten monitoring intervals and recognize management time; these should materially improve short‑term revenue capture for RPM and virtual diabetes education programs.

- The Medicare Diabetes Prevention Program now supports on‑demand asynchronous delivery options, which expands the addressable population for digital prevention and risk‑stratified programs.

- Providers and vendors must prepare coding, documentation, and care‑pathway modifications now to realize reimbursement in 2026; delayed operational readiness will likely defer revenue into later years despite favorable policy tailwinds.

Market structure and strategic implications

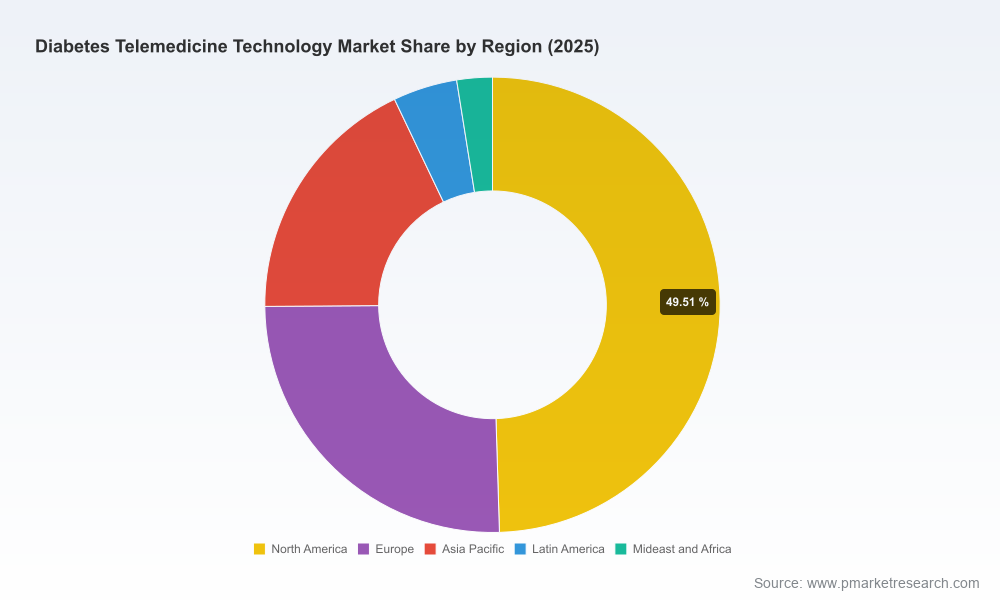

The market shows notable concentration at the top — the three largest players account for a majority share of market revenues, with the top five occupying an even larger share. For strategists this creates a clear set of choices:

- Challengers should pursue niche verticalization (e.g., complication prevention, pediatric care, or integrated behavioral health) where incumbents lack full coverage.

- Platform plays that enable multi‑vendor orchestration (device neutrality, robust APIs, configurable clinician dashboards) can become neutral integrators that capture platform economics without owning hardware margins.

- Large incumbents will continue to leverage scale for payer contracting and device bundling; partnerships or bolt‑on M&A remain the fastest route for scale‑seeking firms.

Recommended 90‑day and 12‑month actions for enterprise leaders

- 90 days — Tactical readiness: Complete a reimbursement gap assessment, prioritize the fastest billable pathways (using new RPM codes), and stand up a commercial pilot with defined success metrics tied to reimbursement capture.

- 6–12 months — Operational scale: Execute EHR integrations, finalize payer contracting templates, and establish clinician enablement programs. Consider targeted partnerships with a device supplier or platform provider to accelerate go‑to‑market.

- 12 months — Strategic positioning: Evaluate M&A or strategic alliances to close capability gaps (data analytics, chronic‑care coaches, supply chain for testing supplies) and move from pilots to value‑based reimbursement arrangements.

What PW Consulting purposely omits here — and why

This preview is designed as a strategic “trailer”: it presents the high‑level market trajectory, strategic implications, and practical playbooks while intentionally omitting the itemized regional and fine‑grained segment revenue tables that many competitors publish. The full report contains detailed breakdowns by region, technology type, and end‑user, plus vendor market shares, price‑elasticity modeling, and downloadable financial models. Those elements are essential for transactional diligence and tactical budgeting, and they are available exclusively in the comprehensive report.

Closing — The strategic payoff for 2026

Enterprises that move quickly in 2026 stand to capture disproportionate value: policy changes create immediate billing opportunities; device and platform integrations reduce clinical friction; and category leaders continue to consolidate scale advantages. PW Consulting’s Diabetes Telemedicine Technology Market research equips executives with the scenarios, playbooks, and operational checklists required to convert that opportunity into sustainable market share. For teams preparing 2026 budgets, partner roadmaps, or M&A pipelines, the question is not whether to enter the market, but how to sequence investments to capture reimbursement, clinical adoption, and payer contracting advantages before competition intensifies.

For access to the full dataset, detailed segmentation, and the actionable templates referenced above, PW Consulting’s full report and downloadable toolkits are available on the official report page.

For detailed analysis of this topic, please visit the official page:Diabetes Telemedicine Technology Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com