5G Expansion and Smart Connectivity Drive Global Low Noise Amplifier Market Toward $12.8 Billion by 2031

Other |

2026-05-12 04:45:07

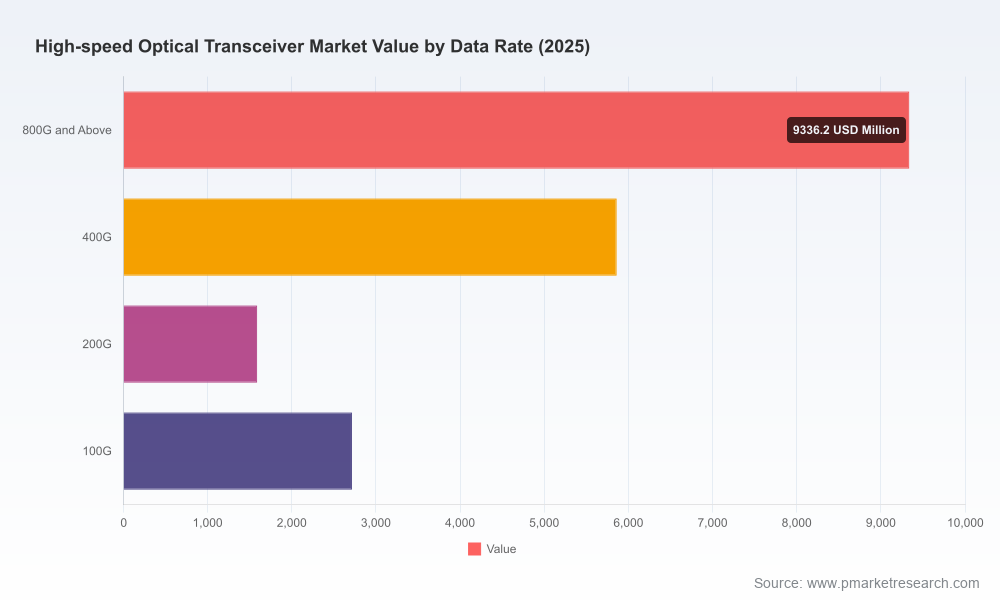

As hyperscale cloud, 5G transport, and AI-accelerated data centers enter an inflection point, PW Consulting’s new High Speed Optical Transceiver Market report furnishes the forward-looking intelligence that enterprise and infrastructure investors need to act in 2026. The market reached USD 19,500 Million in the base year 2025 and, under our central modelling, is projected to expand to USD 55,030 Million by 2032 — a compound annual growth rate (CAGR) of 15.48% over the 2026–2032 forecast window. That pace reflects an industry simultaneously driven by escalating lane rates, new pluggable form factors, and rapid coalescence around silicon photonics and coherent pluggable architectures.

High Speed Optical Transceiver Market

Timing of infrastructure investments: With upgrade cycles for switches, routers, and DCI equipment increasingly tied to 800G/1.6T readiness, procurement windows in 2026 will determine whether organizations buy for near-term interoperability or for multi-year scaling.

High Speed Optical Transceiver Market

Technology choice and product roadmaps: The trade-offs between PAM4 pluggables, coherent ZR family optics, and emerging silicon photonics topologies are no longer academic — they materially affect capital intensity, power budgets, and service economics.

High Speed Optical Transceiver Market

Supply chain and regulatory risk: Raw material constraints, export-control dynamics, and MSA releases are reshaping supplier selection and inventory strategies; enterprises must balance cost, lead-time, and compliance simultaneously.

M&A and partnership prioritization: As the vendor landscape consolidates around a small group of technology leaders, acquirers and strategic partners can materially accelerate time-to-market or secure critical intellectual property stacks.

Several converging forces are accelerating both demand and supplier response. First, network infrastructure owners report that high-speed transceivers account for a meaningful share of total data center networking hardware costs in 400G+ deployments — a structural driver pushing buyers to optimize total cost of ownership (TCO), not only unit price. Second, standards maturation (including recent finalization of IEEE workstreams and new MSA releases) is reducing interoperability risk, enabling buyers to plan for higher-rate pluggables with clearer upgrade paths.

On the supply side, semiconductor and photonics inputs are under pressure: laser technologies (VCSEL and EML) saw price increases driven by wafer constraints, which compress gross margins for vendors that have not vertically integrated supply. At the same time, export-control policies affecting high-bandwidth optical components have introduced geopolitical sourcing complexity that materially changes qualification timetables for global procurement teams. Collectively, these dynamics mean buyers must embed scenario-driven buffers into both CapEx and inventory planning in 2026.

The market is characterized by a mix of technology leaders, specialist photonics firms, and high-volume module manufacturers. Our analysis shows a moderate-to-high level of concentration: the top three suppliers collectively hold a substantial share of revenue, and the top five represent an even larger proportion — a structure that influences pricing power, qualification cycles, and the speed of cross-MSA adoption.

Silicon-photonics and DSP-focused leaders (e.g., Coherent and II‑VI’s capabilities) are moving ahead on high-bandwidth, low-power solutions aimed at short-reach data center interconnects and AI fabrics. Their roadmaps emphasize integration and lower power per bit.

High-volume module manufacturers (notable firms headquartered across APAC and North America) sustain scale advantage for QSFP-DD and OSFP family modules, particularly in hyperscaler and carrier deployments where cost-per-bit remains a dominant procurement metric.

Traditional telecom optics suppliers (including specialists in coherent pluggable optics) are accelerating shipments of ZR/ZR+ form factors to meet DCI and metro demand, shifting some portion of optical spend from line cards to pluggable modules.

Networking OEMs that also offer optics (e.g., Cisco) are leveraging system-level interoperability to reduce integration friction for large network operators, but buyers should still validate multi-vendor performance in production workloads.

Recent product and standards developments underscore speed to market: major vendors launched next-generation 800G and 1.6T pluggables throughout 2025, hyperscaler certifications for 800G silicon-photonics interfaces were announced, and industry bodies completed high-speed electrical and optical interface specs that unlock 1.6T module designs. For procurement and engineering teams, these milestones translate into a compressed qualification runway and a need to prioritize interoperability testing now, not later.

Our report is organized to move teams from insight to execution. Key practical contents include:

Transparent market model (2020–2025 historical, 2026–2032 forecast) with parameterized drivers so you can run bespoke scenarios against capacity, price, and adoption assumptions.

TCO calculators that compare coherent pluggables, PAM4 pluggables, and silicon photonics across CapEx, power, and operational expense over multi-year horizons.

Supplier scorecards and red-team assessments covering technology maturity, manufacturing scale, supply chain resiliency, and export-control exposure.

Procurement playbooks including RFP templates, qualification checklists, and recommended multi-vendor sourcing strategies to mitigate single-point supplier risk.

Product roadmap templates and time-to-market scenarios to inform chipset selection, form-factor commitments, and interoperability testing cadence.

Regulatory and compliance playbooks aligned to recent export-control guidance and standards releases to de-risk cross-border sourcing.

Case studies and vendor negotiation checklists derived from real-world engagements with hyperscalers, telcos, and cloud providers.

Those deliverables are intentionally operational: hands-on tools for procurement, engineering, finance, and corporate development teams charged with decisions in 2026 and beyond.

Adopt hybrid sourcing and pre-qualification of at least two alternate suppliers per critical form factor. Given supplier concentration and geopolitical uncertainty, dual-sourcing reduces program risk and shortens recovery time for supply disruptions.

Accelerate architectural trials of silicon photonics for workloads where power and density materially affect TCO. Run short pilots in controlled DCI or AI fabric segments before enterprise-wide rollouts.

Secure long-lead components via multi-year agreements where price and availability of lasers and wafers create bottlenecks. Conditional forward purchasing and supplier-backed guarantees can stabilize manufacturing cadence.

Coordinate switch/router upgrade cycles with form-factor roadmaps. Avoid stranded capital by aligning procurement timing with MSA and standards milestones that affect pluggable compatibility.

Embed export-control and compliance checks into vendor selection. Vendors’ geopolitical exposure will influence qualification timelines and usable capacity for global rollouts.

Use scenario-based CapEx planning. Base budgets on our central forecast (CAGR ~15.5%), but stress-test against higher-adoption and lower-price trajectories to understand cash-flow impacts.

Leaders should treat our market figures as an operational planning input rather than a static projection. Use the report’s parametrized model to:

Build procurement cadence maps that tie vendor lead-times to switch refresh schedules;

Model incremental power and cooling investments tied to port-density increases;

Stress-test supplier portfolios under scenarios of component price inflation and export-control disruption;

Inform R&D prioritization between integration, thermal management, and DSP optimization to capture premium segments.

The High Speed Optical Transceiver market is entering a phase where technology selection, supplier footprint, and procurement timing will lock in performance and cost structures for years. With a projected trajectory from USD 19,500 Million in 2025 to USD 55,030 Million by 2032 at a 15.48% CAGR, the scale of opportunity is clear — but so are the execution risks. PW Consulting’s report distills the complexity into operational tools and strategic prescriptions that buyers and investors can use immediately to de-risk programs and capture upside.

For teams preparing capital plans, vendor negotiations, or R&D roadmaps for 2026, our research functions as both a decision instrument and a playbook. To access the full dataset, segmented scenarios, and vendor-level scorecards (exclusive to the report), please visit the PW Consulting report page or contact our advisory team for a tailored briefing and implementation workshop.

For detailed analysis of this topic, please visit the official page:High Speed Optical Transceiver Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com