Electronically Scanned Array Market Forecast

Other |

2026-05-27 11:14:07

PW Consulting’s latest market study on Automotive Cross-Domain Electrical/Electronic (E/E) Architectures delivers a tactical playbook for automotive OEMs, Tier-1 suppliers, semiconductor firms, and strategic investors preparing capital allocation and product roadmaps for 2026 and beyond. Drawing on a 2020–2025 historical baseline and a 2026–2032 forecast horizon, the report synthesizes market sizing, technology trajectories, regulatory pressure points, and vendor strategies into an actionable framework that informs near-term program choices while preserving optionality for multi-year software-defined vehicle (SDV) transitions.

Automotive Cross Domain E E Architecture Market

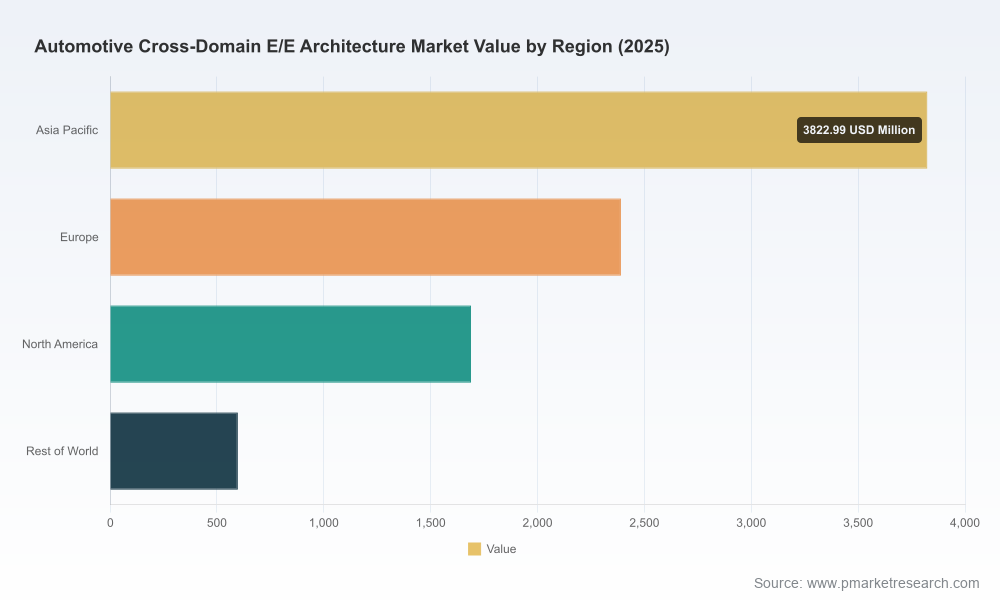

Rapid scale-up: The cross-domain E/E market has moved from a nascent cluster of pilot programs to an industry-wide migration vector. Our topline shows the market growing from the low single-digit billions in 2020 to roughly mid-single-digit billions by the 2025 base year, and, at a compound annual growth rate (CAGR) of 16.55% over the forecast period, accelerating toward a multi-ten-billion dollar industry by 2032. That trajectory demands that strategic choices made in 2026 be durable across successive platform cycles.

Automotive Cross Domain E E Architecture Market

Decision inflection: 2026 is the practical inflection point for many OEMs—programs awarded that year will determine whether an OEM pursues zonal, centralized, or hybrid server-based E/E architectures for the next decade. The report calibrates trade-offs between near-term cost, long-term total cost of ownership (TCO), and software velocity.

Automotive Cross Domain E E Architecture Market

Regulatory and safety constraints: With global mandates like UNECE R155/R156 and engineering standards such as ISO/SAE 21434 as de facto constraints, 2026 procurement and architecture blueprints must embed cybersecurity and update-management requirements from day one. The report maps compliance responsibilities across architecture layers to minimize rework risk and certification delays.

Across 2020–2025 the market experienced double-digit expansion as electrification, ADAS/AD feature proliferation, and the shift to software-defined vehicle models pushed OEMs toward cross-domain consolidation. Our modeling shows this acceleration continuing into the forecast (2026–2032) underpinned by three structural drivers:

Architecture consolidation: Zonal and centralized approaches reduce wiring complexity, enable higher compute utilization, and simplify vehicle derivative management—releasing engineering capacity and lowering hardware BOM for multiple derivatives over platform life.

Software acceleration: OTA updates and cloud-native service patterns require run-time environments and middleware that cross traditional domain boundaries (powertrain, chassis, ADAS, infotainment). This raises the premium on standardized inter-domain interfaces, secure over-the-air frameworks, and compute fabrics that guarantee real-time behavior.

Regulatory pressure: Safety and cybersecurity regulations are not only compliance items but architecture constraints. UNECE mandates and ISO/SAE engineering expectations force SRM/CSMS-aligned lifecycle processes, making once-experimental cross-domain patterns a procurement prerequisite.

Pick your migration archetype and align procurement timelines. The decision to adopt zonal, domain-centralized, or fully centralized server-based E/E topologies will determine supplier ecosystems, software toolchains, and hardware refresh cadence. The report defines five migration archetypes with recommended procurement windows to avoid costly mid-cycle re-architecture.

Embed cybersecurity and update management into the architecture contract. Under UNECE R155/R156 expectations, OEMs must treat CSMS and secure updateability as first-class product requirements. Our checklist maps requirements to contract line items and integration gates to avoid scope creep during validation.

Prioritize middleware and functional partitions for software velocity. Hardware choices are necessary but not sufficient—software frameworks, virtualization strategies, and middleware selection (including cloud-native readiness) determine the velocity of feature rollouts. The report supplies a decision matrix that ranks middleware options by determinism, safety assurance cost, and scalability.

Assess TCO with scenario-based sensitivity. We provide model templates showing TCO sensitivity to compute refresh cycles, OTA frequency, warranty exposure, and cybersecurity remediation scenarios—enabling CFOs to compare capital investment against reduced ongoing engineering and service costs.

The market is coalescing around a set of suppliers that combine domain knowledge with systems-level integration capabilities. The report includes a vendor capability matrix and comparative briefings on leading players to inform sourcing strategy without presupposing a single “winner.” Highlights:

Robert Bosch GmbH (Germany) — Known for cross-domain vehicle computers and zone-oriented E/E architectures, Bosch emphasizes high-performance computing solutions that consolidate functions across powertrain, chassis, ADAS, and cockpit domains. Their offering is positioned for OEMs seeking deep integration across traditional hardware boundaries.

Continental AG (Germany) — Continental is advancing server-based E/E through both high-performance computers and zone control units (ZCUs). Recent product implementations and series introductions demonstrate a go-to-market focus on combining integrated cockpit and vehicle functions for SDVs.

Aptiv PLC (Ireland) — Aptiv’s Smart Vehicle Architecture (SVA) separates I/O from compute via zone controllers and a cross-domain software infrastructure. Their December 2025 LINC platform announcement signals a move toward cloud-native, infrastructure-first approaches for SDV ecosystems.

ZF Friedrichshafen AG (Germany) — ZF provides high-performance domain controllers and solutions that emphasize integration of vehicle motion, chassis, and safety functions. Their solutions target customers prioritizing deterministic control and safety-critical integration.

DENSO Corporation (Japan) — With broad reach in domain and zonal controllers, DENSO brings supplier depth in production-intent components and tight OEM relationships, especially in platforms where thermal, power, and mechanical constraints are critical.

Valeo SE (France) & Magna International Inc. (Canada) — These system suppliers complement electronics with domain expertise in electrification and vehicle integration, addressing both component supply and systems-level packaging for zonal strategies.

NXP Semiconductors (Netherlands) & Infineon Technologies AG (Germany) — Semiconductor incumbents offer processors, SoCs, microcontrollers, and power semiconductors optimized for zonal and cross-domain compute fabrics; their roadmaps anchor hardware roadmaps and enable real-time cross-domain functions.

Our competitive assessment purposely avoids overstating consolidation: while market leadership is emerging, supplier combinations and strategic partnerships remain fluid. The report contains supplier-comparison templates and negotiation levers tailored to 2026 sourcing timelines.

Market sizing and forecast models (base year 2025, forecast 2026–2032) with scenario layers that reflect adoption curves for zonal and centralized E/E topologies.

Architecture decision frameworks that codify trade-offs across BOM cost, software velocity, certification risk, and vehicle derivative economics.

Compliance mapping: actionable checklists for UNECE R155/R156 and ISO/SAE 21434 alignment across procurement, development, and operations.

Vendor capability matrix and integration readiness scores, including system integration risk factors and suggested sourcing stacks for different OEM strategic archetypes.

Implementation playbooks: reference workstreams, testing and validation milestones, OTA governance models, and a phased migration roadmap (pilot → scale → sustain) calibrated to 2026 program cycles.

TCO and sensitivity models with downloadable templates to stress-test capital and operating assumptions under alternative update cadence and compute-refresh scenarios.

Use-case bank and IP mapping that identifies where off-the-shelf platforms suffice and where bespoke software investments are required to protect competitive differentiation.

Productization activity is accelerating: Continental’s demonstrations of integrated HPCs and its series introduction of ZCUs signal a shift from prototypes to production-intent hardware across multiple OEMs.

Software-first vendor moves: Aptiv’s platform announcements reflect a broader industry tilt toward cloud-native, middleware-led approaches—adding new requirements for orchestration and lifecycle management.

Regulation is a gating factor: Compliance expectations are already influencing supplier selection, contractual clauses, and certification timelines. Treating cybersecurity and update management as tablestakes is now a sourcing imperative.

For OEM strategy teams: Use the migration archetypes and TCO scenarios to set platform-level budgets and to determine which program awards in 2026 will include hardware refreshes versus software-only deferrals.

For Tier-1 suppliers: Leverage the vendor capability scoring to identify white-space where systems integration, safety engineering, or middleware packaging can create differentiated commercial propositions for OEMs constrained by certification windows.

For semiconductor and software vendors: Map product roadmaps against the compute and real-time requirements captured in the report; align roadmap milestones to OEM procurement cycles to maximize design-win probability.

For investors and M&A teams: Use the market trajectory and competitive mapping to prioritize opportunities that offer software-based monetization and long-term recurring revenue potential from OTA and service ecosystems.

Cross-domain E/E architecture is no longer an experimental frontier—it is the structural backbone for the software-defined vehicle era. With the market expanding rapidly from the 2020–2025 base and a robust forecast through 2032 at a projected CAGR of 16.55%, 2026 decisions will materially shape platform economics and competitive positioning for the next decade. PW Consulting’s report provides the practical, procurement-ready instruments—decision matrices, compliance mappings, TCO models, and vendor playbooks—that enterprise leaders need to de-risk those decisions.

To review detailed models, vendor scorecards, and the full set of migration archetypes (including downloadable templates and negotiation playbooks), access the full report and accompanying datasets on the PW Consulting report page. The executive summary here intentionally outlines strategic direction while preserving the granular datasets and scenario outputs for subscribers and purchasers—ensuring you base program-critical actions on verified, up-to-date intelligence.

For detailed analysis of this topic, please visit the official page:Automotive Cross Domain E E Architecture Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com