Specialty Films Polymer Market Size, Share & Industry Analysis Report 2026–2032

Other |

2026-06-04 06:24:50

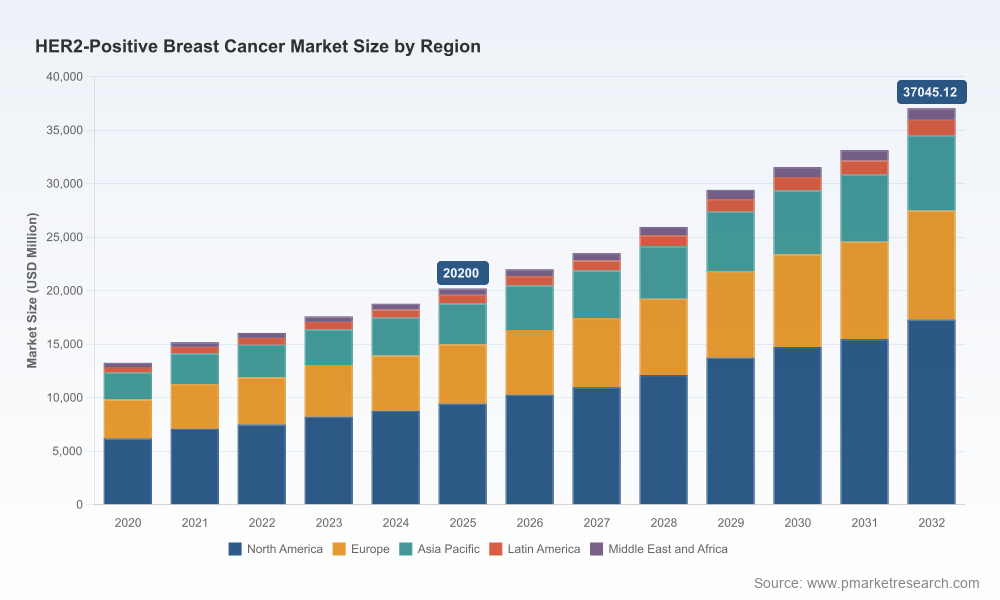

PW Consulting’s new market intelligence brief on HER2-positive breast cancer synthesizes commercial, clinical, regulatory and payer dynamics into a single, action-oriented roadmap for 2026 corporate planning cycles. Using 2025 as the base year and a scenario-driven forecast horizon through 2032, our analysis quantifies a robust market expansion trajectory: the global market is estimated at approximately USD 20.2 billion in 2025 and is forecast to grow at a compound annual growth rate of roughly 9.05% through 2032, producing a materially larger addressable opportunity by the end of the forecast period.

HER2-Positive Breast Cancer Market

Therapeutic innovation is shifting the competitive frontier. Antibody‑drug conjugates (ADCs) that convert biological specificity into cytotoxic payload delivery are moving from niche to mainstream in HER2-positive care pathways. Regulatory expansions for ADCs into earlier disease settings are increasing potential patient exposure and changing line‑of‑therapy dynamics.

HER2-Positive Breast Cancer Market

Biosimilars have reshaped the cost and access baseline. The expiry of foundational monoclonal antibody patents and the rapid commercialization of trastuzumab biosimilars have already altered procurement, contracting and hospital formulary behavior in multiple markets, accelerating volume uptake but compressing originator price premiums.

HER2-Positive Breast Cancer Market

Market concentration remains high. A small group of multinational biopharmaceutical firms continue to control the majority of branded HER2 franchises, while a growing number of biosimilar and specialty players compete on price and service. This asymmetric concentration creates both barriers and structured partnership opportunities for entrants and incumbents alike.

Non‑clinical factors — reimbursement frameworks, supply chain robustness and regulatory nuance around interchangeability — are increasingly decisive for commercial outcomes. Companies that align clinical value with payer evidence and secure resilient manufacturing footprints will de‑risk near‑term launch execution.

Concise market sizing and forward-looking forecast model built from first principles and cross‑validated with proprietary sales intelligence — delivered with scenario toggles for adoption, pricing and access outcomes.

Competitive scorecards and playbooks for leading originator, ADC and biosimilar players, including capability maps, go‑to‑market strengths and vulnerability analysis at molecule and corporate levels.

Regulatory and reimbursement decision calendars, with event‑level impact estimates and contingency strategies for regulatory approvals, label expansions and payer policy shifts expected through 2026–2028.

Payer economics and contracting templates: short‑form models that translate clinical benefit into net price and budget impact under common reimbursement architectures, with sensitivity levers for discounting, outcomes‑based arrangements and multi‑year procurement.

Manufacturing and distribution risk map that flags single‑point dependencies, expected capacity bottlenecks for specialized biologics and ADCs, and mitigation playbooks for supply continuity.

M&A and partnership heatmaps identifying high‑value targets (by technology, geographic reach, or manufacturing capability) and an evaluation framework for prioritizing inorganic plays in 2026.

Commercial launch checklists and field deployment sequencing for ADCs and combination regimens, tailored to different payer archetypes and hospital procurement behaviors.

Note: this press release intentionally omits the core granular segmentation tables and proprietary regional/applicational shares contained in the full deliverable; these are available exclusively from PW Consulting to ensure clients obtain the full decision‑grade dataset and model.

Portfolio prioritization: For companies with late‑stage ADC assets or ADC manufacturing capabilities, 2026 is the window to accelerate late‑stage investment and launch readiness. ADCs are the fastest growing therapeutic class within the HER2 landscape and will command differentiated pricing and access expectations. Companies without ADC exposure should evaluate alliance or licensing plays to participate in this growth vector.

Biosimilar strategy: Firms with trastuzumab biosimilars must balance aggressive win‑share tactics with margin preservation. Contracting strategies that combine service guarantees (e.g., secure supply, patient support) with tiered pricing will outperform pure price‑only approaches in hospital tender markets.

Market access and evidence generation: Payers are increasingly requiring real‑world evidence (RWE) and comparative effectiveness data for higher‑cost regimens, especially ADCs and combination therapies. Allocate budget to post‑launch RWE programs designed to demonstrate durability of response, resource utilization savings and subpopulation benefit — these data will materially influence formulary placement.

M&A and partnerships: Mid‑cap acquisition targets include specialty manufacturing assets (ADC conjugation, cytotoxin supply), regional biosimilar producers with established distribution networks, and clinical-stage companies with novel HER2‑directed modalities. Strategic partnerships that secure manufacturing capacity or accelerate label expansions are likely to deliver faster time‑to‑value than greenfield builds.

Supply chain resiliency: Recent disruptions linked to high biosimilar demand and concentrated API suppliers stress the need for dual‑sourcing strategies, validated secondary suppliers and capacity reservation clauses in contracts for critical biologic inputs.

Pricing architecture: ADCs will command premium list prices driven by complex manufacturing and meaningful clinical differentiation, while biosimilars compete in a volume‑driven economics model. Net pricing strategies must be built on transparent payer models and include outcomes‑linked components where feasible.

The competitive map in HER2-positive breast cancer is a mosaic of global originators, ADC innovators, niche specialty producers and an increasingly crowded biosimilar field. Key strategic positions and recent milestones to watch:

Roche / Genentech — continue to anchor the market with a broad HER2 franchise and combination formulations. Their depth in clinical datasets and broad hospital relationships provide durable advantages, but they face margin pressure from biosimilar uptake and must defend share in a contracting environment.

AstraZeneca / Daiichi Sankyo — have turned trastuzumab deruxtecan into a category‑defining ADC. Regulatory expansions into earlier disease settings materially increase addressable volume and influence standard‑of‑care conversations across oncology networks.

Pfizer (including assets from acquisitions) — is leveraging targeted kinase inhibitors in combination regimens to carve differentiated niches in metastatic settings; positive combination trial readouts strengthen bargaining power with payers for bundled regimens.

Large biosimilar players (Amgen, Biocon Biologics, Viatris, Celltrion, Samsung Bioepis) — have rapidly commercialized trastuzumab biosimilars and are shaping procurement dynamics. Their competitive playbooks emphasize hospital penetration, tender optimization and lifecycle extension through additional indications and service offerings.

Recent public milestones (regulatory approvals, trial readouts and biosimilar launches) have compressed timelines and raised the floor for commercial expectations. Patent expiries enabled biosimilar capture of significant market share within a few years, and the competitive response towards combination regimens and ADCs will be decisive for originators’ mid‑term economics.

Regulatory setbacks or unexpected safety signals in ADC programs could delay label expansions and depress premium pricing expectations.

Accelerated biosimilar uptake in hospital and government procurement settings could compress overall market revenue growth below base forecasts despite volume expansion.

Supply interruptions for complex biologics or cytotoxic payloads would disproportionately affect high‑margin ADC launches and could create short‑term scarcity that reshapes contracting outcomes.

Shifts in payer policy: stronger demands for head‑to‑head evidence or tighter reimbursement ceilings would alter go‑to‑market sequencing and may necessitate re‑pricing or outcomes‑based contracting pilots.

Executive teams should use our scenario model to stress‑test capital allocation choices between ADC commercialization, biosimilar scale expansion and M&A. The model quantifies break‑even timelines under conservative and accelerated adoption scenarios.

Commercial leaders should adopt a two‑track launch playbook: (1) a payer‑first evidence generation plan to secure formulary positioning, and (2) a service and supply guarantee package to win hospital procurement tenders.

M&A and BD leaders should prioritize targets that offer either de‑risked manufacturing capacity or late‑stage clinical programs that accelerate entry into earlier lines of therapy.

This briefing is a strategic preview. The full PW Consulting HER2-Positive Breast Cancer Market report includes the complete proprietary forecast model (with downloadable Excel scenarios), full company dossiers and scorecards, granular segmentation and regional forecasting, payer pricing matrices and a 12‑month event calendar with quantified impact scenarios. These datasets and tools are the practical instruments we use with executive teams to convert insight into a 90‑day action plan and a 24‑month implementation roadmap.

PW Consulting is a global strategy advisor specializing in life sciences commercialization, market access and M&A advisory. Our senior consultants combine operational experience in oncology launches with quantitative modeling and regulatory intelligence to help clients convert scientific innovation into sustainable commercial value.

For access to the full report, bespoke briefings and custom modeling support for 2026 planning, please contact PW Consulting’s HER2 practice team through our website. The complete report contains the detailed segmented datasets and executable playbooks referenced above — the crucial inputs for confident, time‑sensitive strategic decisions in 2026.

For detailed analysis of this topic, please visit the official page:HER2-Positive Breast Cancer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com