Industrial Sodium Nitrate Market: Strategic Outlook for 2026 — PW Consulting Insights

Executive Summary

As companies set strategy for 2026, understanding end‑market dynamics and cost drivers in industrial sodium nitrate is a non‑negotiable. Our new market study benchmarks the sector against a clear historical trajectory and a conservative forward view: the global industrial sodium nitrate market reached approximately USD 520.0 Million in 2025 (base year) after a steady recovery from 2020, and is projected to expand through the 2026–2032 forecast window at a compound annual growth rate (CAGR) of 4.02%, reaching roughly USD 685 Million by 2032 under the base scenario. These headline metrics anchor a practical decision framework for procurement, manufacturing footprint, commercial planning and capital allocation in the year ahead.

Industrial Sodium Nitrate Market

What PW Consulting’s Report Delivers

- Actionable market sizing and a transparent forecast framework (2026–2032) calibrated to observable price and cost signals.

- An operational cost‑curve for sodium nitrate production that integrates feedstock sensitivity to nitric acid and soda ash prices, enabling scenario‑based margin analysis.

- Competitive intelligence on major producers, capacities and strategic positioning — from caliche‑sourced incumbent producers to diversified chemical groups and regional manufacturers.

- Price‑benchmarking and short‑term outlooks for key trading corridors, supported by recent observed movements and drivers.

- Regulatory and ESG implications, including capital and operating cost estimates for emissions and effluent controls required for compliance.

- A deal‑ready M&A and partnership playbook, including target screens, valuation levers and integration risks tailored to strategic acquirers.

Market Dynamics: Drivers, Price Signals and Cost Risks

Three structural forces should shape boardroom decisions in 2026:

Industrial Sodium Nitrate Market

- Feedstock linkage: Sodium nitrate manufacturing remains closely coupled to upstream nitric acid and soda ash (sodium carbonate) markets. Variability in these inputs materially alters producer margins and can flip short‑term price trends, making feedstock hedging and supplier contracts central to procurement strategy.

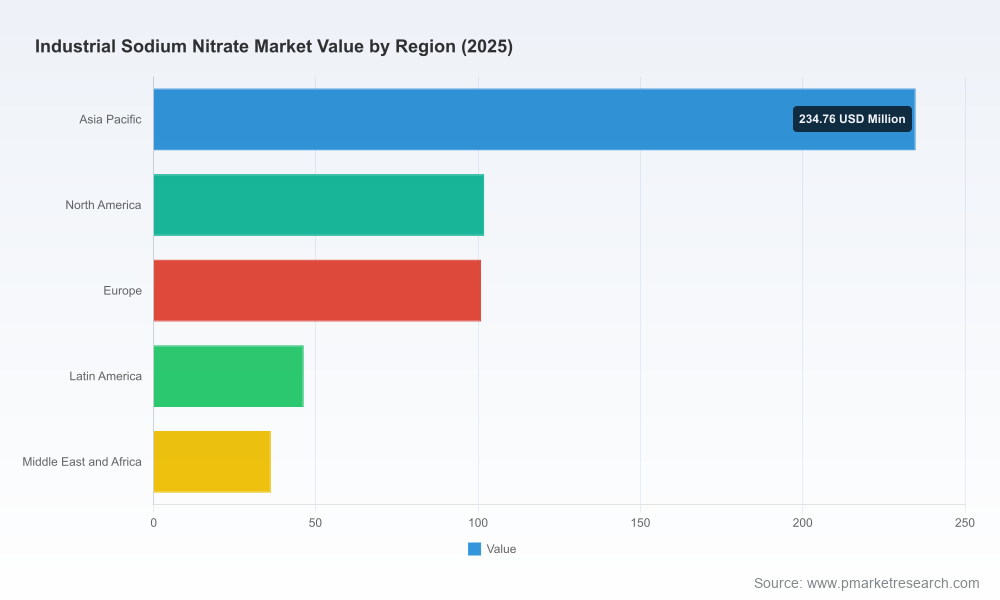

- Regional price dispersion and cyclical demand: Recent price observations exemplify how regional end‑market performance diverges. In Europe, prices moved modestly higher into March 2026, driven by steady demand and firmer upstream costs. By contrast, North American spot levels softened meaningfully compared with late 2025 on the back of weaker end‑market uptake and lower feedstock costs. In Asia, late‑2024 downward pressure was visible, linked to falling soda ash prices and subdued demand. These asymmetric movements create arbitrage opportunities but also complicate global sourcing and hedging decisions.

- Regulatory and environmental pressure: Production and application of nitrogen salts are increasingly scrutinized for impacts on water quality and soil health. Compliance requires capital investment in cleaner production technologies, effluent treatment and monitoring systems — costs that must be incorporated into any capex or expansion evaluation.

Competitive Landscape and Strategic Positioning

The market exhibits a moderate concentration profile: the top three players control a significant portion of the market, with the top five expanding that share further. This structure produces three practical implications for 2026 strategy:

Industrial Sodium Nitrate Market

- Scale advantages matter for feedstock procurement and logistics. Large incumbent producers retain cost leadership in several value chains, particularly where natural deposits or integrated supply chains exist.

- Regional and specialty players can capture attractive niches by focusing on high‑purity grades, value‑added formulations, or service‑oriented supply models that large producers do not prioritize.

- M&A and bolt‑on investments remain viable paths for accelerating access to markets or capacity — especially where a buyer can extract synergies in procurement, distribution or regulatory compliance.

Our analysis profiles major industry participants and their strategic postures. Producers with natural resource access and long‑term capacity plans continue to shape global supply expectations. Notable recent moves include a capacity expansion announced by a major Indian chemicals group with a new facility in Oman (mid‑2025), and production updates from a leading Chilean caliche producer indicating ongoing projects to lift volumes while addressing environmental performance (early 2025). These developments reinforce two themes: ongoing capacity optimization among established players, and the strategic use of geographically targeted investments to manage logistics and regulatory exposure.

Strategic Implications for Corporate Decision‑Making in 2026

For executives building 2026 plans, we recommend prioritizing six pragmatic workstreams informed by our report’s findings:

- Procurement and Feedstock Strategy: Lock in multi‑year feedstock contracts where possible, or implement dynamic hedging linked explicitly to nitric acid and soda ash indices. Where geography permits, evaluate vertical integration or captive supply to insulate margins from commodity cycles.

- Capex Prioritization: Calibrate capacity additions against our scenario set — the base case supports measured growth, but upside scenarios driven by faster adoption in thermal storage or industrial process heat could justify accelerated investment. Always include incremental compliance capex for effluent and emissions controls in financial models.

- Product and Commercial Differentiation: Invest selectively in higher‑purity grades and service capabilities (custom packaging, quality traceability) to defend margins. Specialty applications and long‑term offtake contracts can reduce exposure to spot price swings.

- Geographic and Logistics Strategy: Use the asymmetric regional price environment to inform sourcing and distribution. Tactical short‑term arbitrage may be attractive, but structural positioning should prioritize stable demand centers and reliable logistics corridors.

- M&A and Partnerships: Target acquisitions that deliver feedstock synergies, regulatory know‑how, or access to specialty niches. Our report’s target screen highlights candidates whose value is underpinned by integration upside rather than standalone scale alone.

- Risk Management and Scenario Planning: Run downside scenarios that assume prolonged feedstock shortages or accelerated regulatory tightening. Develop contingency plans for alternative raw material supply and incremental capex options to maintain compliance without jeopardizing production.

How This Report Helps Your 2026 Playbook

PW Consulting’s industrial sodium nitrate study is structured as an executable toolkit rather than an academic exercise. Clients will find:

- Board‑ready slide decks and CFO‑grade financial models that translate market forecasts into EBITDA sensitivity under alternative feedstock, price and regulatory assumptions.

- Commercial playbooks with go‑to‑market options, pricing levers and contract templates for long‑term supply agreements.

- M&A diligence packs and synergy calculators that accelerate deal screening and valuation sign‑off.

- Operational checklists for environmental compliance investments and supplier audits to fast‑track implementation without surprises.

Why Accessing the Full Report Matters

This release is a strategic preview: it surfaces the insights necessary to align corporate priorities for 2026 while preserving the granular segmentation, geographic flows and application‑level detail that underpin investment and procurement decisions. The full report includes comprehensive segmentation, regional trade‑flow matrices, price‑by‑corridor tables, company-level capacity maps and scenario‑driven P&L projections — the precise inputs procurement leads, plant managers and corporate development teams need to move from strategy to execution.

For organizations deciding on capex, pursuing M&A, or refining procurement strategy in 2026, the difference between a good decision and a costly misstep will often be access to the segmentation and pricing granularity that underlies the high‑level trends summarized here. PW Consulting’s full study provides that granularity within a decision‑ready structure.

Next Steps

- Secure a briefing with our industry team to align the report’s scenarios to your balance sheet and risk tolerance.

- Commission a tailored deep‑dive (e.g., feedstock sensitivity stress test or regional logistics optimization) to convert insight into a measurable action plan for 2026.

- Download the full report to obtain the detailed segmentation tables, supplier scorecards and corridor pricing that inform executable commercial and capital strategies.

PW Consulting stands ready to support boards and executive teams as they translate the 2026 outlook for industrial sodium nitrate into confident, operationally realistic decisions. Contact our industry desk to schedule a tailored briefing and access the complete dataset and models that power our recommendations.

For detailed analysis of this topic, please visit the official page:Industrial Sodium Nitrate Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com