What Does a Mailing Company Do? Everything You Need to Know

Other |

2026-06-29 10:00:40

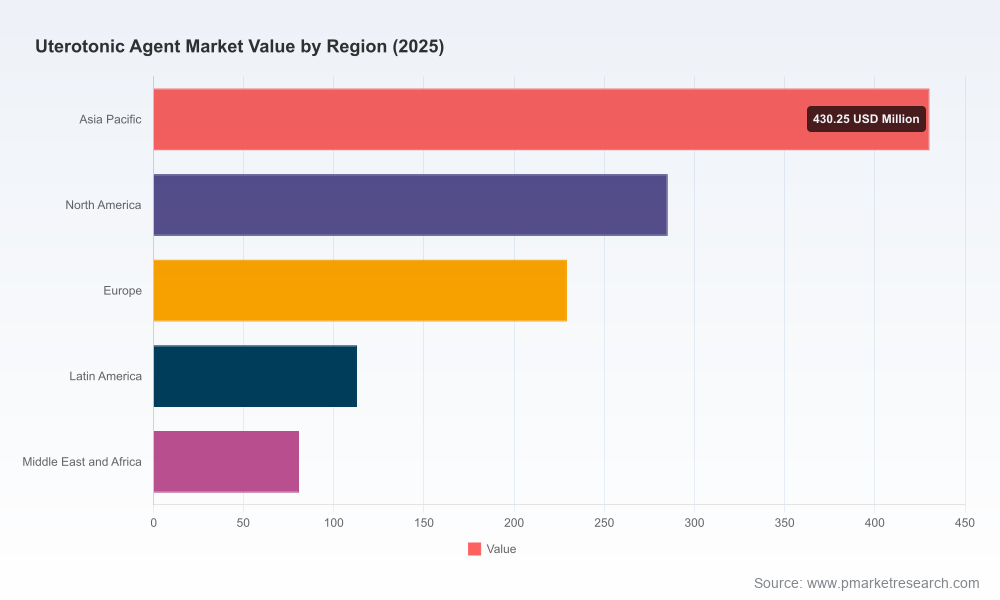

PW Consulting’s latest market research on uterotonic agents delivers a focused, decision-grade roadmap for life sciences executives, procurement leaders, and global health strategists preparing their 2026 plans. Built on a robust historical base (2020–2025) and an independent market model, the study quantifies a sustained expansion through the forecast window (2026–2032) and—more importantly—translates that growth into concrete strategic choices. With the global uterotonic market anchored at a 2025 base and projected to grow at a compound annual growth rate (CAGR) of 6.19% over 2026–2032, market value reaches the high‑single‑digit growth trajectory that will reshape supplier footprints, procurement dynamics, and product innovation priorities over the next planning cycle.

Uterotonic Agent Market

The uterotonic market has demonstrated steady expansion over the past half decade and enters 2026 from a position of renewed strategic relevance. Our model shows continuity of growth into the forecast period—driven by ongoing maternal health initiatives, shifts in procurement policy toward quality-assured products, and product-level innovation (notably heat-stable formulations). For executives and policy planners, the headline trajectory signals two realities: (1) absolute market opportunity is increasing across both public and private channels; and (2) the pace of change is sufficient that near-term tactical moves (supply‑chain investments, prequalification efforts, partnership agreements) will determine which suppliers capture the next wave of demand.

Uterotonic Agent Market

Prioritise quality‑assurance as a competitive moat. Donors and national procurers are increasingly using WHO prequalification and credible QA lists to de‑risk tenders. Manufacturers without validated quality credentials face exclusion or price‑only competition. The 2025 WHO prequalification of certain oxytocin injectables and the R4D Quality‑Assured Supplier List are early indicators; investors and manufacturers should accelerate quality investments (GMP upgrades, stability data packages, WHO PQ submissions).

Uterotonic Agent Market

Differentiate through formulation and cold‑chain strategy. Oxytocin’s cold‑chain requirements remain a systemic source of product failure in tropical climates. Heat‑stable alternatives (notably carbetocin) are now endorsed in key guidance as an alternative where cold chain is unreliable. Suppliers should evaluate product portfolios against last‑mile refrigeration realities: licensing or developing heat‑stable formulations, investing in stability data, and partnering with distribution networks that deliver reliable cold‑chain performance.

Make targeted partnerships to access public markets. The public procurement space increasingly rewards product availability, price, and documented quality. Licensing deals with originators, risk‑sharing arrangements with multilateral agencies, and local manufacturing partnerships are practical levers to accelerate access in priority markets without prohibitive upfront capex.

Use scenario planning to guard against pricing commoditisation. Procurement in low‑resource settings has historically prioritised lowest‑price oxytocin, producing quality failures. Our scenario work shows that a short‑sighted, price‑only approach can increase clinical risk and supply volatility. Suppliers and purchasers should model multi‑year procurement strategies that balance price, quality, and supply security; contract structures can include minimum quality thresholds, staggered volume commitments, and shared investment in cold‑chain improvements.

Local manufacturing and differentiated go‑to‑market models will matter. Local, WHO‑prequalified production can unlock procurement advantages in regional tenders, while international firms can leverage technology transfers and licensing to expand reach. For multinational players, a hybrid approach—direct supply for high‑margin channels and licensing/partnerships for public tenders—is a pragmatic route to scale.

Market model and forward‑looking base case plus alternative scenarios to 2032 (including demand shocks, policy shifts, and product substitution pathways).

Procurement and tender analysis covering major purchasing mechanisms, pricing benchmarks, and contract structures used by multilateral agencies and national ministries.

Regulatory and quality‑assurance playbook — WHO prequalification timelines, dossier requirements, and a practical checklist for GMP upgrades and stability programmes.

Supply‑chain diagnostics — cold‑chain risk heat maps, distribution bottleneck mitigation tactics, and sourcing strategies for active pharmaceutical ingredients.

Competitive positioning tools — vendor scorecards, capability matrices, and acquisition targets tailored to different strategic objectives (market access, product diversification, or capacity expansion).

Commercial and reimbursement guidance — payer behaviour, tender adjudication factors, and pricing strategies that reconcile donor procurement goals with commercial viability.

Operational playbooks — timelines and resource estimates for filing WHO PQ, strategies for securing local GMP approvals, and recommended KPIs for supply reliability and product quality.

Note: This executive preview highlights the strategic value of the analysis; the full report contains granular segmentation, regional breakouts, and company‑level financial estimates reserved for subscribers and purchasers of the complete dataset.

The market is served by a mix of multinational originators, large generic firms, and regional producers. PW Consulting’s competitive analysis evaluates these players across product portfolios, route‑to‑market, quality credentials, and partnership footprints. Key dynamics include strategic licensing of heat‑stable formulations, the enduring importance of oxytocin in clinical guidelines, and the competitive pressure from low‑cost generics in public tenders.

Innovator and branded players: Firms that have invested in differentiated products—such as heat‑stable carbetocin—are positioned to capture premium segments where quality and logistical resilience matter. Recent licensing frameworks and collaboration with multilateral programmes have catalysed access and expanded public‑sector adoption pathways.

Large generics and WHO‑prequalified suppliers: These companies dominate price‑sensitive procurement channels and are competing to convert safety‑conscious buyers by gaining or publicising prequalification status. Their scale provides supply reliability, but they must continually demonstrate quality to avoid being outcompeted on performance rather than price.

Regional manufacturers: Local producers reduce lead times and can be advantaged in certain national procurement frameworks. Their strategic importance grows when export‑oriented tendering prioritises local content or when cold‑chain gaps favour near‑site supply.

Market concentration metrics indicate a moderately concentrated market structure, where the top three and top five firms collectively command a meaningful share of the market. This creates space for both scale advantage and tactical differentiation—the latter particularly relevant where product quality and formulation advantages (e.g., heat stability) are decisive.

Guidance and essential medicines policy: WHO continues to set practice norms (e.g., recommending oxytocin as first‑line, with heat‑stable carbetocin as an alternative where cold chain is not assured). These endorsements materially affect procurement criteria and can rapidly shift demand toward quality‑assured alternatives.

Quality risk in low‑resource environments: Persistent evidence of oxytocin potency degradation in unrefrigerated supply chains has driven procurement reappraisals. Organisations prioritising clinical outcomes are increasingly willing to pay a premium for validated products and supply‑chain assurance.

Recent developments that matter: WHO prequalification updates and public supplier lists have immediate procurement impact. Licensing agreements and technology transfer partnerships that expand access to heat‑stable formats are strategic inflection points for 2026 planning.

Use the report’s scenario outputs to set procurement commitments and manufacturing cadence for the next 18–36 months.

Prioritise WHO PQ and similar quality credentials where access to public tenders is a strategic priority—accelerating these programmes can be a make‑or‑break decision in 2026 solicitations.

Design pilot programmes that test heat‑stable formulations in high‑risk districts and quantify cost of quality‑failures (clinical and economic). Results will inform national policy updates and donor funding criteria.

Negotiate flexible tender terms that reward documented quality and supply reliability, not just lowest unit price; structure multi‑year agreements with escalation clauses tied to quality metrics.

For decision‑makers preparing 2026 budgets and market entries, PW Consulting’s uterotonic market analysis converts headline growth into actionable playbooks: where to invest in quality, how to structure partnerships, and which operational changes unlock near‑term competitive advantages. The market’s steady growth, combined with rising emphasis on quality and formulation attributes, creates a window for both incumbents and new entrants to reshape maternal health outcomes while securing commercial returns.

To access the complete market model, regional and application segmentations, and company scorecards that underpin the strategic recommendations above, please consult the full PW Consulting report and our supplementary datasets—designed to support procurement negotiations, M&A diligence, and commercial planning for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Uterotonic Agent Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com