Africa Tobacco Products Market Opportunity Analysis

Other |

2026-05-22 09:38:14

PW Consulting’s latest Soy Milk Market briefing synthesizes market-scale verification, competitive momentum, input-cost dynamics and on-the-ground go-to-market playbooks that will determine who wins and who is repositioning in 2026. Our independent model shows the global soy milk market reached roughly USD 11.7 billion in 2025 and — at a compound annual growth rate (CAGR) of 6.02% across the 2026–2032 forecast window — trajectories point to sustained expansion through the end of the decade. This release is designed as a strategic preview: we disclose the directional implications and decision levers, while detailed segment tables, SKU-level forecasts and proprietary company share matrices are reserved for the full report on our site.

Soy Milk Market

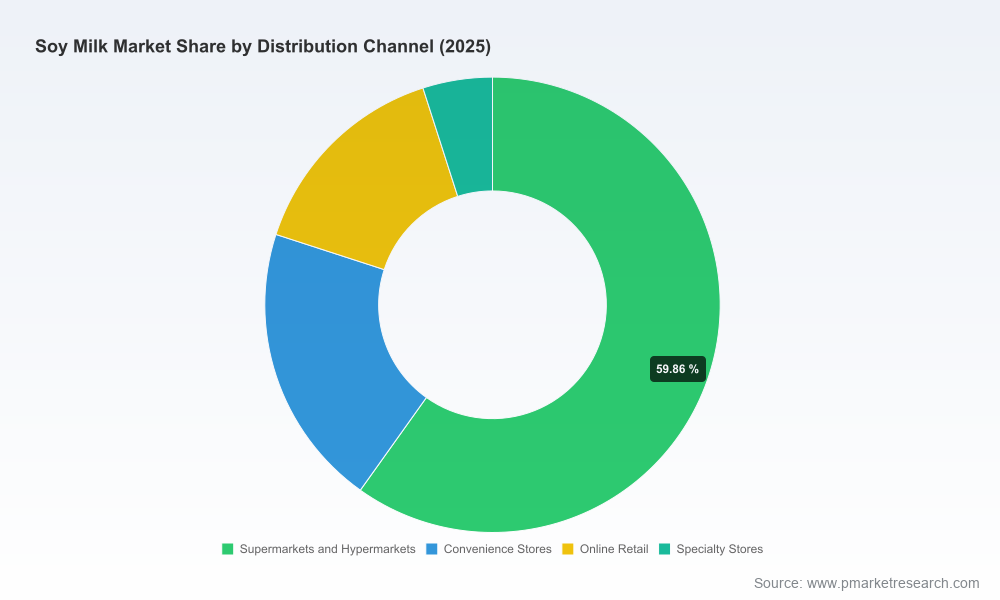

Demand growth is broad-based but nuanced. Macroeconomic momentum and plant-based diet trends continue to underpin volume gains, while product innovation (high-protein formulations, clean-label minimal-ingredient lines, and region-specific flavor iterations) is shifting where and how value is captured within shelf space.

Soy Milk Market

Input-cost volatility is resurfacing as a central margin risk. The USDA revised the 2025/26 U.S. soybean season-average price higher — a sign that crush demand and competing oilfeedstock dynamics are tightening raw-material availability — while global soybean output has only inched higher year-on-year. Simultaneously, FAO vegetable oil indices have shown upward pressure influenced by biofuel expectations. Producers that lack active procurement hedging or alternative sourcing strategies will see compressing margins absent price realization strategies.

Soy Milk Market

Competitive structure remains moderately fragmented: the top three players account for a low-to-mid-thirty percent share and the top five under 50 percent. That structure creates both room for scale plays and opportunities for specialized brands to capture premium niches.

Proprietary market model covering 2020–2025 historicals and 2026–2032 forecasts with scenario toggles for input-cost shocks, premiumization adoption and channel substitution.

Actionable SKU and channel optimization playbooks: SKU rationalization matrices, promotional elasticity benchmarks, and a prioritized list of channel investment opportunities for 12-month to 36-month horizons.

Procurement and sourcing playbook: hedging triggers, alternative soybean sourcing routes, supplier concentration heatmaps and cost-to-serve implications for different packaging and shelf-stability strategies.

Innovation and NPD sprint templates: use-cases, protein positioning frameworks, and co-manufacturing selection criteria to accelerate time-to-shelf while protecting margin.

M&A and partnership scorecards: target archetypes, financial criteria, integration risks and a short-list of putative targets across branded, co-manufacturing and ingredient specialists.

Regulatory and labeling risk assessment, including trade-policy scenarios, sustainability traceability templates and consumer-claims risk matrices.

Danone S.A. (Silk, Alpro) — Global scale and multi-brand reach are Danone’s structural advantages. Their recent launch of higher-protein refrigerated plant milks demonstrates a deliberate push up the value curve. For rivals, the imperative is clear: either neutralize via competing formulations or double down on channels and formats where scale advantages are weaker (e.g., regional flavors, foodservice or private label).

Vitasoy International — Deep regional roots in Asia and breadth across retail/foodservice make Vitasoy the local challenger to watch. Their entrenched distribution and flavor adaptation capability underscores how market incumbency can defend share even as global players expand in the region.

Kikkoman Corporation — The company is capitalizing on health-awareness messaging and smaller-format usage occasions. Their sales uptick in unprocessed and single-serve lines signals an opportunity for competitors to explore similarly targeted formats for commuting and on-the-go consumption.

Specialist & Organic Players (Eden Foods, Pacific Foods, SunOpta, The Hain Celestial Group, Organic Valley, WestSoy, MALK, Califia Farms) — These brands function as the innovation vanguard and premium doorsill. Clean-label launches and high-protein recipes are repositioning consumer expectations. The strategic choice for mainstream manufacturers is a two-track approach: protect core volume with scale economics and selectively incubate premium/clean-label sub-brands to defend against erosion.

Private-label and co-manufacturers — There remains sizable room for private-label expansion, especially where retailers can aggregate scale and control sourcing. Firms should evaluate margin trade-offs between contract manufacturing investments versus retail partnership agreements.

Product launches: Several notable high-protein and minimal-ingredient soy milk products have debuted in early 2026, highlighting mainstreaming of premium claims and a widening of the competitive set beyond traditional dairy-alternative specialists.

Regional product modernization: New brands entering Southeast Asian markets with simplified formulations indicate a modernization wave of classic soy beverages, raising the bar for local incumbents.

Sales performance: Public reporting from established producers shows sustained growth in smaller-format and health-positioned SKUs, underlining the consumption shift from purely value-driven purchases to health- and occasion-driven choices.

Raw-material pricing pressure is real: U.S. soybean season-average price forecasts were revised upward in 2025/26, reflecting strong crush demand. At the same time, global soybean production growth has been marginal — a combination that increases the probability of periodic price spikes.

Vegetable oil markets are affecting margins indirectly. A rise in broad vegetable oil indices, influenced by biofuel demand expectations, makes integrated commodity price scenarios an essential stress-test for any commercial plan.

Strategic responses should include a mix of forward-coverage, supplier diversification (different origin mixes), and product design that allows short-term input-cost pass-through without devaluing brand equity.

Prioritize channel-specific SKUs: Use the next 12 months to optimize portfolio and promotional investments by channel. High-velocity convenience and on-the-go formats require different cost structures and margin targets than bulk supermarket SKUs.

Launch calibrated premium innovations: High-protein and clean-label propositions are translating into measurable price premiums. Pilot in high-affluence urban corridors and roll by performance cohorts.

Hedge and diversify soybean sourcing: Implement layered procurement strategies combining short-term hedges with longer-term supplier contracts and origin diversification to dampen volatility.

Build a private-label / co-manufacturing capability: For manufacturers with excess capacity, targeted private-label partnerships can offset fixed-cost exposure and deepen retail relationships.

Invest in traceability and sustainability claims: As consumer discrimination increases, investments in transparent supply chains and sustainability certifications will be durable share protectors and can justify price premiums.

Use M&A tactically: Prioritize acquisitions that add capability (protein tech, UHT lines, regional footprint) rather than incremental volume. Integration readiness and SKU rationalization must be part of diligence.

For executives making allocation and portfolio decisions in 2026, our Soy Milk Market report functions as a decision intelligence kit: it combines a validated market-size baseline, a scenario-enabled forecast engine, competitor playbooks and procurement stress-tests. The evidence is clear — growth persists, but the pathways to profitable growth are becoming more complex as input prices, premiumization and channel dynamics interplay.

PW Consulting’s full report provides the granular forecasts, regional and channel splits, SKU-level demand curves and a company share database needed to operationalize the recommendations above. If your 2026 plan includes new product launches, portfolio rationalization, procurement hedges, or inorganic growth, this is the working document you should base those decisions on. Visit our research portal to access the complete dataset and modelling tools.

For detailed analysis of this topic, please visit the official page:Soy Milk Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com