Global Synthetic Feed Antioxidants to Hit USD 2.18 Billion by 2032 at 5.7% CAGR

Other |

2026-06-04 09:09:40

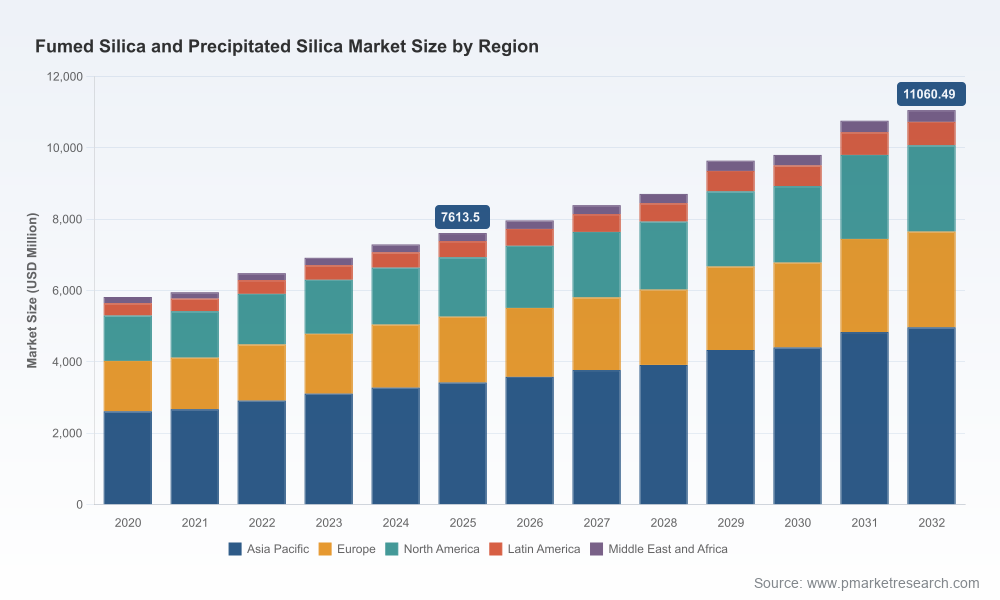

The global market for synthetic amorphous silica — encompassing both fumed (pyrogenic) and precipitated grades — has entered a phase of steady, structurally-driven expansion. PW Consulting’s latest market model places the industry at approximately USD 7.6 billion in 2025, growing at a compound annual growth rate (CAGR) of about 5.5% through our 2026–2032 forecast horizon and reaching roughly USD 11.1 billion by 2032. That trajectory masks important inflection points for producers, OEMs, suppliers of feedstock and capital allocators: pricing volatility in upstream inputs, regulatory reclassification risk, and accelerated premiumization around low‑carbon and specialty grades create a very different competitive landscape than five years ago.

Fumed Silica And Precipitated Silica Market

Investment timing: capital projects announced or commissioned in 2026 will influence global balance through the late 2020s. Our modelling identifies windows where new capacity shifts prices and margins materially — strategic investors need to align greenfield/brownfield timelines to avoid value dilution.

Fumed Silica And Precipitated Silica Market

Procurement & security of supply: trade measures and regional policy actions in 2025 changed import dynamics for several markets. Buyers who revise sourcing strategy in 2026 can capture cost and service advantages across multi‑year contracts.

Fumed Silica And Precipitated Silica Market

Product portfolio strategy: demand for higher‑value, performance‑oriented silicas (e.g., for green‑tire, battery, electronics and specialty silicones) is expanding faster than commodity segments. Understanding the margin spread and qualification timelines is essential for prioritizing R&D and sales investments.

End‑market pull is diversifying. Traditional rubber and tire demand remains foundational, but coatings, adhesives, electronics, pharma and oral‑care are driving incremental, higher‑margin demand. This mix increases the value of product differentiation and application know‑how relative to scale alone.

Upstream feedstock cost and availability: sodium silicate — the primary precursor for precipitated silica — traded in a narrow band in early 2026, reflecting regional raw material and energy pressures. Silicon tetrachloride, the key intermediate in fumed silica manufacture, is itself on an expansion trajectory (a market that grew into hundreds of millions USD in 2024 and forecasts show strong growth to 2032), driven by polysilicon and optical fiber demand. These inputs create both cost pass‑through and sourcing risk for manufacturers.

Regulatory and handling considerations. Synthetic amorphous silica remains distinct from crystalline phases under current CLP frameworks; however, industry attention to STOT RE 1 labelling for certain forms is reshaping product stewardship and supply chain documentation. Companies that pre‑emptively adapt packaging, training, and documentation will reduce friction in multinational sales.

Trade policy and regional realignment. Tariff measures enacted in 2025 altered trade flows and pushed several buyers to reassess dependence on imports. The immediate effect was price dispersion across regions and accelerated local investment conversations in tariff‑exposed markets.

Consolidation and strategic transactions. Recent deal activity and capacity moves are not just incremental — they are re‑shaping competitive footprints and customer convergence points (see Competitive Landscape section below).

The market exhibits moderate concentration: the top three suppliers collectively control just under 40% of global capacity, while the five largest participants account for roughly half the market. That structure supports both regional leadership strategies and niche specialization — an environment where scale matters for feedstock integration and logistics, but technical differentiation unlocks premium margins.

Evonik Industries AG — a global leader across both fumed (AEROSIL®) and precipitated (ULTRASIL®, SIPERNAT®) portfolios — is leveraging integrated feedstock and multi‑continent production to pursue both scale and sustainability. Its 2024 decision to expand precipitated silica capacity in Charleston with circular raw materials is a clear strategic bet on sustainable ‘green tire’ demand.

Cabot Corporation and its regional JV structures retain strong fumed silica capabilities across major geographies. Near‑term brownfield investments being executed in 2026 target higher‑growth local end markets including pharma and semiconductor sectors.

Wacker, Tokuyama, OCI and other established pyrogenic silica players compete on high‑purity grades and specialty applications where qualification cycles are lengthy but margins are attractive.

QEMETICA’s acquisition of PPG’s precipitated silica business in late 2024 reshuffled regional footprints and strengthened its position in tires and battery fillers. That transaction exemplifies the type of strategic consolidation we expect to continue where incumbents seek scale in key regions.

Regional manufacturers across Asia — from Tata Chemicals to several specialized producers in India, China and Taiwan — provide lower‑cost supply and nimble product development. Their role is increasingly important for global buyers seeking cost diversification or local market resilience.

For industrial producers: prioritize a twin track of capacity and capability. Brownfield debottlenecking and selective greenfield capacity should be paired with investments in specialty R&D (surface treatments, HDS grades, hydrophobic silicas) and sustainability certifications. Hedging strategies for sodium silicate and silicon tetrachloride exposure — including long‑term supply agreements with chemical producers and vertical integration where feasible — will materially stabilize margins.

For OEMs and formulators: accelerate supplier qualification and dual‑sourcing strategies now. Longer lead times for specialty grades and increasing regional trade complexity mean procurement cycles started in 2026 will determine 2027–2028 continuity. Invest in collaborative development agreements to lock in tailored grades and price stability.

For private equity and strategic investors: look beyond headline multiples. Targets with strong technical service capabilities, proprietary specialty grades and regional logistics advantages command higher risk‑adjusted returns than pure commodity players. M&A playbooks should include integration of regulatory compliance systems and talent retention plans for R&D teams.

For policymakers and industry bodies: supply chain visibility and skills development are critical. Tariff‑induced disruptions in 2025 highlighted national vulnerabilities — targeted programmes that lower barriers to local investment and upskill process engineers will pay dividends in resilience.

We have structured the report to be operationally useful for executive teams and investors who must make decisions in 2026. Key deliverables include:

Dynamic market model: a scenario‑based demand and pricing engine calibrated to 2020–2025 data and sensitive to feedstock cost trajectories, regulatory shocks and tariff scenarios. (Note: detailed sub‑segment tables and region/application splits are available in the full dataset.)

Cost benchmarking and margin maps: plant‑level cost stacks for typical fumed and precipitated silica facilities, including raw material, energy, labour and logistics components — with sensitivity analyses for sodium silicate and silicon tetrachloride movements.

Capex prioritization and ROI toolkits: stepwise investment plans for brownfield expansions versus greenfield projects, with commissioning timelines aligned to demand windows where price uplift is likely.

M&A and integration playbook: target screening criteria, valuation heuristics for specialty versus commodity assets, and a 90‑day integration checklist focused on R&D, regulatory compliance and customer retention.

Procurement playbook for buyers: contracting templates, qualification roadmaps, and inventory strategies to mitigate trade and tariff‑induced delivery risks.

Regulatory & sustainability roadmap: compliance gap assessment tools for CLP/STOT considerations and a decarbonisation checklist for converting legacy product lines to low‑carbon feedstock alternatives.

Monitor feedstock indices and secure rolling supply agreements where possible — the next two quarters will set procurement cost baselines for 2027 contracting cycles.

Review qualification timelines for specialty grades with key OEM customers; fast‑track at least one collaborative development to lock in commercial terms.

Assess the competitive impact of announced capacity projects; recent expansions by major producers and regional brownfield announcements will crystallize regional pricing differentials by late 2027.

Embed regulatory readiness into commercial contracts — STOT labelling and cross‑border documentation requirements must be operationalised to avoid transactional friction.

PW Consulting’s analysis is intentionally pragmatic: we surface the strategic inflection points and provide executable frameworks while reserving detailed segment tables and plant‑level forecasts for the full report. If your 2026 planning cycle includes capital allocation, procurement strategy, or M&A activity in the synthetic silica value chain, the full dataset and scenario models will supply the actionable granular intelligence you need to turn foresight into advantage.

To request the complete report, dataset access, or a tailored executive briefing that maps our findings to your portfolio, visit the report page or contact PW Consulting’s industry practice leads for a confidential briefing.

For detailed analysis of this topic, please visit the official page:Fumed Silica And Precipitated Silica Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com