Soy Based Infant Formula Market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-06-04 10:51:55

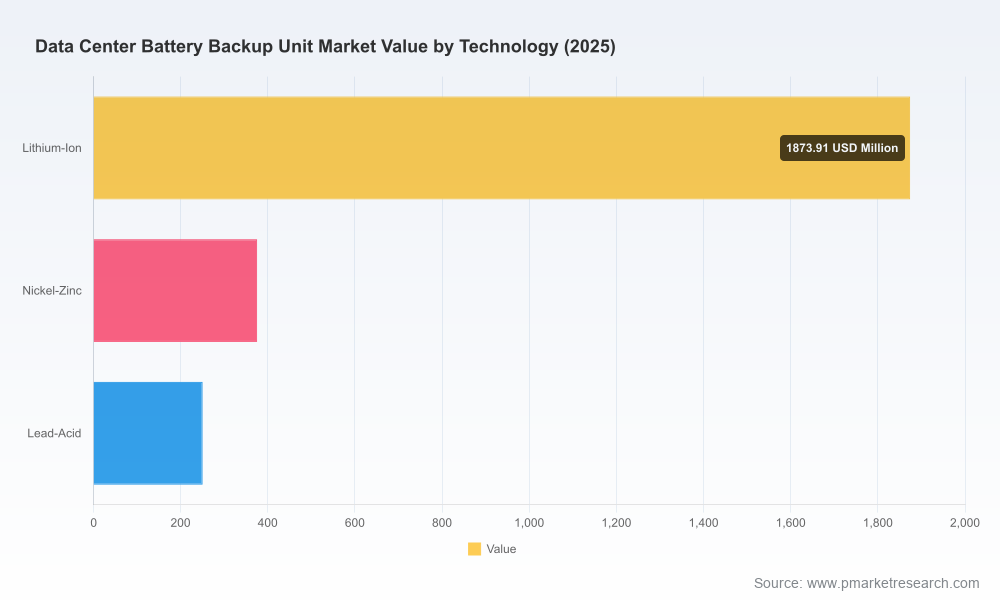

PW Consulting's new market study on Data Center Battery Backup Units (base year 2025) offers a compact, decision‑focused playbook for technology, procurement, and infrastructure leaders planning capital and operational choices in 2026. The market we modeled has grown from a multi‑year baseline and reached a 2025 size of USD 2,500 Million (million USD basis). Under a central forecast case the sector expands at a compound annual growth rate (CAGR) of 8.15% through our forecast window (2026–2032), with total market value approaching roughly USD 4.33 Billion by 2032 under the baseline scenario. These top‑line dynamics make 2026 a pivotal year for reshaping architecture, supplier relationships, and total cost profiles.

Data Center Battery Backup Unit Market

Executive decision frameworks — prioritized checklists for technology selection (lead‑acid, lithium variants, emerging chemistries), procurement timing, and total cost of ownership (TCO) tradeoffs tied to real project archetypes.

Data Center Battery Backup Unit Market

Supply‑chain heatmap and risk register — practical steps to mitigate component concentration, tariff exposure, and long lead items that affect deployment schedules.

Data Center Battery Backup Unit Market

Vendor scorecards and go‑to‑market playbooks — comparative supplier assessments built around serviceability, modularity, warranty economics, and retrofit readiness (designed to accelerate vendor shortlisting).

Technology adoption playbook — staged migration paths for integrating higher energy‑density cells (with pilot templates for rack‑level demonstrations), and guidance on when to retain proven lead‑acid platforms.

Scenario modeling tools — stress tests for AI load growth, multi‑site redundancy strategies, and regulatory/tariff shock scenarios that quantify timing and magnitude of capital and operating impacts.

Procurement templates and contract clauses — practical language to reduce vendor lock‑in, secure spares, and embed performance guarantees linked to lifecycle metrics.

Three interlocking macro trends will determine winners and losers in the coming 18–36 months:

Material and supply concentration. Recent analyses underscore heavy geographic concentration in battery cell inputs, notably cathode and precursor production that underpin common LFP‑based data center cells. This concentration drives policy and commercial actions — from near‑term spot price volatility to strategic import controls and reshoring conversations — and it should be treated as a planning assumption when setting inventory and procurement cadence.

Cost trajectory and installed system economics. Market data for 2026 shows a range for data center‑grade LFP cell pricing and installed BESS capital costs that makes lifecycle economics highly sensitive to cycle life, rack footprint, and balance‑of‑system integration. Evaluating pure capital cost per kWh is necessary but insufficient; owners must model value streams such as reduced footprint, faster recharge, and potential grid services.

Regulatory and policy pressure. Elevated tariffs and evolving trade policy have already altered sourcing strategies. Simultaneously, grid interconnection constraints and extended procurement lead times for large electrical equipment (transformers, switchgear) are changing project schedules and raising the premium on early supplier engagement.

The sector remains moderately consolidated: the top three and top five suppliers capture meaningful but far from monopolistic shares of market activity. That structure creates room for differentiated plays — service specialization, chemistry leadership, system integration, or channel excellence.

EnerSys — plays to its strengths in robust, high‑temperature lead‑acid platforms optimized for long life and grid‑support duties. Their recent market commentary highlights strong demand for traditional battery technologies even as they pilot lithium trials, indicating a pragmatic dual‑track strategy. For buyers, EnerSys represents a low‑risk option where maturity and service coverage are prioritized.

C&D Technologies — leverages deep VRLA and pure‑lead AGM experience to serve hyperscale, colocation, and enterprise clients. The company's century‑plus legacy in stationary power is being repackaged as reliability and installability advantages for teams debating retrofit vs replace decisions.

Saft — positions as a turnkey lithium systems supplier capable of scaling to large MW projects. Their value proposition centers on integration — coupling cells, power electronics, and project delivery for owners seeking single‑vendor responsibility for larger energy storage projects.

Schneider Electric and Eaton — both emphasize modular UPS platforms with integrated lithium options. The strategic question for customers is whether to prioritize integrated UPS/battery solutions (simpler lifecycle management) or maintain open selection to optimize cell economics independently.

Vertiv, Mitsubishi Electric, and ABB — differentiate on system architecture, service networks, and on‑ramp features for AI‑ready deployments (including cooling and higher‑density rack compatibility). Recent collaborations and product announcements reflect a focus on liquid cooling, rack‑scale UPS, and co‑engineering with compute vendors.

Recent industry developments reinforce these themes: new silicon‑carbon anode systems designed to reduce rack footprint, liquid‑cooled rack UPS collaborations aimed at AI platforms, and supplier disclosures highlighting persistent demand for legacy chemistries even as trials of newer batteries proceed. Taken together, these moves signal a market that will evolve through incremental replacement and selective greenfield adoption rather than a single‑step chemistry flip.

Procurement cadence matters. With long lead items and tariff volatility, buyers should move from single‑year sourcing to rolling 18–36 month procurement plans. Locking options (not just prices) and staged acceptance milestones will materially reduce schedule risk.

Differentiate by application. Not every use case benefits from the newest chemistry. Use a segmentation of mission criticality, density constraints, and grid‑service value to determine where to pilot lithium solutions versus where to retain mature lead‑acid approaches.

Insist on lifecycle metrics. Contracting should move beyond nominal capacity to measurable lifecycle outcomes (cycle count, degradation curve, service turn time). Require shared KPIs and financial penalties that align supplier incentives with long‑term reliability.

Use pilots to derisk AI workloads. For facilities hosting high‑density AI racks, run controlled pilots of rack‑level UPS and liquid‑cooled battery systems to validate integration, cooling interactions, and maintenance regimes before campus‑wide rollouts.

Invest in supply base diversity and locality. Where policy and supply concentration pose risks, diversify cell and pack suppliers and evaluate regional assembly partners to reduce tariff and logistics exposure.

Embed grid services in planning. Evaluate whether batteries can be aggregated for grid services or demand response to create secondary revenue streams — and design procurement to preserve that optionality.

This study is constructed as an execution toolkit rather than an academic exercise. For a 2026 planning cycle we deliver:

Actionable TCO models pre‑populated with vendor and installed‑cost bands that you can reparameterize for your sites and tariffs.

Supplier scorecards that translate technical attributes into procurement language and contractual clauses you can use in RFIs/RFPs.

Scenario playbooks that quantify how tariff shocks, cell price moves, or supply chain delay cascades affect delivery and lifecycle economics.

Implementation roadmaps tailor‑made for retrofit and greenfield projects, including sample pilot scopes and acceptance tests for battery packs and UPS integration.

If your 2026 capital planning or procurement cycle touches battery backup, the report provides the evidence base and playbook needed to make robust choices under uncertainty. We deliberately present macro market sizing and structured scenario outcomes here to ground strategic judgment while reserving granular regional, application, and segment breakouts for the full report. Those details — including supplier shares by subsegment, capacity band economics, and region‑level sensitivity analyses — are available in the complete dataset and downloadable models on PW Consulting’s report page.

Decisions made in 2026 will determine not only cost and uptime for the next five years but also flexibility to respond to accelerating compute density and evolving policy regimes. With a market that has expanded to USD 2.5 Billion in 2025 and a clear upward trajectory, practical, risk‑aware strategies will reap outsized operational and financial returns. PW Consulting’s Data Center Battery Backup Unit Market report is designed to be the operational backbone for those strategies.

For detailed analysis of this topic, please visit the official page:Data Center Battery Backup Unit Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com