The Rise of Advanced Technologies in the US Pneumatic Components Market

Other |

2026-06-11 08:20:13

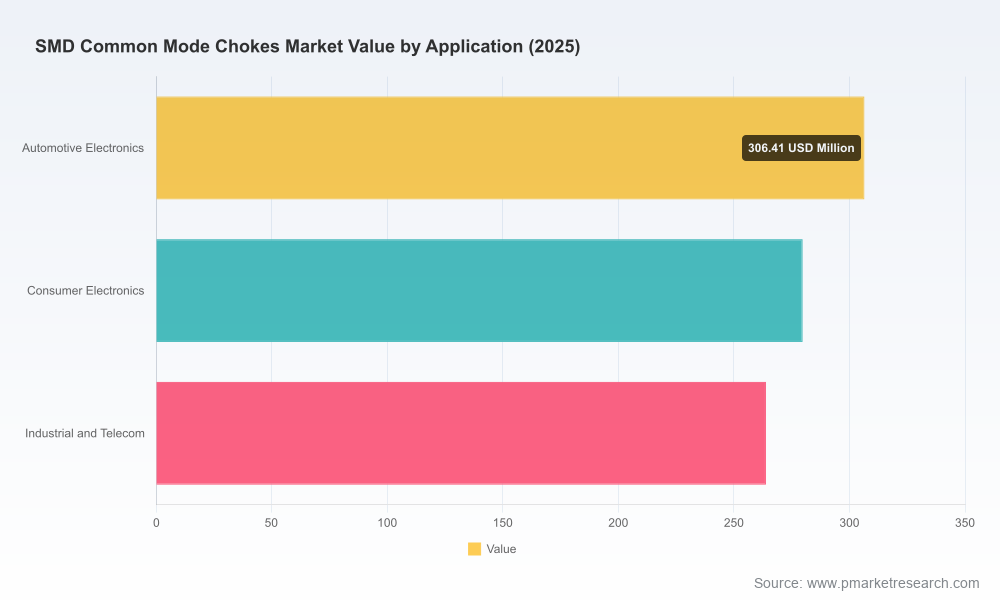

PW Consulting’s new market research brief on SMD common mode chokes delivers a concise, practitioner-focused intelligence package designed to inform board-level and operational decisions in 2026. Anchored to a 2025 base year and projecting through 2032, the analysis synthesizes historical performance (2020–2025) and forward-looking scenarios that reflect competitive shifts, raw-material volatility, and accelerating end-market demand. The market shows clear momentum: total industry revenue rose from approximately USD 620 million in 2020 to roughly USD 850 million in 2025, and under a central-case trajectory (CAGR ~6.5%) is expected to cross the USD 1.3 billion mark by the early 2030s. These high‑level trajectories matter for capital allocation, product roadmaps, and supply‑chain resilience planning in 2026.

Smd Common Mode Chokes Market

Three converging dynamics make 2026 a pivotal year for players and buyers of SMD common mode chokes. First, electrification and high‑power electronics trends are increasing nominal demand for high‑current SMD solutions, while system‑level EMC requirements are tightening across automotive, telecom and industrial segments. Second, supplier structures and raw‑material cycles are creating asymmetric risk: ferrite and specialty core supply dynamics, together with copper price swings, mean input‑cost volatility and episodic lead‑time extensions that ripple into product availability. Third, pace of innovation — including nanocrystalline cores and compact high‑current topologies — is altering the specifications buyers prioritize when balancing cost, size and thermal performance.

Smd Common Mode Chokes Market

For executives setting 2026 budgets or negotiating multi‑year supply agreements, the implication is simple: act from a scenario perspective. Locking in EOL components or one‑off BOM designs without supply‑chain hedges may be costly; conversely, selective investment in validated next‑generation choke designs can secure a competitive advantage as system integrators demand higher current density and lower EMI footprints.

Smd Common Mode Chokes Market

Each deliverable is designed for immediate deployment in boardrooms, design sprints and procurement negotiation cycles. The goal is to convert market insight into executable programs within a 6–12 month horizon.

The market combines a mix of global conglomerates, specialized magnetics houses and regionally strong suppliers. Several profiles highlight where to direct strategic attention:

Notably, recent product activity (for example, TDK’s high‑current SurfIND launch in January 2025 and YAGEO’s May 2025 ER19‑core product) confirms an industry pivot toward higher‑current, reflow‑capable SMD solutions. That pivot is both a response to end‑system requirements and a battleground for supplier differentiation.

Boards, supply‑chain leads and product teams will find immediate utility in three use cases. First, negotiate supplier agreements with confidence: use the report’s supplier scorecards and cost‑sensitivity models to underpin term sheets and price floors. Second, prioritize R&D and NPI funding: the product roadmap templates help translate market demand into concrete electrical and mechanical targets. Third, refine M&A and strategic partnership pipelines using the report’s consolidation scenarios and capability heatmap to spot pockets where integration delivers rapid scale or capability improvements.

We purposefully present high‑level market sizing and concentration context in this release to support strategic thinking, while reserving the full segmented forecasts, supplier matrices, and SKU‑level market shares for the full report. That granular intelligence — including breakouts by type, application and geography, and the detailed vendor benchmarking — is essential to finalize supplier selection, design targets and capital allocation decisions.

PW Consulting’s SMD Common Mode Chokes Market report is structured to be operational from day one: downloadable models, M&A heatmaps and procurement playbooks are delivered alongside the narrative. For executives preparing 2026 budgets or operational plans, the report functions as both a strategic primer and an execution kit. To access the complete dataset, segmented forecasts, and the supplier scorecards that drive contract and design choices, please refer to the full report on the PW Consulting publication page.

For detailed analysis of this topic, please visit the official page:Smd Common Mode Chokes Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com