Wellhead Equipment Market Demand: Driving Efficiency in Modern Oil and Gas Extraction

Drinks |

2026-03-31 05:42:24

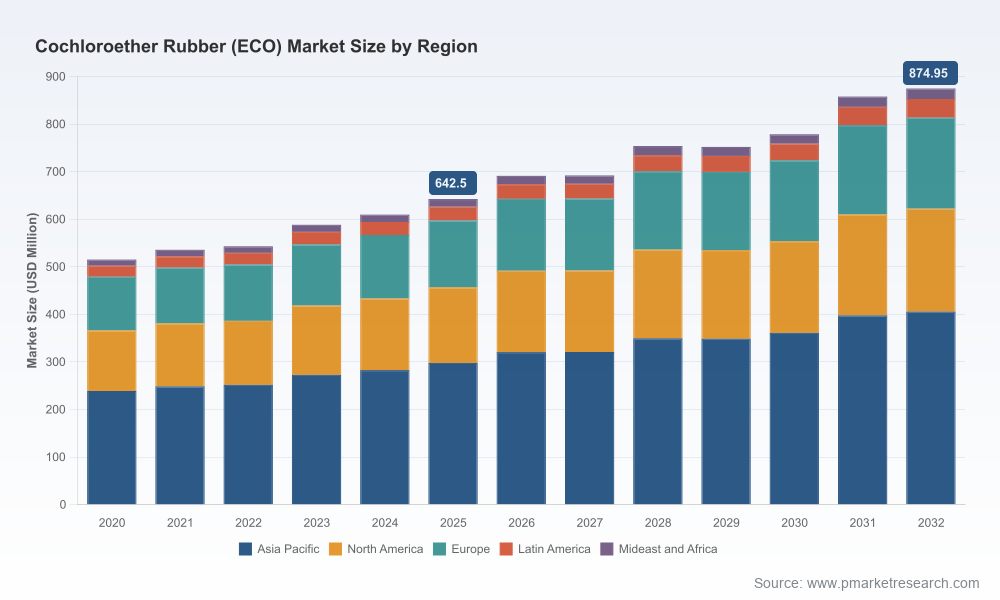

PW Consulting’s latest market research on the Cochloroether (ECO) rubber market lays out a concise, decision-ready view of an industrial elastomer class that will shape supplier strategies, product roadmaps, and sourcing decisions in 2026. Anchored on a 2025 base year and a forecast horizon through 2032, the study shows a steady, mid-single-digit expansion of the total market (2025 market: USD 642.5 Million; projected compound annual growth rate 2026–2032: 4.51%), with aggregate revenue growth continuing into the late 2020s. This briefing summarizes the report’s strategic implications while reserving the detailed segment tables and proprietary datasets for subscribers and the full report page.

Cochloroether Rubber Eco Market

Procurement leaders need forward-looking visibility on epichlorohydrin availability and supplier concentration to negotiate contracts and avoid supply interruptions.

Cochloroether Rubber Eco Market

Product teams must prioritize formulation choices (homopolymer / copolymer / terpolymer pathways and ETU-free cure systems) that align with tightening automotive, industrial, and aerospace specifications.

Cochloroether Rubber Eco Market

M&A and corporate development teams require a clear map of market concentration and where value can be captured via bolt-on capacity or technology partnerships.

Sustainability officers must understand how bio-based epichlorohydrin routes and lead/ETU-free compound options affect scope-3 emissions and compliance frameworks.

The ECO rubber market is mature but not static. After consistent expansion through 2020–2025, the sector enters a steady-growth phase across 2026–2032. PW Consulting’s base-case forecast uses a 4.51% CAGR for the period, reflecting a balance of durable demand from mobility and industrial sealing markets against cyclical pressures in capital goods and print technologies. Our model projects a progressive rise in aggregate market revenue through 2032, underpinned by replacement demand, regulatory-driven reformulations, and incremental adoption in specialty end-markets.

Key inflection points to watch in 2026 are twofold: first, upstream epichlorohydrin capacity dynamics and second, regulatory and specification shifts that favor ETU-free and lead-free curing systems. Recent industry information highlights that global epichlorohydrin production capacity reached approximately 2.385 million tons in 2025 with production near 1.37 million tons; significant new capacity additions in 2024 and 2025—targeting cleaner glycerol-based routes—are changing feedstock sourcing dynamics. These upstream moves materially affect cost curves and supplier bargaining power.

The market’s supplier structure is relatively concentrated: the top three producers control a material majority of supply, and the top five are dominant market-makers. This concentration delivers both stability and single-source risk. A clustered supplier base supports scale efficiencies and integrated-grade continuity but raises vulnerability to price actions, capacity outages, or strategic pricing decisions—evidenced by price adjustments announced by major manufacturers in recent cycles. Strategic procurement in 2026 should therefore factor in counterparty risk, tiered contracting, and contingency sourcing strategies.

Concentration snapshot: CR3 indicates a majority share positioning among leading producers; CR5 further underlines a high share captured by the upper quintile of suppliers.

Recent pricing signals: notable supplier price adjustments underscore the pass-through potential of upstream cost shifts to downstream elastomer pricing; these moves are tactical triggers for renegotiation and hedging discussions.

PW Consulting’s competitive review focuses on established, vertically integrated manufacturers and specialized compounders that serve automotive, industrial, and specialty applications. The following firms exemplify the strategic archetypes current in the market:

Osaka Soda Co., Ltd. (Japan) — A vertically integrated producer with global scale in epichlorohydrin-derived rubber grades. Their fully integrated process from epichlorohydrin monomer to finished elastomer provides resilience and margin control. Recent commercial actions include upstream price revisions that reflect feedstock pass-through dynamics.

Mitsui Plastics, Inc. (Japan) — Long-tenured supplier, notable for high-purity grades and customizable formulations. The company’s established line and flexible production footprint make it a go-to for OEMs requiring certified materials for seals and fuel-system components.

Zeon Corporation (Zeon Chemicals) (Japan / U.S. production for certain lines) — Offers distinct commercial positioning via Hydrin® elastomers, with emphasis on temperature performance and application-specific grades produced in localized facilities for key markets.

BRP Manufacturing (U.S.) — A US-based compounder focusing on application-ready ECO compounds certified to industrial standards. Their strength is in tailored compound formulations and ASTM-grade compliance for mobility and industrial clients.

RADO Gummi GmbH (Germany) — Differentiates with lead-free and ETU-free curing systems and extended storage stability for automotive hoses and technical parts—attributes that accelerate adoption where regulatory pressures or OEM requirements prohibit older cure chemistries.

Each of these suppliers plays a different role in customers’ go-to-market and risk management strategies: consolidated upstream producers provide supply security and integrated grade continuity; specialized compounders deliver application tuning and regulatory-compliant formulations.

Procurement and supply security: Establish layered contracts (shorter-volume commitments with price collars plus long-term supply agreements) with at least two integrated producers. Consider capacity reservation clauses tied to feedstock escalation parameters.

R&D and product differentiation: Prioritize ETU-free and lead-free curatives and accelerate validation of bio-based epichlorohydrin feedstock routes to meet OEM sustainability mandates and reduce scope-3 exposure.

Commercial and pricing: Adopt value-based pricing for specialty grades (e.g., formulations validated for biofuels or elevated thermal windows). Use backward linkage analysis to model how epichlorohydrin price volatility transmits to finished goods margins.

Capacity and manufacturing footprint: Evaluate co-investment or tolling arrangements in regions with emerging epichlorohydrin production capacity to shorten lead times and mitigate logistic friction.

M&A and partnerships: Target niche compounders with application-specific certifications or cure-technology IP to accelerate product line extensions without heavy capex.

Scenario planning: Build stress scenarios around feedstock disruption, stricter automotive emission/chemical rules, and accelerated print-sector substitution to quantify EBIT impacts and capital prioritization choices.

The published study is intentionally practical. It includes a consolidated market model with annualized topline revenue forecasts from 2020 through 2032, a transparent methodology appendix, and sensitivity modeling tied to feedstock price and volume shocks. The report also contains:

Supplier and capacity tracker (facility-level map, announced expansions, and regional capacity dynamics).

Technology and formulation matrix (homopolymer, copolymer, terpolymer choices; cure systems; performance trade-offs—presented at the specification level, without disclosing client-sensitive allocations).

Commercial benchmarking and contract templates for procurement teams.

Regulatory and ESG impact assessment outlining pathways to reduce carbon intensity through bio-based epichlorohydrin and formulation changes.

Five practical scenario plays with decision triggers tied to price, capacity, and regulatory outcomes.

In keeping with the “trailer” approach, this briefing deliberately highlights insights and strategic takeaways while deferring the underlying segment-level tables, proprietary price curves, and client-ready Excel models to the full report and subscriber portal.

Short-term (0–6 months): renegotiate supply contracts using new information on upstream capacity additions and recent supplier price actions; add containment language for feedstock-driven escalators.

Medium-term (6–18 months): prioritize validation of ETU-free formulations for high-volume automotive and industrial sealing lines; engage R&D partners to trial bio-based epichlorohydrin routes.

Long-term (18+ months): consider strategic investments in regional finishing capacity or minority stakes in specialized compounders to capture margin and accelerate time-to-market for premium formulations.

For 2026, managing the ECO rubber value chain will be about balancing three levers: upstream feedstock exposure, product and process innovation (particularly for regulatory-compliant cure systems and bio-based feedstocks), and targeted commercial arrangements with a concentrated supplier base. PW Consulting’s report arms executives with the models and playbooks needed to convert market signals into actionable sourcing, investment, and product decisions. We encourage procurement, R&D, and corporate development teams to review the full report and the underlying datasets to operationalize the scenarios most relevant to their portfolio.

To access the complete report, segment-level tables, and downloadable model, please visit the PW Consulting report page. Subscribers and enterprise clients can request a tailored briefing or a workshop to translate the findings into a bespoke 2026 action plan.

For detailed analysis of this topic, please visit the official page:Cochloroether Rubber Eco Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com