PW Consulting Releases Strategic Brief: Wafer Purge System Market Research — A Decision-Grade Preview for 2026

As semiconductor supply chains reconfigure and advanced-node production scales in 2026, wafer purge systems are transitioning from complementary utilities to mission-critical enablers of yield, throughput and sustainability. PW Consulting’s latest market research, anchored on a 2025 base year and a 2026–2032 forecast horizon, synthesizes quantitative market-sizing with operational playbooks that C-suite teams, plant managers and procurement leaders can act on immediately. This release summarizes the strategic implications and high-level findings of the report — intentionally omitting granular regional and application splits to preserve the report’s role as the definitive source for subscribers.

Wafer Purge System Market Research

Market at a glance: robust growth, measurable upside

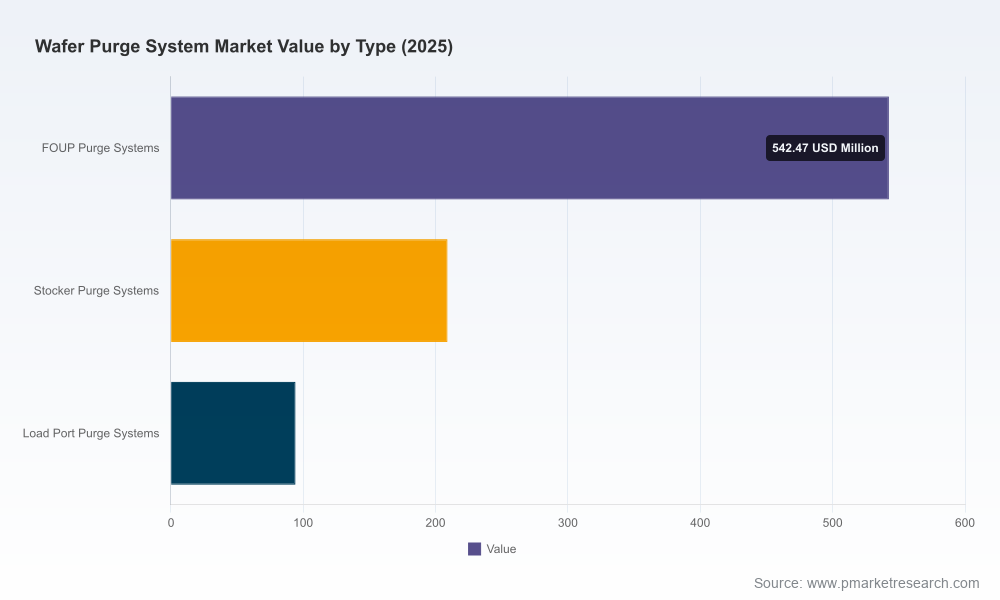

Our macro model shows the wafer purge system market expanding from an assessed USD 845.5 Million in the base year (2025) to an estimated USD 924.7 Million in 2026, and accelerating across the forecast period to reach ~USD 1.6 Billion by 2032. This trajectory corresponds to a compounded annual growth rate (CAGR) of approximately 9.5% for 2026–2032. Historical trend analysis (2020–2025) demonstrates consistent expansion driven by 300mm fab buildouts, retrofits in mature fabs, and growing adoption of integrated purge solutions in automation stacks.

Wafer Purge System Market Research

Market concentration is meaningful: the top three vendors account for a clear majority share (CR3 ~58.4%), and the top five push concentration further (CR5 ~76.3%). These concentration metrics underline a market where established suppliers can shape standards, but also leave room for targeted, technology-driven challengers.

Wafer Purge System Market Research

Why this matters for 2026 decision-makers

- Yield protection as a strategic lever: Nitrogen purge strategies are no longer a shop-floor detail. For fabs pushing tighter process windows and heterogeneous integration, effective purge systems materially reduce surface oxidation and airborne contamination — translating into observable yield gains and lower rework rates. PW’s scenario models show that even modest improvements in in-line oxidation control compound into significant P&L impact over multi-year production ramps.

- CapEx vs. OpEx trade-offs: Decision-makers must balance equipment acquisition, retrofit complexity and ongoing gas consumption. New valve and nozzle technologies — and smarter flow-control strategies — can reduce nitrogen demand materially, shifting ROI profiles in favor of more advanced systems despite higher upfront costs.

- Compliance and market access: Regulatory regimes (including SEMI S2 conformity and export control frameworks that affect front-end equipment) are non-negotiable inputs to sourcing decisions. Our report operationalizes compliance checks into procurement gates to avoid costly retrofits or export license delays.

- Supply-chain resilience: Raw material trends — notably rising stainless steel and sensor component costs — increase manufacturing cost pressure. Firms able to lock favorable supplier terms or redesign for alternate materials will maintain margin integrity.

What the PW Consulting report gives you — the pragmatic toolkit

The full study moves beyond headline numbers to provide tactical, implementable assets that support 2026 strategy cycles. Key deliverables include:

- Proprietary market-sizing model by year (2020–2032) with scenario toggles for demand shocks, energy price volatility and gas-supply constraints.

- Vendor scorecards with capability matrices (technology, retrofit friendliness, automation integration, service footprint) and a defensible methodology for supplier shortlists.

- Customer-oriented decision frameworks: CapEx/OpEx heatmaps, total cost of ownership calculators, and break-even analyses under alternate nitrogen pricing and flow-efficiency assumptions.

- Implementation playbooks for plant engineers: retrofit sequencing, cleanroom integration checklists, MFC (mass flow controller) tuning recipes, and contamination validation protocols aligned with SEMI guidelines.

- Regulatory and export-risk maps tied to sourcing strategies, plus templated language for RFPs and compliance documentation to accelerate procurement.

- Scenario-driven strategic options for OEMs and component suppliers: partnership archetypes, buy/build decision trees, and M&A targets informed by concentration metrics.

To preserve the value of proprietary analysis, the report does not publicly disclose detailed regional and application-level splits in this summary. Subscribers and authorized licensees receive full disaggregation, raw model outputs and the underlying assumptions required for bespoke sensitivity testing.

Competitive landscape — capability contrasts and strategic vectors

The vendor ecosystem includes long-established automation integrators, specialized purge-focused firms, and component innovators. Below are concise strategic assessments of core players featured in our vendor analysis; full profiles and scorecards are available in the report.

- Fabmatics (Germany) — A specialist in retrofittable pod purge solutions for FOUP and SMIF systems, Fabmatics combines modularity with extensive field validation. Its focus on continuous purge during interim storage (Zero Footprint Storage, overhead buffers, stockers) positions it well for retrofit-driven demand at advanced nodes.

- Murata Machinery / Muratec (Japan) — With thin purge retrofit units, mass-flow control and high-efficiency nozzle designs, Muratec competes on engineering precision and integration with existing stocker fleets. Its strengths lie in reliability and the technical rigor required by tier-one fabs.

- Rorze Corporation (Japan) — Rorze brings in-house stocker and load-port purge options, emphasizing low flow and high cleanliness. The company’s nozzle mechanisms and systems-level integration suit high-volume FOUP handling environments.

- Palbam Class (Israel) — A niche provider of purge stations and ultraclean N2 cabinets, Palbam Class excels in automated control and desiccator-style storage solutions suited for sensitive process steps.

- Daifuku (Japan) — As an AMHS and material handling incumbent, Daifuku integrates nitrogen purge capabilities into broader logistics solutions, offering value in holistic automation and factory-floor orchestration.

- Sinfonia Technology (Japan) — Focused on FOUP load ports for 300mm, Sinfonia’s movable-nozzle designs and EFEM compatibility make it a pragmatic choice for equipment OEMs and fab customers seeking low-oxygen interfaces.

- Kostek Systems (South Korea) — Kostek’s LPM modules and communications-enabled MFCs are tailored to OEM partners that prioritize real-time O2 monitoring and host-level integration.

- Santa Phoenix Technology (Taiwan) — Noted for installations in major foundries, SPTI’s advanced charging units and storage systems have strong appeal in high-volume 300mm fabs.

- SEMI-TS (South Korea) — Offering smart purge solutions as part of AMHS, recent exhibition activity evidences a market push to combine purge functions with clean conveyors and standardized material handling interfaces.

Collectively, these players illustrate two strategic pathways: (1) integrated AMHS suppliers offering purge as part of a broader automation stack, and (2) focused purge-system specialists driving technological differentiation (nozzles, low-flow valves, adaptive control). Our vendor matrix maps supplier archetypes to client use cases to accelerate shortlist creation.

Industry dynamics and risk vectors

- Raw material and component inflation: Stainless steel and electronic sensor components account for a large share of manufacturing cost in purge equipment; recent trends show price pressure that manufacturers must either absorb or pass through. The report models cost-pass-through scenarios and identifies engineering levers to reduce bill-of-material exposure.

- Flow-efficiency innovations: New actuator and valve technologies — including piezo-based low-energy flow valves — can reduce nitrogen consumption dramatically (industry claims indicate reductions up to ~75% in some implementations). These innovations materially affect operating expense projections and sustainability metrics.

- Regulatory compliance: SEMI S2 and national export controls create operational constraints and potential gating events for cross-border equipment flows. The report offers a compliance-ready procurement checklist to mitigate delays and licensing risks.

- Value-at-stake from purging: Historical studies and field reports suggest significant annual savings from N2-purged bare wafer stockers through reduced cleaning and scrap; we translate these into present-value terms across typical fab lifecycles to inform investment thresholds.

Actionable recommendations for 2026

- Prioritize retrofit pilots in buffer zones and stockers where purge ROI is fastest — use PW’s TCO calculator to identify break-even timing under your nitrogen pricing profile.

- Negotiate supplier contracts that include performance SLAs for oxygen/humidity targets and gas-consumption caps; structure incentives around continuous improvement on consumption.

- Invest in flow-efficiency upgrades (nozzles, MFCs, low-energy valves) for legacy installations to achieve rapid OpEx reductions without full system replacement.

- Embed compliance gating into sourcing and logistics processes — no retrofit should ship without certifiable SEMI S2 alignment and export-clearance mapping where relevant.

- Assess strategic partnerships or minority investments in niche purge-specialists if your strategy emphasizes differentiation via process control and yield protection.

Next steps & how to access the full study

PW Consulting’s Wafer Purge System Market Research report is designed to be a decision tool for 2026 planning cycles — combining market modeling, vendor intelligence, and plant-level implementation guidance. For complete regional and application breakdowns, vendor scorecards, downloadable model files, and the full set of recommendations and procurement templates, visit our report page or contact PW Consulting’s semiconductor practice. The executive briefing includes a walk-through of model scenarios and a customized workshop option to translate findings into your 2026 operating plan.

PW Consulting remains committed to delivering research that is both rigorous and immediately deployable. For inquiries, licensing or to schedule a briefing, please contact our industry desk.

For detailed analysis of this topic, please visit the official page:Wafer Purge System Market Research

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com