JetBlue Infant Birth Certificate Requirements for Domestic & International Travel

Other |

2026-06-24 17:56:32

PW Consulting’s latest market study on Built‑In Electric Curtains frames a rapidly maturing opportunity set for hardware manufacturers, system integrators, real‑estate developers and institutional buyers planning 2026 investments. Using 2025 as the base year and a 2026–2032 forecast horizon, the report projects sustained compound growth (CAGR ~10.51%) driven by accelerating smart‑home adoption, commercial retrofit cycles and an expanding addressable market for integrated track and recessed installations. The headline trajectory — a meaningful step up from mid‑2020s levels toward multi‑billion‑dollar industry scale by the end of the decade — should reframe how corporates allocate R&D, M&A and channel resources in 2026.

Built In Electric Curtains Market

Actionable foresight: The market’s double‑digit CAGR creates a near‑term window to capture scale effects, but the window is conditioned by product‑level choices (power architecture, integration layer) that will lock in cost and channel dynamics for years.

Built In Electric Curtains Market

Timing implications for product roadmaps: Companies must choose between rapid premium positioning (high‑integration, full systems) and volume plays (OEM motor supply, retrofit kits). The wrong choice can lead to margin compression as competition intensifies.

Built In Electric Curtains Market

Supply‑chain and regulatory urgency: Tariff exposures on motors, fabrics and aluminum extrusions — coupled with safety standards and import duty dynamics — require procurement hedges and alternative sourcing strategies in 2026 to protect gross margins.

Integration and platform bets: Interoperability standards (Matter/Thread, Zigbee/RTS families) and ecosystem partnerships will determine future control‑layer economics; early platform alignment in 2026 is a differentiation lever.

High‑fidelity market model: Annual total market sizing from the historical period through 2032, including scenario runs, upside/downside cases and sensitivity to macro drivers (installation rates, material cost inflation, tariff shocks).

Segmentation framework and investment lenses: Power source, installation type (built‑in recessed, track, retrofit) and end‑use categories with detailed demand drivers and adoption curves for each lens.

Competitive scorecards: Strategic positioning, channel footprint, product capabilities, and go‑to‑market competencies for the key global players — enabling side‑by‑side benchmarking.

Supply‑chain risk map: Components, critical raw materials and freight/tariff exposures; procurement playbook with alternative sourcing and nearshoring scenarios.

Commercial playbooks and pricing models: Channel segmentation (builders/specifiers vs installers vs OEM buyers), margin tables, and suggested commercial terms for 2026 contract negotiations.

M&A and partnership screen: Criteria‑based target lists and accretion/dilution modeling for roll‑up strategies and technology tuck‑ins.

Regulatory & standards impact assessment: Practical implications of safety norms and trade policy on product redesign costs and time‑to‑market.

Smart home convergence: Increasing buyer preference for unified control systems — voice, app and home automation hubs — pushes product requirements beyond basic motorization to include secure firmware, OTA update capability and certified interoperability. Vendors that demonstrate robust integration are capturing premium projects.

Power architecture tradeoffs: AC mains, rechargeable battery and solar options coexist, each with distinct value propositions across retrofit and new‑build segments. The 2026 battleground will center on energy management (battery longevity, power‑saving controls) and installation speed.

Channel evolution: Traditional window‑treatment dealers, smart‑home integrators and construction specifiers are converging. Providers that design clear SKUs, certification programs and installer enablement will dominate local volume capture.

Regulatory and trade pressures: Import tariffs on components and additional duties on extrusions are creating downward pressure on gross margins for players reliant on offshore manufacturing. Concurrently, safety standards that phase out free‑hanging cords accelerate motorization adoption but increase compliance costs.

Consolidation signal: The market is neither atomized nor monopolistic — an oligopolistic dynamic is emerging. The top commercial players hold a meaningful share of the market, leaving opportunity for nimble challengers focusing on niches or system‑level differentiation.

Somfy — Global systems leader: Strength in specialized motors, integrated systems and platformization for both residential and commercial recessed installations. Somfy’s ecosystem play (proprietary apps and wide protocol support) is a reference architecture for premium specifiers.

Hunter Douglas — Premium, project scale reach: Proprietary motorization lines combine with an entrenched distribution network in high‑end projects; the company’s strengths are in custom solutions and premium channels.

Lutron Electronics — Systems integrator for luxury and commercial builds: Lutron’s shading and lighting convergence creates a differentiated value proposition for whole‑room automation and high‑spec commercial deployments.

Silent Gliss — Track & quiet performance specialist: Focus on track systems and noise‑sensitive applications positions Silent Gliss for hospitality and healthcare projects where acoustic performance and durable engineering matter.

Coulisse (Motionblinds) — Digital‑first B2B challenger: Rapid adoption of standards like Matter via recent product innovations (e.g., the Motionblinds Matter Bridge) signals a play for integrator and installer ecosystems that demand easy smart‑home interoperability.

Dooya — OEM motor scale: As a leading motor OEM, Dooya supplies many motorized systems globally; its advantage is cost and manufacturing scale for tubular and curtain motors used in integrated track solutions.

Notably, Coulisse’s April 2025 product announcement — a Matter bridge and smart showroom initiative — is emblematic of a broader platform race where software and UX matter as much as mechanical reliability.

For incumbents targeting premium projects: Double down on integration with building management systems and specifier‑level toolkits. Invest in certified interoperability and installer training to protect margin in high‑value commercial pipelines.

For OEMs and component suppliers: Prioritize diversification of manufacturing footprints to mitigate tariff exposure and insulate margins from aluminum and motor duties. Offer bundled supply‑and‑installation packages to capture higher supply‑chain economics.

For challengers and scale‑seeking startups: Win on go‑to‑market clarity — specialize in a vertical (e.g., hospitality or multi‑family residential) and deliver turn‑key solutions that reduce project friction. Use Matter/Thread compatibility as a market entry enabler.

For channel partners and integrators: Build standard installer certification programs and ROI calculators for clients that quantify labor savings, energy benefits and lifecycle maintenance costs — these tools accelerate procurement decisions in 2026.

For investors and M&A strategists: Prioritize targets that deliver one or more of: proprietary integration software, recurring service revenue (maintenance/monitoring), or scale in critical components where tariffs create supply barriers for competitors.

Tariff and raw‑material shocks: Hedging strategies include nearshoring, long‑term supplier contracts with indexation clauses, and design for alternative alloys or composites where feasible.

Standards‑driven redesign costs: Anticipate compliance timelines and budget for product reengineering and certification; use modular electronics architectures to accelerate compliance cycles.

Cybersecurity & firmware risk: As products become internet‑enabled, implement secure boot/OTA governance and consumer breach response playbooks to preserve brand trust.

Channel disintermediation: Protect margins by offering exclusive services, installer training, and platform subscriptions rather than competing solely on hardware price.

Transparent forecasting: The study combines bottom‑up unit economics with top‑down adoption scenarios and is stress‑tested against tariff, material cost and standards shocks.

Vendor validation: Primary interviews with manufacturers, integrators and large installers underpin the competitive profiles and channel assumptions.

Practical output: The deliverables are designed as decision tools — not academic tables — including playbooks, negotiation checklists and scenario dashboards you can operationalize in 2026.

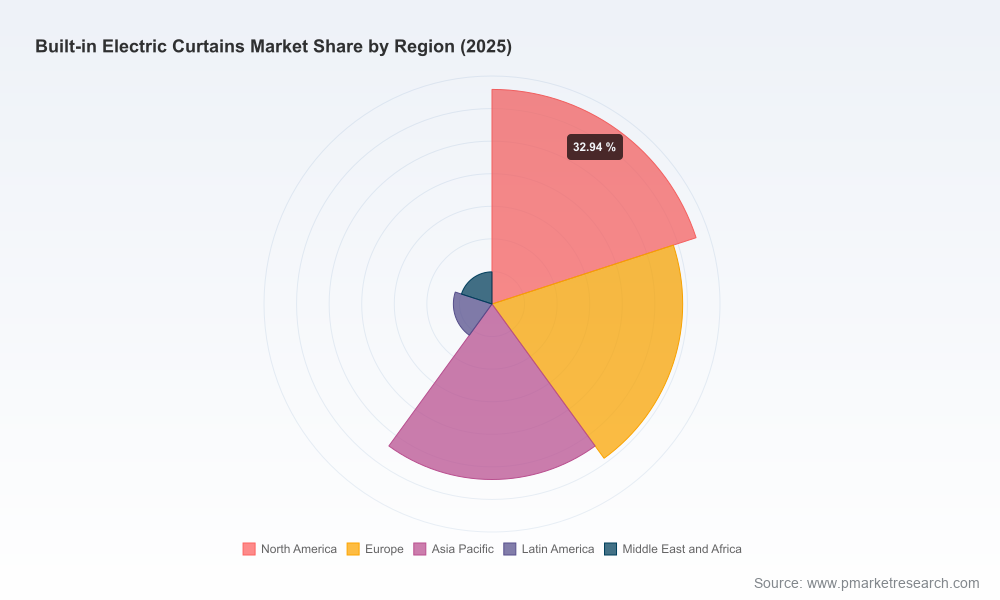

This briefing intentionally omits the granular sub‑segment and regional line items that drive specific commercial actions (detailed power‑source breakdowns, regional splits, and exact segment revenues). PW Consulting’s full report includes those critical datasets, downloadable models, vendor scorecards and our interactive scenario toolset — all calibrated for rapid 2026 decision cycles.

For immediate access to the full Built‑In Electric Curtains Market report, bespoke briefings and implementation workshops for 2026 planning, contact PW Consulting’s Built‑Environment practice. Our team will provide the full dataset, a tailored executive summary focused on your strategic choices, and a 90‑day playbook to convert analysis into market share.

— PW Consulting, Senior Strategy & Industry Analysis Team

For detailed analysis of this topic, please visit the official page:Built In Electric Curtains Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com