PW Consulting Releases Orthodontic Aids Market Strategic Brief: A 2026 Playbook for Executive Decisions

PW Consulting today publishes a strategic companion to our full Orthodontic Aids Market report (base year 2025), providing senior executives and investors with the high‑level, decision‑critical perspective they need to act in 2026. Our independent analysis shows the global orthodontic‑aids market has grown steadily through 2020–2025 and is positioned for continued expansion across the 2026–2032 forecast window at an aggregate CAGR of 8.45%. The market scale at the 2025 base year and the multi‑year trajectory to 2032 both underscore a commercially attractive, technology‑led phase for the sector.

Orthodontic Aids Market

What this briefing delivers for 2026 decision‑makers

- Evidence‑based implications of the market’s growth trajectory for capital allocation, product road maps, and channel strategy.

- An executive summary of competitive positions and capability gaps that will determine winners and laggards in the near term.

- Actionable regulatory and reimbursement priorities that materially affect time‑to‑market and revenue recognition in 2026.

- A concise strategic playbook that translates market dynamics into prioritized initiatives for product, commercial, and M&A teams.

Macro picture: why 2026 is a turning point

After robust recovery and expansion during 2020–2025, the market enters 2026 from a position of scale and momentum. Our forecast through 2032 reflects an industry undergoing structural shifts — digital treatment planning, AI‑assisted diagnostics, and hybrid care delivery models — rather than simple cyclical demand. A mid‑single to high‑single digit CAGR reflects steady elective care demand, rising penetration of aesthetic and digitally enabled solutions, and incremental upselling of adjunct devices and consumables across clinical channels.

Orthodontic Aids Market

For 2026 corporate planning cycles, this combination of predictable growth and structural change translates into three practical implications: (1) investment in digital and regulatory competencies will compound return on product innovation, (2) established manufacturers must accelerate service‑based offerings to defend margins, and (3) new entrants and non‑traditional players will drive consolidation pressure in specific technology niches.

Orthodontic Aids Market

Report contents: practical tools included

Our full report is designed as an operational toolkit for strategy teams. Highlights include:

- A 2020–2032 market model with base‑case and two alternate scenarios aligned to macroeconomic, reimbursement, and regulatory contingencies.

- Top‑line demand drivers and sensitivity analysis to test price, utilization, and channel shifts against revenue outcomes.

- Commercial playbooks by cohort (incumbent manufacturer, regional distributor, DSO, digital health entrant) with prioritized tactics and KPIs for 12–24 month horizons.

- Regulatory pathway matrices and recommended clinical evidence packages for Class II orthodontic devices across major jurisdictions.

- M&A screening criteria and integration checklists targeting technology bolt‑ons, consumables scale plays, and channel consolidators.

- Downloadable financial model (Excel) and scenario toggles to support board‑level sensitivity analysis.

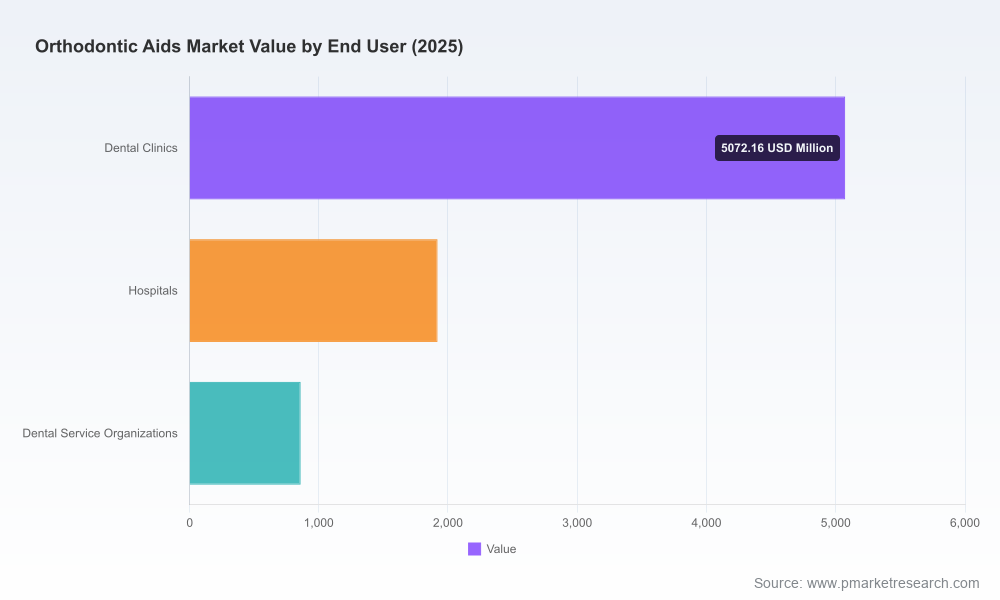

Note: To preserve the utility of this executive brief as a strategic “trailer,” detailed segment‑level tables and granular regional / application splits are reserved for the full report and accompanying data package available through our site.

Competitive landscape: who to watch and why

The market combines a few large, vertically integrated players with a broad tail of specialist manufacturers and distributors. The three largest firms collectively account for a majority share of the market, and the top five firms consolidate roughly two‑thirds of industry revenues — a concentration that shapes pricing power and innovation pathways.

Strategic perspectives on leading firms:

- Align Technology — Continues to lead in digitally enabled aligner therapy and scanner ecosystems. Recent regulatory clearances for specialized attachment systems and palatal expander platforms extend Align’s control over clinical workflows and increase switching costs for providers that adopt its end‑to‑end stack.

- 3M — A diversified portfolio player with deep channel reach across brackets, wires, and aesthetic offerings. Its strengths lie in product breadth, supply chain scale, and distributor relationships that defend traditional fixed appliance demand.

- Envista / Ormco — Competes on bracket/wire systems and lab integration; its value proposition centers on system‑level efficiency for tooth movement and orthodontic laboratories.

- DENTSPLY SIRONA — Blends device and consumer‑facing product strategies, with digital treatment appliances and adjunct devices (e.g., high‑frequency vibration) that target outcome improvement and treatment acceleration.

- Institut Straumann — Leverages an integrated dental platform strategy, connecting implantology and restorative workflows to orthodontic digital offerings — a model attractive to practice groups seeking cross‑sell efficiencies.

- Specialist manufacturers and distributors — Companies such as American Orthodontics, Rocky Mountain Orthodontics, G&H, Dentaurum, Henry Schein’s orthodontics arm and UK‑based DB Orthodontics continue to serve as primary suppliers to clinicians with differentiated product attributes (e.g., archwire metallurgy, bracket tolerances, value pricing).

Recent regulatory and product developments — including multiple 510(k) clearances for AI‑enabled imaging and novel appliance attachments, CE marking activity, and new aesthetic bracket launches — are changing competitive dynamics by lowering technical barriers for niche entrants while raising the cost of claims and evidence for broad market adoption.

Regulatory and reimbursement dynamics to prioritize in 2026

- Class II device pathways remain central. Firms must actively manage 510(k) strategies, predicate selection, and post‑market surveillance to avoid launch delays and costly recalls.

- European MDR and national conformity processes demand robust biocompatibility and clinical data; multi‑jurisdictional file harmonization should be treated as a program rather than a one‑off activity.

- Reimbursement coding changes effective January 1, 2026 (updated CDT codes) materially influence claims processing and revenue recognition for provider partners; early payer engagement and clinical documentation templates are immediate priorities.

- Direct‑to‑consumer model risk remains elevated after market suspensions and operational curtailments observed in late‑stage DTC cases; legal and compliance functions should stress‑test distribution models for regulatory exposure.

Recommended 2026 strategic plays

Based on our scenario analysis and interviews with C‑suite and clinical leaders, we recommend the following prioritized actions for 2026 planning cycles:

- Double‑down on digital integration — Allocate budget to scanner, AI imaging, and treatment‑planning integrations that increase lifetime value of provider relationships and permit higher ASPs for bundled solutions.

- Build regulatory‑led product road maps — Invest up front in the clinical evidence required for Class II pathways, especially for devices that embed software or AI components; this reduces launch risk and shortens commercialization timelines.

- Pursue selective M&A — Target capabilities that accelerate digital workflows (3D imaging, AI diagnostics), recurring consumable streams, or regional distribution scale — and insist on integration KPIs that protect gross margin improvement.

- Engage payers early — Map revised CDT codes to product bundles and pilot coding pathways with major DSOs and hospital systems to accelerate reimbursement acceptance.

- Harden supply chains — Secure critical materials and diversify manufacturing footprints to mitigate geopolitical and raw‑material disruptions that have begun to appear in orthodontic consumables markets.

- Design value‑based commercial models — Experiment with outcome‑linked pricing and treatment acceleration bundles to differentiate on clinical and economic value rather than price alone.

How PW Consulting’s full report supports execution

The full Orthodontic Aids Market report is intentionally structured for use in board rooms and strategy workshops. It provides the complete dataset, segment and regional breakdowns, supplier scorecards, and an executable two‑year implementation roadmap tied to measurable KPIs. Our clients use the package to align R&D budgets, refine commercial territories, and prioritize M&A targets with a clear linkage to modeled revenue and margin outcomes.

Because this briefing follows a “trailer” principle, we have intentionally highlighted strategic implications while reserving detailed tables and segment‑level figures for the full report and data subscription. This preserves the report’s value as an operational decision support asset.

Next steps

If your 2026 planning requires a fact‑based, executable strategy for product development, regulatory planning, commercial execution, or M&A screening in the orthodontic aids arena, PW Consulting’s full report and the supporting data model provide the precise inputs you need. Contact our advisory desk to arrange a briefing, license the dataset, or commission a tailored strategic workshop that translates the market forecast and scenario analyses into a specific 12–24 month action plan for your organization.

For detailed analysis of this topic, please visit the official page:Orthodontic Aids Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com