Lyocell Fiber Market Overview: Key Drivers and Challenges

Other |

2026-05-28 09:43:40

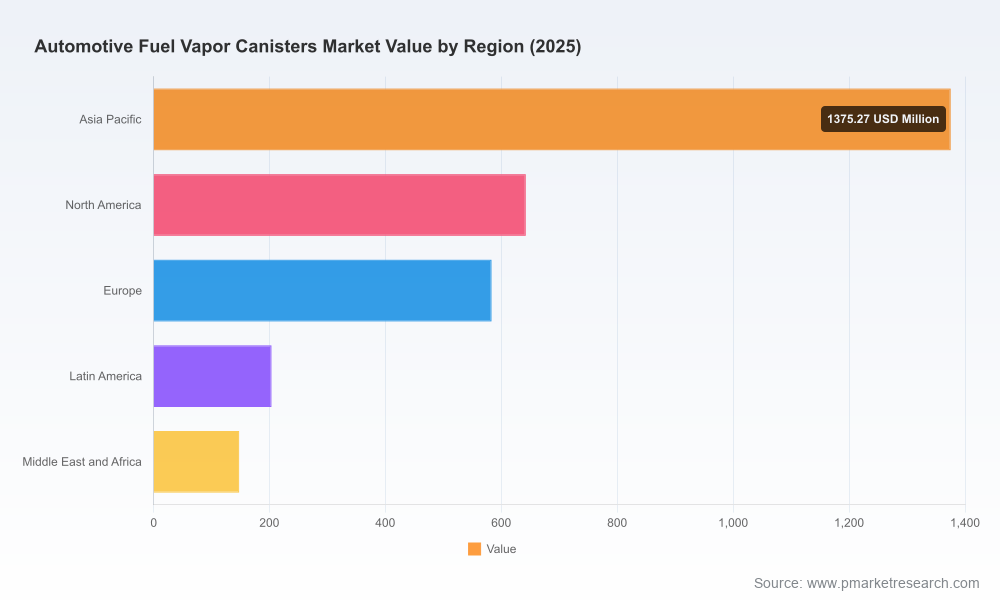

As governments and OEMs accelerate efforts to reduce evaporative hydrocarbon emissions, the automotive fuel vapor canisters market has moved from a compliance afterthought to a strategic battleground. PW Consulting’s forthcoming market study — covering 2020–2025 historicals with forecasts through 2032 — provides a practical blueprint for executives who must make capital allocation, sourcing, product, and M&A decisions in 2026. The global market is estimated at approximately USD 2,952.2 Million in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 3.42% over the 2026–2032 forecast window. This brief outlines why that growth matters, where real strategic levers lie, and how the report’s tools will alter decision outcomes — while preserving the proprietary data that drives our recommendations.

Automotive Fuel Vapor Canisters Market

From regulatory tightening to fuel-blend complexity: Multiple jurisdictions (notably CARB, EPA, Euro regulators and China standards) have tightened running-loss and diurnal test requirements and detailed canister performance protocols. The result is a baseline technical hurdle that increasingly determines market access for new-vehicle platforms.

Automotive Fuel Vapor Canisters Market

System-level optimization opportunity: Canisters no longer function as passive appendages. They are part of integrated fuel-management and powertrain strategies — interacting with purge control algorithms, tank-venting architecture, and, in some applications, alternative-fuel validation. Design choices in canister media, flow-pathing, and purge-control interfaces materially affect vehicle-level emissions, certification timelines, and total-cost-of-ownership.

Automotive Fuel Vapor Canisters Market

Value migration into adjacent domains: Materials (activated carbon feeds), modular hardware (multi-layer media, high-flow canisters), and aftermarket serviceability are shifting value away from basic commodity canisters to suppliers that can pack regulatory assurance, validated performance, and predictable supply into their offerings.

Decision-grade market sizing and scenarios: We provide a consolidated topline and three demand scenarios that translate regulatory vectors and fuel-blend trajectories into order of magnitude volume and revenue outcomes through 2032. These scenarios are calibrated to the market’s historic behavior and modeled sensitivity to key variables (regulatory phase-ins, fuel composition shifts, EV adoption offsets).

Regulatory impact matrix and compliance playbook: A granular mapping of global regulatory milestones, certification protocols (including operational test procedures and canister working-capacity validation), and a set of mitigation strategies for OEMs and Tier suppliers that prioritizes low-cost compliance versus premium-performance architectures.

Supplier and raw-material risk maps: Supply chain heatmaps that show concentration risk for activated carbon feedstocks, exposure to feedstock variability, and logistics vulnerabilities. The report includes supplier-tiering criteria, qualification checklists, and short- and medium-term hedging levers to stabilize media supply and mitigate price volatility.

Technology & product playbook: Product-level decision trees comparing single-layer versus multi-layer media, composite housings, high-flow variants, and integration pathways for OBD and purge diagnostics. Each option is modeled for certification risk, incremental bill-of-material (BOM) cost, and operational fuel-consumption trade-offs.

Aftermarket and service-life strategies: Practical guidance for aftermarket players on program expansion, parts coverage prioritization, and warranty-risk modeling — informed by recent program moves that expand late-model coverage across major light-truck and van platforms.

M&A and partnership scorecards: Identification of strategically relevant targets across media producers, modular canister designers, and aftermarket specialists, with acquisition rationale frameworks, integration risk checklists, and expected synergies under multiple adoption scenarios.

Commercial templates: Go-to-market frameworks for OEM and aftermarket suppliers, including channel segmentation, pricing uplift calculators for certified performance tiers, and sample supplier agreement clauses to secure capacity and quality under tightening emissions regimes.

The sector exhibits meaningful concentration, which shapes supplier negotiation dynamics and the speed of technology diffusion. The top three suppliers account for a majority share of the market, with the five largest vendors holding an even larger cumulative position — a structure that benefits established players who can offer validated media performance, certification support, and global spare-parts networks.

PHINIA Inc.: With decades of evaporative control experience and modular portfolios that support a wide range of tank sizes and blended fuel chemistries, suppliers like PHINIA are positioned to win platform-level contracts where global footprint and multi-fuel validation are non-negotiable.

A. Kayser Automotive Systems GmbH: As a long-standing specialist in activated-carbon canister systems and associated valves and lines, Kayser’s system focus exemplifies the value of integrated supply — especially for OEMs seeking turnkey emission solutions that simplify vehicle assembly and certification.

MAHLE GmbH: Leveraging system-integration expertise for combustion-driven routing of captured hydrocarbons, MAHLE is illustrative of powertrain-integrated approaches that tie canister strategy to overall thermal and emissions management.

Standard Motor Products (SMP): Recent program expansions underscore the aftermarket’s strategic importance. Broad late-model coverage and a large EVAP SKU catalog make SMP a critical partner for fleet operators and independent repair networks seeking rapid serviceability and reduced warranty exposure.

MotoRad and similar manufacturers: Focus on restoring emission controls through replacement canisters and complementary components, positioning these players for steady aftermarket demand even as regulatory regimes evolve.

Ingevity Corporation: As an upstream carbon-material specialist, Ingevity exemplifies how material-science leadership can become a competitive moat — especially where feedstock selection and pore-structure control directly affect certified performance metrics.

Program expansions in the aftermarket: Leading aftermarket suppliers have broadened late-model coverage over the past 18 months, increasing serviceable addressable markets for replacement canisters and purge components. For operators, this reduces downtime risk and supports warranty-cost containment strategies.

Regulatory tightening with defined test protocols: CARB’s 2022 rulemaking introduced explicit evaporative test methods and canister performance benchmarks that become material to platform certification starting in model-year 2026. Companies that align development roadmaps to those protocols will shorten certification cycles and reduce rework costs.

Media supply dynamics: Activated carbon remains the primary adsorbent. Feedstock variability and the need for high-capacity, durable media validated under regulatory test cycles have elevated raw-material risk into procurement conversations — catalyzing partnerships between medium producers and system integrators.

Prioritize regulatory-first design gates: Embed compliance testing protocols (including regulatory working-capacity metrics) at the earliest stages of canister and system design to avoid costly late-stage redesigns. Treat certification targets as design constraints, not checkboxes.

Secure media supply with multi-sourcing and qualification tiers: Put certified alternative suppliers through staged qualification and negotiate capacity options that include price collars or offtake guarantees to mitigate feedstock volatility.

Re-evaluate aftermarket channel strategies: For OEMs, strengthen certified repair networks and parts availability. For aftermarket suppliers, invest in coverage expansion for late-model fleets and OEM-equivalent validation to capture service revenue streams.

Consider targeted M&A for capability gaps: Prioritize acquisitions that close gaps in validated media technology, regulatory testing capability, or geographic spare-parts reach. Use our M&A scorecards to compare expected payback horizons across scenarios.

Shift commercial models toward performance-linked pricing: Where certification or captured-fuel performance can be demonstrated, adopt premium pricing or long-term supply contracts tied to validated working-capacity outcomes.

We built this study for pragmatists. The models are transparent, the scenarios are actionable, and the tools are meant to be operationalized within 90–180 days. Clients tell us they value three outcomes above all:

Faster, lower-risk platform certification by designing to regulatory test protocols up front;

Reduced supply-chain exposure through data-driven supplier strategies and hedging; and

Clear acquisition roadmaps where inorganic options outperform organic development on time-to-market and cost-to-certify.

Our approach balances quantitative rigor with commercial pragmatism: modeling sensitivity to regulatory phase-in schedules, mapping supplier dependencies, and delivering executable workstreams for procurement, product, and M&A teams. Importantly, we present both topline market sizing — reflecting the current USD 2,952.2 Million base and the 3.42% CAGR through 2032 — and the scenario-driven decision levers that translate that topline into prioritized investments.

This briefing is intentionally tactical and illustrative. For teams that need the underlying datasets, granular scenario tables, validated supplier lists, and the full regulatory impact matrix (including test-protocol alignments and certification timelines), the full PW Consulting Automotive Fuel Vapor Canisters Market report contains the proprietary annexes and ready-to-execute templates. Accessing the report will allow your organization to convert the high-level guidance above into procurement tenders, development sprints, and M&A diligences aligned to 2026 priorities.

In a market that is growing steadily and becoming more regulatory-driven, the winners will be those who convert compliance obligations into differentiated product and supply-chain positions. PW Consulting’s study is designed to make that conversion both faster and less risky.

For detailed analysis of this topic, please visit the official page:Automotive Fuel Vapor Canisters Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com