Targeted Drugs for Multiple Myeloma: Strategic Imperatives for 2026 — PW Consulting Preview

Executive Summary

The targeted-drugs market for multiple myeloma has entered a new phase of commercialisation and clinical maturation. Our new PW Consulting market study, anchored on a 2025 base year and a 2026–2032 forecast horizon, projects sustained expansion driven by next-generation biologics, bispecifics, and optimized combination regimens. The market expanded from roughly USD 18.45 billion in 2020 to about USD 25.85 billion in 2025, and our model projects continued growth at a compound annual growth rate (CAGR) of approximately 6.45% through the forecast period. By 2032 the market opportunity approaches the USD 40 billion range, reflecting both durable uptake of approved agents and the progressive introduction of novel modalities.

Targeted Drugs For Multiple Myeloma Market

Why this matters for 2026 corporate decision-making

- Regulatory and reimbursement shifts are accelerating time-to-market and altering value-capture mechanics for targeted therapies.

- Commercial winners will be defined not only by clinical efficacy, but by evidence strategy (including MRD-driven endpoints), supply scalability, and flexible pricing models that respond to generic erosion in legacy agents.

- Portfolio decisions made in 2026 — from launch sequencing to M&A prioritisation — will determine company trajectories for the full 2026–2032 cycle.

Market dynamics shaping near-term strategy

Several structural trends dictate where companies should focus finite resources in 2026. First, regulators are increasingly receptive to surrogate and intermediate endpoints: FDA draft guidance and recent decisions have elevated minimal residual disease (MRD) negativity and complete response as acceptable endpoints to support accelerated approval pathways. Companies with MRD-capable development programs can materially compress development timelines and de-risk launches — but only if sponsors invest in robust, prospectively planned MRD datasets and linked long-term outcome evidence.

Targeted Drugs For Multiple Myeloma Market

Second, real-world evidence has begun to reshape post-approval controls. Regulatory streamlining of monitoring requirements and elimination of certain REMS for CAR-T products — reflecting accumulating safety and real-world data — reduces friction for commercial access and supports broader inpatient and outpatient uptake of cell therapies. Third, legacy oral agents are entering a new phase of price competition as first-wave generic entry starts to erode protected volumes, forcing incumbent companies and payers to revisit bundle and combination pricing models.

Targeted Drugs For Multiple Myeloma Market

Competitive landscape — what 2026 looks like

The competitive architecture combines a handful of diversified global players with nimble biotechs. Key strategic actors and their recent moves provide a clear read on where competitive intensity will concentrate in 2026:

- Johnson & Johnson (Janssen) — A broad targeted portfolio spanning anti-CD38 antibodies, bispecifics, and CAR-T positions Janssen to defend and extend front- and later-line indications. Recent approvals expanding teclistamab combinations and frontline daratumumab-based regimens underscore an integrated combination strategy that pairs biologics with established backbones.

- Bristol Myers Squibb — With established IMiD franchises and next-generation CELMoDs advancing through late-stage testing, BMS is pursuing an oral targeted playbook complemented by CAR-T capabilities. Positive Phase 3 readouts for investigational oral agents materially increase optionality for relapsed/refractory settings.

- Regeneron and other bispecific leaders — Accelerated approvals for BCMA×CD3 bispecifics have introduced a fast-follow commercial class; execution will hinge on manufacturing scale, administration models, and differentiation on safety/tolerability.

- GSK, Pfizer, Amgen, Takeda and others — Each holds targeted assets (ADCs, proteasome inhibitors, bispecifics) that will compete across complementary niches. These firms will win where they align clinical positioning with differentiated payer evidence and streamlined delivery requirements.

- Specialist biotechs and collaborators — CAR-T innovators and companies advancing novel targets continue to be acquisition targets or strategic partners for larger pharmas seeking to fill gaps in BCMA and non-BCMA portfolios.

Recent regulatory and commercial inflection points

- FDA acceptance of MRD as a pathway to accelerated approval: this recalibrates evidence packages required at launch.

- Streamlining of CAR-T REMS and monitoring: reduces long-term administrative burden and enhances hospital adoption.

- Approved bispecifics and ADC combinations now competing for the same relapsed/refractory population: payers will increasingly demand head-to-head value differentiation.

- Generic entry for key IMiD agents has started to materialize, shifting treatment economics and manufacturer incentives for combination development.

Strategic implications and recommended actions for 2026

To translate market opportunity into shareholder value in 2026, leaders must make six pragmatic choices — each with tactical levers our report details.

1. Portfolio prioritisation and go/no-go criteria

- Elevate programs with MRD-endpoint alignment and complementary real-world evidence plans. For asset teams, a go/no-go gate in 2026 should include MRD power calculations and a post-approval outcomes commitment.

- De-prioritise late-stage mono-therapies that lack clear combination pathways or payer-fundable differentiation in a crowded bispecific/ADC environment.

2. Clinical development and trial design

- Design adaptive platforms and randomized controlled comparisons that generate both MRD and long-term survival correlates. Use hybrid trial designs to satisfy accelerated approval while generating confirmatory data for full conversion.

- Invest in centralized MRD testing partnerships and digital endpoints to accelerate cross-trial comparability.

3. Market access, pricing, and contracting

- Prepare value-based contracting templates that account for differential durability between cell therapies, bispecifics, and ADCs. Include outcome triggers linked to MRD and real-world progression-free survival.

- Anticipate generic disruption to oral IMiDs; develop combination pricing that preserves commercial viability for novel agents while acknowledging lower-cost backbone availability.

4. Manufacturing, supply chain and delivery models

- Scale manufacturing capacity for bispecifics and CAR-Ts with flexible capacity arrangements (CMOs with surge capabilities). Hybrid in-house/outsourced strategies reduce time-to-supply risk.

- Redesign commercial models for hospital-administered biologics to exploit REMS reductions — enable outpatient infusion pathways and bundled care tariffs.

5. M&A, partnerships and alliance strategy

- Prioritize acquisitions or licensing that fill mechanistic gaps (e.g., non-BCMA targets, novel payload ADCs, proprietary MRD diagnostics) rather than incremental me-too assets.

- Structure milestone-heavy partnerships that share both clinical and commercial risk — tie payments to MRD-positive outcomes and real-world effectiveness metrics.

6. Commercial execution and launch sequencing

- Sequence launches to leverage combination approvals and key guideline endorsements; invest early in KOL networks to shape guideline adoption where MRD evidence is strongest.

- Differentiate through patient support services for complex modalities (CAR-T / bispecifics) to reduce time-to-treatment and improve adherence to protocolized monitoring.

What the PW Consulting report delivers

The full report is structured to convert insight into action. Key deliverables include:

- A transparent market model (historical and forecasted) with scenario testing across price, uptake, and reimbursement settings.

- Pipeline and product maps linked to clinical timelines, label prospects, and commercialization readiness scores.

- Risk heatmaps across regulatory, IP, and supply-chain dimensions, and an impact matrix quantifying consequences to revenue and access.

- Detailed playbooks: launch sequencing, payer dossier templates, manufacturing scale-up checklists, and M&A valuation frameworks tailored to multiple myeloma assets.

- Primary interview synthesis with clinicians, payers, and hospital pharmacy directors that underpins our assumptions and adoption curves.

What we intentionally withhold in this preview

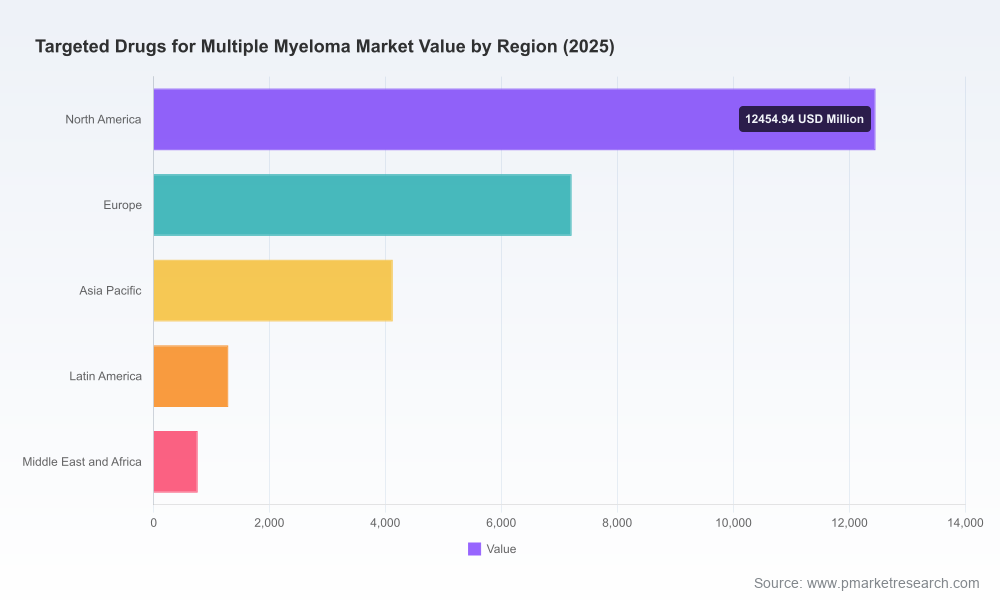

To preserve the strategic value of the full study, detailed segment-level tables, regional splits, channel-level pricing curves, and product-by-product revenue schedules are reserved for the complete report and accompanying decision dashboards. These granular data are essential for transaction due diligence, country-specific market access plans, and in-depth pricing negotiations — and are available through our purchase and advisory engagements.

How PW Consulting supports you in 2026

Beyond delivering the quantitative forecast and qualitative insights, PW Consulting offers bespoke advisory services to translate the report into executable strategies. Typical engagements for 2026 include accelerated launch readiness programs, payer negotiation simulations, MRD evidence packages development, and carve-outs or bolt-on M&A advisory. Our consultants pair industry-specific modeling with hands-on execution tools so that leadership teams can move from insight to signed contracts and operational changes within quarters, not years.

Next steps

For executives planning 2026 portfolio rebalancing, M&A screening, or launch sequencing in the multiple myeloma space, our report provides the evidence base and operational playbooks required to act decisively. Contact PW Consulting to access the full market model, company benchmarking matrices, and tailored advisory options designed to convert 2026 choices into long-term competitive advantage.

For detailed analysis of this topic, please visit the official page:Targeted Drugs For Multiple Myeloma Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com