Millimeter Wave Radar for Unmanned Driving: Strategic Outlook for 2026 Decision‑Makers

PW Consulting's latest market study, "Millimeter Wave Radar For Unmanned Driving Market," delivers a forward‑looking blueprint for executives planning investments, partnerships, and product strategies in 2026 and beyond. Built on a transparent model spanning a 2020–2025 historical baseline and a 2026–2032 forecast horizon, the report combines proprietary market sizing, scenario analysis, vendor benchmarking, and practical playbooks designed to convert insight into immediate action.

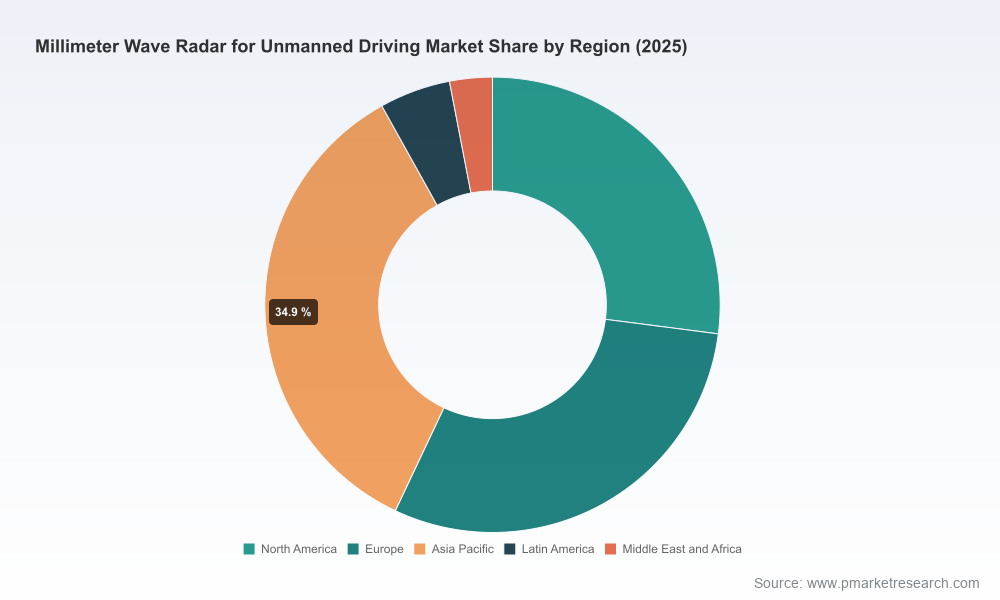

Millimeter Wave Radar For Unmanned Driving Market

Executive snapshot: growth trajectory and market dynamics

Millimeter wave radar is maturing from an ADAS enabler into a foundational sensor for unmanned mobility architectures. Our modeled market expands at a compound annual growth rate (CAGR) of 19.7% across the 2026–2032 forecast window, reflecting accelerated adoption of higher‑frequency radar, advances in 4D imaging, and increasing OEM integration of radar into perception stacks. The market has already seen a pronounced step change from the base year (2025) and continues to scale through the late 2020s under multiple demand scenarios.

Millimeter Wave Radar For Unmanned Driving Market

Key macro facts from our report that matter for 2026 planning:

Millimeter Wave Radar For Unmanned Driving Market

- Comprehensive historical coverage (2020–2025) and a dedicated base year of 2025 underpin the report’s baseline assumptions.

- Projected trajectory through 2032 captures both rapid commercialization phases and sensitivity to supply and regulatory constraints.

- Market concentration is meaningful: the top three vendors hold a near‑majority share of revenue, with the top five firms representing a clear majority of industry sales—an important signal for competitive strategy and supplier selection.

Why this report matters for corporate strategy in 2026

For executives setting 2026 priorities, the radar market presents simultaneous opportunity and operational risk. Our research translates market momentum into pragmatic decision inputs in five areas:

- Product roadmaps: Which radar architectures (high‑frequency SoCs, digital 4D imaging chips, integrated modules) should be prioritized to meet OEM performance and cost targets?

- Supply chain and procurement: How to negotiate flexible long‑term supply agreements while mitigating semiconductor and assembly bottlenecks?

- Partnerships and M&A: When should firms favour tier‑one alliances versus acquisitions of niche radar chipset or software assets?

- Regulatory engagement: Which spectrum and type‑approval developments will materially affect deployment timelines for unmanned systems?

- Manufacturing footprint: What mix of localized assembly, offshore fabs, and co‑development hubs best balances cost, quality and geopolitical risk?

What the report contains — practical, decision‑grade deliverables

This study is intentionally operational. Beyond high‑level forecasts, subscribers receive tools meant for immediate application inside strategy, procurement, R&D and corporate development teams:

- Detailed market sizing and forecasts with transparent methodology and sensitivity testing across demand and supply scenarios.

- Technology landscape mapping: RF architectures, frequency strategies, digital beamforming trends, and the emergence of 4D imaging radar.

- Competitive intelligence: vendor profiles, capability heatmaps, manufacturing footprints and product roadmaps for leading incumbents and challengers.

- Supply chain stress tests: risk matrices, mitigation playbooks (dual‑sourcing, buffer stocking, co‑investment), and cost impact models for semiconductor shortages.

- Commercial playbooks: supplier selection scorecards, OEM engagement templates, pricing negotiation levers, and example term sheets.

- Investment and M&A guidance: target screening criteria, valuation benchmarks, and integration checklists specific to radar and perception software assets.

- Use‑case scenarios and adoption timelines across unmanned driving segments, tied to policy and certification milestones.

To preserve confidentiality and to encourage direct engagement, the report intentionally reserves granular segment breakdowns and detailed regional/application revenue tables for subscribers.

Competitive landscape: where incumbents and challengers are placing their bets

The radar value chain is characterized by a mix of large automotive suppliers scaling production and nimble semiconductor and radar‑specialist entrants pushing performance boundaries. Our report examines each class of competitor and identifies strategic inflection points:

- Tier‑one automotive systems suppliers remain central to OEM roadmaps. Several have moved from prototype to mass production readiness, formalizing major series programs for high‑frequency radar targeted at unmanned and advanced ADAS deployments. Their advantages are scale, OEM relationships and system integration capabilities.

- Legacy semiconductor vendors and MMIC suppliers focus on radar SoCs and RF front‑end solutions that enable Tier‑one sensor modules. Their roadmaps emphasize process nodes, power management and integration with automotive‑grade ASIL processes.

- Radar pure‑plays and startups are commercializing high‑resolution 4D imaging chips and radar‑centric perception subsystems. These firms are notable for rapid iteration, high angular resolution products and partnerships to place chipsets into Tier‑one modules or end‑OEM perception stacks.

Recent industry developments underscore this dynamic: leading Tier‑ones have announced next‑generation sensor programs and scaled production efforts; major semiconductor entrants launched new mmWave SoCs aimed at Level‑2+ and beyond; and radar imaging specialists showcased automotive‑grade 4D systems for integration into unmanned perception stacks. The combined effect is faster product maturation but also competitive pressure on margins and supply chains.

Technology, regulation and supply constraints shaping 2026 decisions

Three forces will dominate the operational environment in 2026:

- Regulatory momentum: Governments globally are accelerating mandates for active safety features, increasing baseline demand for radar in ADAS platforms. At the same time, spectrum allocation for mmWave radar remains uneven across jurisdictions, generating deployment timing uncertainty for certain use cases.

- Semiconductor supply volatility: Persistent supply chain disruptions—particularly for high‑frequency RF chips and specialized packaging—raise the premium on procurement flexibility, inventory strategies and strategic partnerships with foundries and MMIC suppliers.

- Talent and manufacturing cost pressures: A shortage of RF engineering and precision metrology skills is driving up labor costs for automated radar production lines, increasing the value of automation, training programs and co‑development arrangements with manufacturers.

For 2026 planners, these forces mean that product timelines, go‑to‑market plans and supplier commitments should be stress‑tested against both accelerated adoption and constrained supply scenarios. The report includes scenario templates and stress‑test outputs tailored to these exact sensitivities.

Actionable recommendations for 2026 — prioritized and practical

- Secure differentiated perception stacks: Invest in sensor fusion software and validation tooling that leverage radar strengths (robustness in adverse weather, velocity measurement) to create defensible system performance.

- Hedge supply risk tactically: Negotiate conditional long‑term agreements with key MMIC foundries, pursue co‑funded capacity expansions where justified, and adopt multi‑sourcing where possible for critical RF components.

- Pursue selective partnerships: Co‑development pacts with established Tier‑ones accelerate certification and access to OEM programs, while minority investments in radar innovators provide optionality on high‑resolution imaging capabilities.

- Engage early on spectrum and regulation: Proactive regulator engagement and participation in standards bodies can shorten commercialization timelines and prevent regional deployment bottlenecks.

- Embed flexibility in manufacturing footprint: Balance onshore assembly for regulatory or OEM preferences with offshore fabs for cost efficiency, and prioritize automation to counteract skilled labor shortages.

Why PW Consulting’s study is the right input for 2026 decisions

Our report is designed for executives who must translate market forecasts into executable strategies within nine months. We combine quantitative forecasting with qualitative vendor intelligence and hands‑on playbooks. Deliverables include scenario‑based P&L impacts, procurement negotiation artifacts, and an integration checklist for radar hardware and perception software acquisitions.

Note: This release intentionally highlights strategic takeaways and macro results while reserving the full segment tables, regional and application breakouts, and vendor‑level revenue models for subscribers. Those granular exhibits are critical for deal modelling, supplier selection and procurement negotiations and are available through PW Consulting’s subscription portal.

Next steps

Corporates preparing budgets and roadmaps for 2026 should treat radar strategy not as a technical line item, but as a cross‑functional program spanning product, procurement, regulation and M&A. PW Consulting’s "Millimeter Wave Radar For Unmanned Driving Market" report is purpose‑built to convert the sector’s rapid evolution into repeatable decisions and measurable outcomes.

Contact PW Consulting to schedule a briefing, obtain subscriber access to the full dataset and receive tailored scenario work that maps the report’s insights directly onto your 2026 planning cycle.

For detailed analysis of this topic, please visit the official page:Millimeter Wave Radar For Unmanned Driving Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com