Advanced Laser Hair Removal in Dubai Methods

Other |

2026-04-28 11:04:37

PW Consulting’s latest Paper Coaster Market briefing distills the operational imperatives, competitive fault lines, and regulatory inflections that will shape sourcing, product development, and M&A decisions in 2026. The global paper coaster market reached approximately USD 530.0 Million (base year 2025) and, under our base forecast, is set to expand at a 6.2% CAGR across the 2026–2032 horizon, approaching roughly USD 807.5 Million by 2032. This briefing highlights the strategic takeaways executives need now; our full report contains the granular segmentation, supplier scorecards, and scenario models referenced below.

Paper Coaster Market

Three converging forces elevate 2026 from another planning cycle to a decision point: (1) an accelerating recovery in hospitality-led demand and promotional spending after pandemic-era disruption; (2) heightened regulatory pressure around end-of-life management for paper packaging; and (3) renewed raw-material cost dispersion stemming from regional pulp and paper dynamics. Together these drivers change the math on supplier selection, product specifications, and total cost of ownership (TCO) for buyers and brand owners.

Paper Coaster Market

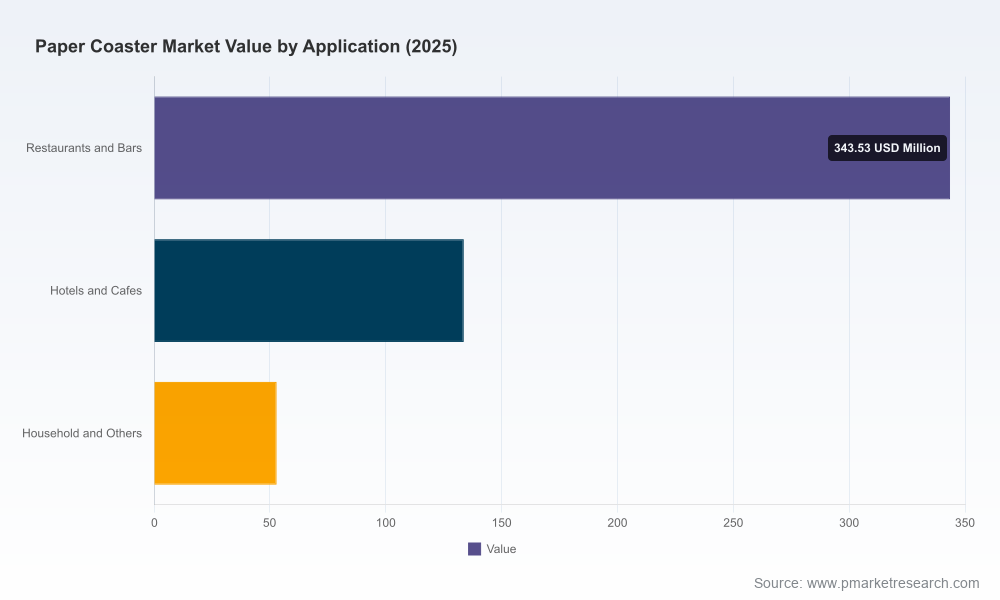

The market’s mid-single-digit CAGR masks important asymmetries that matter to corporate strategy. Growth is supported by steady demand from foodservice and promotional channels, where customization and single-use convenience remain central. At the same time, commodity pressures and sustainability mandates compress margins for low-differentiated producers and create opportunities for premiumization—specialty substrates, higher-end finishing, and certified recycled content.

Paper Coaster Market

For decision-makers, the implication is clear: volume alone will not deliver margin in 2026. Strategic priority must shift toward capture of value through differentiated product features, supply-chain resilience, and regulatory cost management.

Paperboard cost dispersion: Recent market checks show notable regional variation in paperboard pricing (Analysts Insights, March 2026). North American paperboard traded near USD 0.15/kg while prices were higher in Northeast Asia and Europe, and peaked in parts of Southeast Asia. These regional disparities are material to sourcing strategy for exporters and import-dependent buyers.

Price stability does not mean predictability: the US Producer Price Index for corrugated paperboard in sheets and rolls registered a steady read (index ~354), signaling that while headline volatility has calmed, supply tightness and shipping premiums can reassert quickly under demand shocks.

Procurement teams must therefore combine near-term hedging, multi-sourcing across regions, and specification flexibility to manage TCO across raw-material cycles.

Policy developments in North America will materially increase producer obligations in the coming three to seven years. As of late 2025–early 2026, seven U.S. states have adopted comprehensive Extended Producer Responsibility (EPR) laws for packaging and paper products. Washington and Minnesota have launched formal implementation roadmaps with producer responsibility organizations (PROs), cost-sharing mechanisms, and phased compliance milestones toward 2030–2032.

For manufacturers, importers, and brand owners, EPR changes three things immediately: product design constraints (recyclability and reusability), visible cost allocation (fees and PRO contributions), and administrative burden (reporting, registration, and compliance audits). Our advisory is to treat EPR not as a compliance cost only, but as a commercial factor—use it to differentiate through lower-impact product lines and to negotiate supplier contracts with explicitly allocated regulatory liabilities.

The paper coaster market remains fragmented: the top three players account for less than one-fifth of the market, and the top five together control under 30%. Low concentration implies easy entry for regional operators, price competition in commoditized segments, and meaningful opportunity for roll-up strategies by buyers with consolidation appetite.

Fragmentation also creates a two-track competitive environment. On one track, specialist producers compete on speed, customization, and quality finishes (UV spot, foil, airlaid materials). On the other, high-volume, low-cost suppliers—often export-focused—compete on lead-time and unit price. Winning in 2026 means identifying which track your organization intends to dominate and aligning procurement, product design, and channel strategy to that choice.

Direct custom players (e.g., Coaster Factory, Hoffmaster): U.S.-based manufacturers emphasize domestic production, high-volume capability, and a broad palette of finishing options (two-sided printing, colored pulpboard, specialty coatings). Their value proposition is speed-to-market, close technical support, and local supply resilience. Strategic move: deepen value services—digital previews, shorter lead time SKUs, and EPR-compliant labeling.

European specialty providers (e.g., Alfred Mank): Focus on higher-absorbency substrates (airlaid), laminate solutions, and hospitality-grade aesthetics. They can command premium pricing in event and hotel channels. Strategic move: leverage certifications and proprietary material expertise to defend margins.

Promotional and eco-focused suppliers (e.g., Totally Promotional): Compete on brandability and environmental positioning—biodegradable substrates, full-color imprinting, and promotional channels. Strategic move: formalize sustainability credentials (certs, LCAs) and offer circularity partnerships.

China-based mass manufacturers (e.g., Singreen Package, Guangzhou Zhi Xiang): Cost leadership through scale and export logistics. They are natural partners for private-label players and large promotional campaigns but face margin exposure when freight or tariff dynamics shift. Strategic move: pursue service upgrades (kitting, compliance documentation) to move up the value stack.

Run a supplier segmentation exercise: identify strategic suppliers for co-development, tactical suppliers for spot buy, and contingency suppliers for risk mitigation. Include EPR liability in supplier scorecards.

Embed a TCO model that captures raw-material price dispersion, expected EPR fees, logistics variability, and finish-cost premiums. Scenario-test for +20% paperboard price and incremental EPR contributions in your core markets.

Short-list material pilots: evaluate airlaid, certified recycled pulpboard, and PE-laminated options across absorptivity, print fidelity, and end-of-life outcomes. Use objective test metrics (absorption rate, smear resistance, recyclability index).

Pursue design-for-recycling: specify inks, adhesives, and laminates that simplify sorting and reduce EPR exposure; partner with PROs early to align on acceptable pathways.

Negotiate contractual protections: index part of your supply agreements to raw-material indices, include force-majeure and health-check review clauses for regulatory changes, and agree lead-time buffers for high-season promotional windows.

Given low top-line concentration, expect targeted consolidation in 2026–2028 around three propositions: (1) regional scale plays to capture foodservice channel margins; (2) capability acquisitions—digital printing, airlaid technology, or finishing—to raise ASPs; and (3) vertical tie-ups with recycling and collection providers to internalize EPR risk. Private equity interest will favor platform buys that can consolidate contract manufacturing and add a shared-services layer for compliance and procurement optimization.

Our full Paper Coaster Market report is designed for boards, procurement heads, product leaders, and corporate development teams. It contains:

Detailed segmented forecasts (by material, application, and region) with sensitivity scenarios;

Supplier scorecards and comparative capability matrices across production capacity, finishing, ESG credentials, and responsiveness;

Operational templates: TCO calculators, sample RFP language incorporating EPR allocation clauses, and pilot test plans for alternative substrates;

Regulatory scenario analysis mapping state-level EPR rollouts to cost outcomes and compliance pathways;

Case studies on successful product premiumization and procurement-led cost capture, plus an M&A watchlist of value-accretive targets.

Prioritize supplier diversification now—especially if you currently rely on a single region for volume. Re-assess lead-times and freight risk under a 10–20% price shock scenario.

Invest in two to three product pilots that trade up on finish or sustainable content to protect margin when commodity pressure intensifies.

Incorporate EPR scenarios in annual budgets and negotiate supplier contractual language that clearly allocates future regulatory costs.

Monitor consolidation signals: evaluate bolt-on acquisition targets or strategic alliances with recyclers and niche-material providers to secure mid-term margin expansion.

PW Consulting’s market model and strategic playbooks are designed to convert the broad trend data—the USD 530.0 Million base, 6.2% CAGR through 2032, low market concentration, and regional raw-material dispersion—into executable actions for 2026. For executives who need the granular segmentation, supplier identities, and the negotiation templates required to act, our full report provides the necessary detail and operational tools.

Contact PW Consulting to access the full Paper Coaster Market report, request a live briefing, or schedule a bespoke workshop that maps these findings to your supply base and P&L. The market is neither purely a commodity nor entirely a premium niche—2026 will separate those who can operationalize sustainability and customization from those who remain price-takers.

For detailed analysis of this topic, please visit the official page:Paper Coaster Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com