Pet Food Ingredients Market Size, Share, Trends, Growth Opportunities, Key Drivers and Competitive Outlook

Other |

2026-06-19 12:44:53

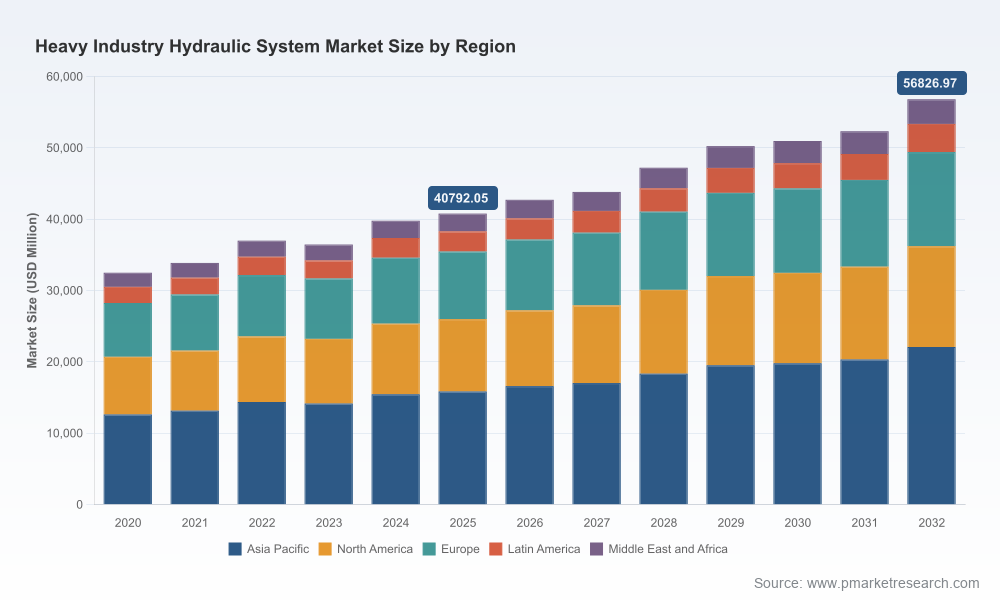

PW Consulting’s latest market research — the Heavy Industry Hydraulic System Market Report (base year 2025) — frames the hydraulic landscape that industrial leaders must navigate as they set budgets, product roadmaps, and M&A priorities for 2026. The market is on a steady expansion trajectory, with the global heavy-industry hydraulic systems market estimated at USD 40,792.05 Million in 2025 and projected to reach USD 56,826.97 Million by 2032, reflecting a compound annual growth rate (CAGR) of 4.85% over the forecast period (2026–2032).

Heavy Industry Hydraulic System Market

Timing: Procurement, R&D, and strategic planning cycles that begin in Q4 2025 and run through 2026 must account for technology shifts, regulatory milestones, and supply-side volatility. Our report synthesizes market growth dynamics—both structural and cyclical—so executives can convert macro forecasts into operational milestones.

Heavy Industry Hydraulic System Market

Execution focus: Rather than a purely descriptive view, the report provides executable modules—TCO models, CAPEX/OPEX scenarios, supplier scorecards, and technology adoption roadmaps—designed for CFOs, CTOs, and heads of procurement to use immediately in budgeting and vendor negotiation.

Heavy Industry Hydraulic System Market

Risk-aware growth: With moderate market concentration (CR3 ~31.5%; CR5 ~44.1%), opportunities exist for regional champions and technology-led entrants. The report maps where consolidation risk is material and where nimble players can capture share through service differentiation and electrified offerings.

Actionable executive summaries and scenario planning: Three investment scenarios (conservative, baseline, aggressive) translate the 4.85% CAGR and the 2026–2032 forecast into budget ranges, payback timelines, and sensitivity analyses tied to commodity and regulatory shocks.

TCO & lifecycle models: Detailed templates for CapEx vs. OpEx trade-offs across hydraulic architectures (traditional hydraulic power units, hybrid-electrified HPU concepts, and fully electrified actuation approaches).

Supplier scorecards & procurement playbooks: Customizable scorecards that blend reliability, service footprint, digitization maturity, and energy-efficiency credentials to accelerate supplier selection and renegotiation cycles.

Technology adoption roadmap: A 24–36 month roadmap for integrating digital hydraulics, telematics, condition-based maintenance, and electrified hydraulic power units (eHPUs), with recommended pilot architectures and KPIs.

Regulatory and standards compliance matrix: A practical guide to aligning product design and procurement with new standards such as ISO 18464:2025 and with regional energy-efficiency mandates that increasingly affect heavy machinery procurement and retrofit specifications.

M&A and partnership screening: Target prioritization frameworks and valuation heuristics for acquirers and private equity firms seeking bolt-ons or capability plays in hydraulics, controls, and service networks.

Case studies and application playbooks: Real-world examples of retrofit programs, electrification pilots, and services-driven revenue models showing unit economics and break-even timelines.

The report’s competitive analysis focuses on incumbent engineering leaders, systems integrators, and regionally strong suppliers. Core players covered include established global names recognized for durability, system expertise, and service networks. Their strategic postures can be summarized in three vectors:

Systems integrators and OEM incumbents that leverage installed base and vertical integration to sell full-system solutions and aftermarket contracts. These organizations compete on reliability, high-pressure capabilities, and global service.

Component specialists pushing energy efficiency and electrification: firms that position advanced pumps, valves, and controls as platforms for decarbonization and OEM differentiation through lower life‑cycle energy consumption.

Regional and niche manufacturers that exploit proximity, customization, and cost-optimized manufacturing to capture OEM and distributor business in specific geographies or end-use niches.

Strategic profiles in the report highlight each leading firm’s strengths and the practical implications for partners and buyers. For example, firms with established portfolios in connected and energy-efficient systems are best placed to win electrification retrofit projects; global OEMs that embed hydraulic systems into their machines command unique aftersales channels; while specialized filtration, hose, and component suppliers can monetize shorter replacement cycles and service agreements.

Regulatory and standards pressure: ISO 18464:2025 introduces prescriptive design methodologies aimed at minimizing energy consumption in hydraulic fluid power systems. This is a direct accelerator for energy-efficient architectures, and our regulatory matrix details compliance timelines and certification implications for product portfolios.

Material cost volatility: Steel-price swings materially affect component economics (cylinders, housings, valve bodies). The report models several steel-price scenarios and their impact on margins, pass-through strategies, and sourcing alternatives.

Electrification and hybridization: Market signals—product awards and exhibitions at leading trade events—illustrate an accelerating interest in electrified hydraulic power units (eHPUs) and hybrid architectures. The report includes an adoption curve and TCO crossover points where electrified solutions become economically preferable.

Service and digitalization: Telematics-enabled condition monitoring and outcome-based service contracts are increasing aftermarket lifetime value and creating defensible annuity streams for suppliers who can deliver predictive maintenance at scale.

Exhibitions and product awards in early 2026 have confirmed the direction of travel: system suppliers and innovative OEMs are publicizing next-generation mobile hydraulic solutions, purpose-built cylinders for OEM integration, and eHPU demonstrators that blend electrification with traditional hydraulics. These events validate both technological progress and market appetite for retrofit and new-build solutions. PW Consulting uses these developments as inputs to short-term demand scenarios and technology diffusion models in the report.

Embed energy-efficiency compliance into product roadmaps: With ISO 18464:2025 and regional mandates shaping procurement, product development teams must prioritize energy-optimized sub-systems and validate energy metrics early in design cycles.

Prioritize electrification pilots where economics fit: Use the provided TCO templates to identify machine classes and operating profiles where eHPUs or hybrid hydraulics reach payback within enterprise planning horizons.

Hedge raw-material exposure: Revise supplier contracts for steel and other commodity inputs, consider multi-sourcing strategies, and explore local sourcing to reduce lead-time and cost volatility.

Monetize aftermarket and services: Build condition-based maintenance bundles and outcome-based service agreements—our revenue models quantify how service can raise margins while reducing customer churn.

Evaluate consolidation selectively: Given a market with material, but not prohibitive, concentration, acquirers should focus on technology and service-led targets that close capability gaps rather than purely scale acquisitions.

Invest in digitization capability: Telematics, analytics, and integration with OEM fleet management are differentiators. The report’s roadmap shows phasing, KPIs, and partner archetypes for rapid deployment.

Leaders using this report can align investment, procurement, R&D and M&A strategies to a rigorously modeled market view. By translating the macro forecast (USD 40,792.05 Million in 2025; USD 56,826.97 Million by 2032; 4.85% CAGR) into actionable playbooks, CFOs and product heads reduce execution risk and create a prioritized, timed pathway to capture share and margin.

Importantly, while this brief communicates strategic direction and macro forecasts, the full report contains the granular market segmentation, regional and end-use breakdowns, supplier shares, and downloadable models that practitioners require to implement the actions summarized here. These detailed tables and datasets are intentionally withheld from this preview to ensure decision-makers access the complete, validated datasets via the official PW Consulting delivery portal.

If you are setting 2026 budgets or evaluating supplier strategies, use the report’s scenario templates to stress-test planned investments against commodity and regulatory shocks.

For R&D leaders, begin pilot definitions for electrified hydraulic units using our recommended KPI stack and pilot selection criteria.

Procurement and supply-chain teams should adopt the supplier scorecards to re-run supplier evaluations with energy-efficiency and service capability weighted in the scoring.

PW Consulting’s Heavy Industry Hydraulic System Market Report is designed for immediate integration into executive planning cycles. To access the full dataset, segmentation tables, supplier shares, and downloadable TCO/CAPEX models, visit the official PW Consulting research portal and request the full report package.

For detailed analysis of this topic, please visit the official page:Heavy Industry Hydraulic System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com